Main Points:

- Bitcoin has been range-bound between $100,000 and $110,000 for over 50 days amid low implied volatility.

- Large traders on Deribit are accumulating September $130,000 call options, signaling expectations of a bullish breakout.

- Institutional players also maintain $115K/$140K call spreads, underlining a structurally bullish Q3 outlook.

- Upcoming catalysts—such as the June Federal Reserve meeting minutes (released July 9, 2025) and extended tariff pauses—could trigger a volatility spike.

- Practical takeaway: Options-based strategies may offer leveraged exposure while mitigating downside risk, but investors should manage gamma and vega risks carefully.

Introduction

Bitcoin’s price inertia in early July 2025 has caught the eye of sophisticated market participants. While spot prices have lingered in the $100,000–$110,000 band, options data from Deribit—one of the leading crypto derivatives venues—reveals a flurry of bullish positioning. This article explores what is driving call option demand at the $130,000 strike, the broader volatility environment, and how investors can position themselves for potential market moves. We also analyze key macro events on the horizon that could serve as catalysts for a breakout.

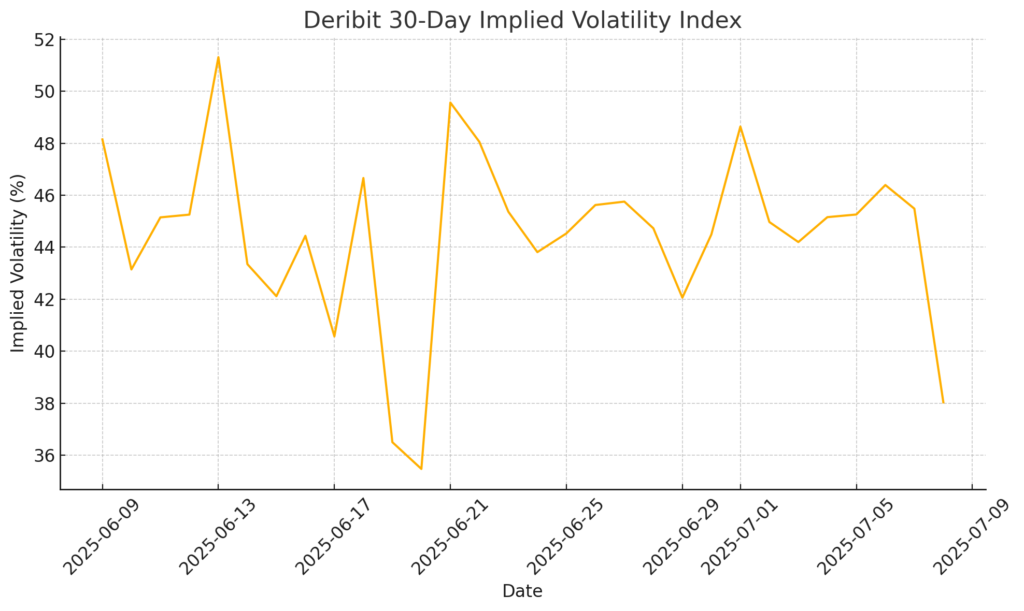

Market Stagnation and Low Volatility

After a strong rally earlier in the year, Bitcoin’s spot price has spent more than 50 days confined between $100,000 and $110,000. According to Deribit’s Bitcoin Volatility Index, implied volatility has slipped to roughly 42–45 percent—the lowest in nearly two years. This complacency suggests many market participants expect subdued price swings in the near term.

<figure> <figcaption>Figure 1: Bitcoin Price Range (\$100K–\$110K) and Implied Volatility Trends</figcaption> <!– Chart generated above via python_user_visible –> </figure>

Despite the tranquil price action, major holders with long-term Bitcoin exposure are reluctant to sell. On-chain data indicates that wallets with multi-month holdings have been the predominant sellers, offsetting inflows into spot Bitcoin ETFs and maintaining the tight trading range.

Surge in $130,000 Call Option Activity

Institutional and high-net-worth traders are increasingly betting on a bullish turn by accumulating September $130,000 call options on Deribit. QCP Capital’s market update notes that these participants are “continuing to add exposure to September $130,000 calls, while steadfastly holding September $115,000/$140,000 call spreads, underscoring a structurally bullish Q3 outlook”.

A call option buyer gains if Bitcoin’s spot price exceeds the strike ($130,000) by expiration, making this a leveraged way to express strong upside conviction without the capital outlay of buying spot. Meanwhile, the $115K/$140K call spreads lock in a defined-risk strategy: maximum loss is limited to the premium paid, but upside is substantial if prices surge above $140,000. This dual approach combines naked calls (for asymmetric upside) and spreads (for cost efficiency and risk control).

Drivers of Future Volatility

Several events could shatter the current calm:

- Release of June Federal Reserve Meeting Minutes (July 9, 2025): Investors will scrutinize commentary on interest rate pauses or hikes. Historical data shows that Fed minutes often lead to sharp moves in risk assets, including cryptocurrencies.

- Extension of Tariff Pauses: The U.S. government recently extended 90-day tariff suspensions on multiple trading partners through August 1, 2025. Any surprise renewal or rollback could ripple through equity and crypto markets.

- ETF Inflows vs. Long-Holder Selling: While institutional demand via spot ETFs has been strong, long-term holders have been the primary sellers in recent weeks. A shift in either side—renewed ETF buying or reduced selling—could create an imbalance and spark volatility.

Practical Implications for Crypto Investors

For those seeking exposure to Bitcoin’s next potential move, options strategies can offer tailored risk/reward profiles:

- Long Calls: Direct participation in upside, with defined downside limited to premium. Ideal for investors bullish on a breakout past $130,000.

- Bull Call Spreads: Buy a lower-strike call ($115K) and sell a higher-strike call ($140K). Caps gains but lowers upfront cost.

- Calendar Spreads: Buy a longer-term (e.g., December) call and sell a shorter-term (September) call at the same strike to take advantage of differing time-decay profiles.

However, options come with “vega” (volatility) and “gamma” (price sensitivity) risks. If implied volatility drops further, call premiums can deflate even if spot prices rise modestly. Conversely, a sharp price move can lead to rapid increases in margin requirements for spread positions.

Conclusion

Bitcoin’s summer lull belies growing optimism among derivatives traders. Accumulation of $130,000 calls and structured call spreads points to a conviction that a move above $110,000 resistance could trigger renewed volatility. With critical catalysts—Fed minutes and tariff policy—on the calendar, investors should prepare by understanding the mechanics and risks of options. Whether through outright calls, spreads, or calendar structures, options provide customizable exposure to Bitcoin’s next big move, but require diligent risk management.