Key Points :

- Bitcoin payments failed because they did not solve real merchant problems such as fees, delays, and chargebacks.

- Stablecoins succeeded by eliminating volatility and enabling fast, predictable settlements.

- Businesses now use stablecoins for cross-border payments, liquidity efficiency, and cost reduction.

- Adoption is accelerating because stablecoins integrate into existing systems without changing user behavior.

- The future of payments is not ideological—it is invisible infrastructure powered by blockchain.

Introduction: From Hype to Utility in Crypto Payments

The early vision of cryptocurrency was bold: a decentralized financial system that could replace traditional banking and reshape global commerce. At the center of that vision stood Bitcoin—a revolutionary digital asset that promised borderless, censorship-resistant transactions.

Yet, more than a decade later, Bitcoin has not become a mainstream payment method.

Instead, a different class of digital assets—stablecoins such as USDC and USDT—is quietly transforming global payments.

This shift reveals a critical truth: business adoption is driven not by innovation alone, but by practical problem-solving.

Lessons from Failure: The Early Era of Bitcoin Payments

The first wave of cryptocurrency payments emerged during Bitcoin’s rise into mainstream awareness. Companies such as Overstock and Microsoft began accepting Bitcoin—not because it solved operational challenges, but because it generated attention.

Even major brands like Starbucks experimented with crypto payments through partnerships like Bakkt.

However, these efforts ultimately failed. The reasons were structural:

1. Volatility Destroyed Pricing Stability

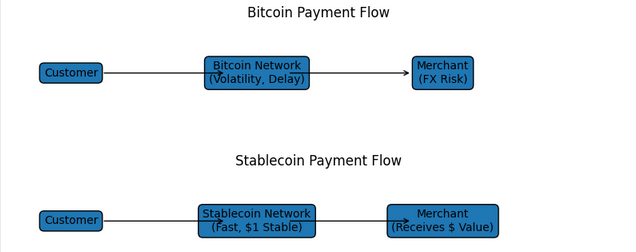

Merchants price goods in fiat currencies, not Bitcoin. Accepting BTC exposed them to constant exchange rate risk. A $5 coffee could become $4 or $6 within minutes.

2. Slow Settlement Times

Bitcoin transactions could take minutes—or longer during network congestion—making it unsuitable for real-time retail.

3. Complexity for Users

Customers had to manage wallets, private keys, and transaction fees. This added friction rather than removing it.

4. No Real Cost Advantage

Transaction fees were not consistently lower than credit card processing, especially during high demand.

5. No Solution to Core Merchant Pain Points

Most importantly, Bitcoin did not solve the issues businesses actually care about:

- Payment delays

- High fees

- Chargebacks

- Cross-border inefficiencies

As a result, Bitcoin payments remained a novelty. Once the hype faded, so did adoption.

The Rise of Stablecoins: Predictability Over Speculation

Unlike Bitcoin, stablecoins were not designed to disrupt ideology—they were designed to solve operational inefficiencies.

Stablecoins like USDC and USDT are pegged to the U.S. dollar. This simple design choice eliminated the biggest barrier to adoption: volatility.

What Makes Stablecoins Different?

- Price Stability: Always close to $1

- Fast Settlement: Transactions settle in seconds on blockchain networks

- Global Accessibility: No need for traditional banking intermediaries

- Programmability: Easily integrated into payment systems

Stablecoins do not promise wealth generation. They promise something far more valuable to businesses: predictability.

(Recommended: Stablecoin vs Bitcoin Payment Flow Comparison Diagram)

Infrastructure, Not Innovation Theater

Stablecoins succeeded because they did not try to change user behavior.

Instead of asking merchants to:

- Think in crypto

- Price in tokens

- Accept volatility

They allowed businesses to:

- Continue pricing in dollars

- Receive exactly the same value

- Settle faster and cheaper

This distinction is critical.

Bitcoin attempted to replace the financial system. Stablecoins aim to upgrade it.

Global Adoption: From Niche Tool to Financial Backbone

After years of development, stablecoins are now being integrated into global payment infrastructure.

Major players are leading this transition:

- Stripe is integrating stablecoin rails for faster global settlements

- Checkout.com is enabling merchants to accept stablecoins

- PayPal launched PYUSD

Across emerging markets in Latin America, Africa, and Asia, businesses increasingly rely on USDT and USDC for cross-border payments.

Why Businesses Prefer Stablecoins

- Near-instant settlement

- Lower transaction fees than credit cards

- Reduced reliance on intermediaries

- Improved cash flow management

For example:

A $500 invoice paid in USDC:

- Settles in seconds

- Arrives as exactly $500

- Avoids FX conversion delays

- Eliminates intermediary fees

For businesses operating on thin margins, this is transformative.

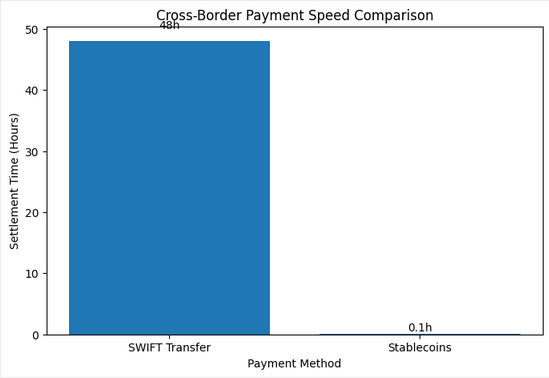

(Recommended: Cross-border Payment Speed Comparison Chart: SWIFT vs Stablecoins)

The Real Use Case: Cross-Border Payments

The most powerful use case for stablecoins is not retail coffee purchases—it is global commerce.

Traditional cross-border payments rely on:

- SWIFT networks

- Correspondent banking

- Multiple intermediaries

This leads to:

- High fees

- Multi-day delays

- Lack of transparency

Stablecoins replace this with:

- Direct blockchain settlement

- Transparent transaction tracking

- Reduced cost structure

This is particularly impactful in regions where:

- Banking infrastructure is weak

- Currency volatility is high

- Access to USD is limited

Stablecoins effectively act as digital dollars with instant mobility.

From Cypherpunk Ideology to Business Utility

The crypto industry initially focused on ideological goals:

- Financial sovereignty

- Decentralization

- Resistance to traditional systems

While important, these ideals did not drive mass adoption.

Stablecoins succeeded because they embraced:

- Regulation

- Compatibility with existing systems

- Business needs

They are not replacing banks—they are becoming part of the financial stack.

The Future: Invisible Blockchain Infrastructure

The next phase of adoption will not be visible to consumers.

Users will:

- Shop online

- Send money abroad

- Pay invoices

Without knowing that blockchain is involved.

Behind the scenes:

- Payments will settle faster

- Costs will decrease

- Intermediaries will shrink

Stablecoins will function as invisible infrastructure—similar to how the internet operates today.

Conclusion: Utility Wins Over Hype

The failure of Bitcoin payments and the rise of stablecoins highlight a fundamental shift in the crypto industry.

Innovation alone is not enough.

For technology to succeed, it must:

- Solve real problems

- Reduce friction

- Integrate seamlessly

Stablecoins have achieved this by focusing on speed, stability, and usability.

For investors and builders, the implication is clear:

The next wave of opportunity in crypto will not come from speculation—but from infrastructure that powers real economic activity.