Ripple partners with Ripple and Kyobo Life Insurance to tokenize government bonds

Settlement cycles could shrink from T+2 to near real-time execution

Tokenized government bonds represent a major step in RWA (Real-World Asset) adoption

Institutional-grade custody (Ripple Custody) enables compliant digital asset infrastructure

Stablecoins and 24/7 markets are emerging as the backbone of next-gen finance

Asia, especially South Korea, is becoming a key battleground for institutional blockchain adoption

1. A Strategic Shift: From Crypto Speculation to Institutional Infrastructure

The recent partnership between Ripple and Kyobo Life Insurance marks a defining moment in the evolution of blockchain finance. Rather than focusing on speculative crypto assets, this initiative targets one of the most conservative and foundational pillars of traditional finance: government bonds.

Government bonds, typically denominated in fiat currencies such as USD (e.g., $1,000 face value instruments), are considered low-risk assets and are widely used by institutional investors for liquidity management and capital preservation. By tokenizing these assets, Ripple and Kyobo Life are effectively bridging traditional finance (TradFi) with blockchain-based financial infrastructure.

This move reflects a broader structural shift in the crypto industry. The early era of token launches and retail-driven speculation is giving way to a new phase defined by institutional adoption, regulatory alignment, and real-world utility.

2. How Tokenized Bonds Work on Blockchain

Subheading: From Paper to Programmable Assets

Tokenization refers to the process of converting real-world financial assets into digital tokens that exist on a blockchain. In this case, sovereign bonds—traditionally issued and settled through centralized clearing systems—are transformed into programmable assets.

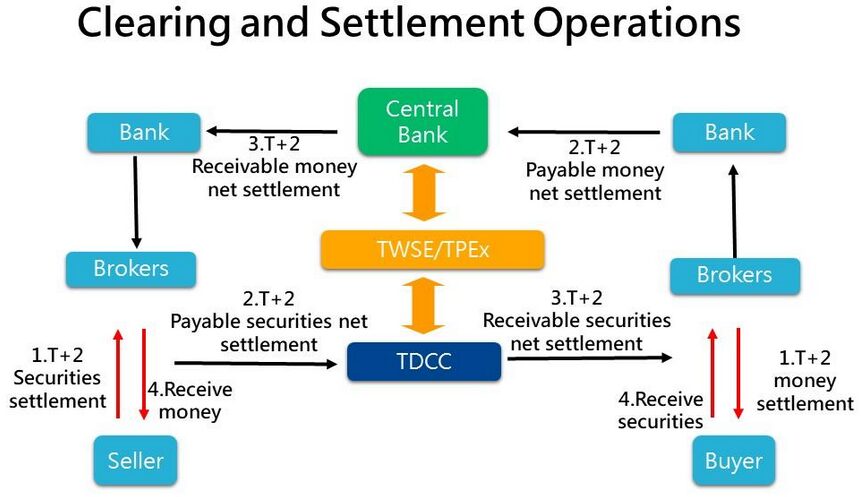

(Diagram: Traditional Bond Settlement vs Tokenized Bond Settlement)

In traditional systems:

Multiple intermediaries are involved (custodians, clearing houses, brokers)

Settlement typically takes T+2 (2 business days)

Counterparty risk exists until final settlement

In contrast, blockchain-based tokenization enables:

Atomic settlement (instant delivery vs payment)

Reduced intermediaries

Transparent, auditable transactions

Ripple’s infrastructure, particularly Ripple Custody, acts as the backbone of this system, offering:

Secure asset storage

Transaction execution

Compliance-ready reporting

3. Why This Matters: Capital Efficiency and Risk Reduction

Subheading: Eliminating Friction in Financial Markets

The traditional bond market is enormous, with global sovereign debt exceeding $100 trillion. Even marginal efficiency gains can translate into billions of dollars in savings.

Tokenized bonds unlock several key advantages:

1. Faster Settlement

Reducing settlement from T+2 to near real-time frees up capital that would otherwise be locked during the clearing period.

2. Lower Counterparty Risk

Simultaneous settlement (Delivery vs Payment) reduces the risk of default between parties.

3. Improved Liquidity

Tokenized assets can be traded more easily across digital platforms, potentially enabling fractional ownership (e.g., $10 increments instead of $1,000 lots).

4. Operational Cost Reduction

Automation reduces reliance on manual reconciliation and legacy infrastructure.

For institutional players like Kyobo Life, these improvements directly translate into higher capital efficiency and better portfolio management.

4. South Korea: A Strategic Launchpad for Digital Finance

Subheading: Regulation Meets Innovation

South Korea has been steadily building a regulatory framework for digital finance since 2017. Licensing systems for remittance and digital asset services have created a compliant environment for experimentation.

This makes the country an ideal testing ground for initiatives like Ripple’s tokenized bond project.

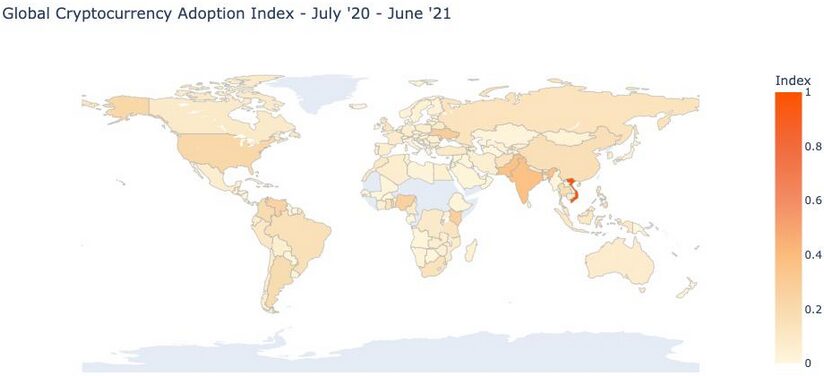

(Chart: Growth of Digital Asset Adoption in Asia vs Global Average)

Key factors supporting this initiative:

Strong regulatory oversight

Advanced financial institutions

High digital adoption rates

According to industry trends, Asia-Pacific is becoming a global leader in institutional blockchain adoption, rivaling the U.S. and Europe.

5. The Role of Stablecoins and 24/7 Financial Markets

Subheading: Always-On Finance Becomes Reality

One of the most forward-looking aspects of this initiative is the potential integration of stablecoins.

Stablecoins—digital assets pegged to fiat currencies like USD ($1 = 1 token)—enable:

Instant settlement

Reduced volatility

Cross-border compatibility

When combined with tokenized bonds, stablecoins create a powerful framework for 24/7 financial markets.

This contrasts sharply with traditional finance, where markets operate within limited hours and settlement is delayed.

The implications are profound:

Continuous liquidity

Global investor participation

Real-time risk management

6. Broader Industry Trends: RWA Tokenization Gains Momentum

Subheading: From Niche to Trillion-Dollar Opportunity

Ripple’s move is part of a larger trend toward Real-World Asset (RWA) tokenization.

Major financial institutions are increasingly exploring tokenization:

Asset managers are tokenizing funds

Banks are experimenting with digital bonds

Governments are testing central bank digital currencies (CBDCs)

Estimates suggest that tokenized assets could reach $10–$16 trillion by 2030.

Key sectors driving this growth:

Government bonds

Real estate

Private credit

Commodities

For investors, this represents a shift from speculative tokens to yield-generating, asset-backed opportunities.

7. Strategic Implications for Investors and Builders

Subheading: Where the Next Opportunities Lie

For readers seeking new crypto assets and revenue streams, this development highlights several actionable trends:

1. Infrastructure Tokens

Projects enabling custody, compliance, and settlement may see increased demand.

2. RWA Platforms

Protocols focused on tokenizing real-world assets could become dominant players.

3. Stablecoin Ecosystems

As settlement layers, stablecoins will play a central role in future finance.

4. Cross-Border Payment Networks

Ripple’s core strength remains in global payments—this initiative reinforces its positioning.

For builders, the message is clear: The next wave of innovation lies not in creating new tokens, but in integrating blockchain into existing financial systems.

8. Conclusion: The Beginning of a New Financial Architecture

The partnership between Ripple and Kyobo Life Insurance is more than a technical experiment—it is a signal of where the financial industry is heading.

By bringing government bonds onto the blockchain, this initiative demonstrates that:

Blockchain is ready for institutional-scale deployment

Real-world assets are the next frontier of crypto

The convergence of TradFi and DeFi is accelerating

As capital continues to flow into AI, digital assets, and tokenized finance, the boundaries between these sectors will increasingly blur.

The future of finance will not be defined by isolated innovations, but by integrated systems that combine trust, efficiency, and programmability.

And in that future, tokenized sovereign debt may become as fundamental as cryptocurrencies once were.

About Us and Media

Blockchain and cryptocurrency media covering and exposing the practical application development on the blockchain industry and undiscovered coins.

Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.