Key Takeaways :

- The S&P 500 surpassed 7,000 for the first time, signaling a strong recovery from geopolitical shocks

- Oil-driven inflation fears are easing, restoring risk appetite across global markets

- Big Tech dominance (“Magnificent Seven”) is accelerating capital concentration

- Algorithmic funds are re-entering markets, amplifying upside momentum

- Crypto markets are stabilizing, but capital is rotating selectively

- AI, RWA (Real World Assets), and infrastructure plays are emerging as the next frontier

S&P 500 Recovery vs Oil Price Shock

1. From War Shock to Market Euphoria: The Macro Reset

The global financial market has once again demonstrated its ability to rapidly reprice risk. On April 16, 2026, the S&P 500 closed above 7,000 for the first time in history, marking a critical psychological and structural milestone. This move represents not merely a recovery, but a full reversal of the geopolitical shock triggered by escalating tensions between the United States and Iran just weeks earlier.

At the height of the crisis in late February, markets priced in a worst-case scenario: a prolonged conflict in the Middle East leading to sustained oil price spikes, inflation resurgence, and potentially a return to stagflation reminiscent of the 1970s. Oil markets reacted immediately, pushing prices higher and igniting fears that central banks would be forced to maintain tighter monetary policies longer than expected.

However, the narrative shifted abruptly. Signals of a ceasefire, followed by renewed diplomatic negotiations, reversed market sentiment. As oil prices declined, inflation expectations softened, and investors quickly rotated back into risk assets.

This pattern highlights a key structural feature of modern markets: geopolitical shocks are increasingly traded as short-term volatility events rather than long-term structural threats—unless they directly disrupt liquidity or earnings.

2. The Power of Big Tech: Concentration, Not Broad Strength

Magnificent Seven Market Influence

The recent rally has not been evenly distributed across the market. Instead, it has been overwhelmingly driven by the so-called “Magnificent Seven”:

- Microsoft

- Apple

- NVIDIA

- Tesla

- Amazon

- Meta Platforms

- Alphabet

These companies have not only led the recovery but have become the core engine of global capital allocation, driven by:

- AI infrastructure demand (especially GPUs and cloud computing)

- Strong earnings growth expectations (projected ~43% YoY in tech)

- Institutional preference for scalable, high-margin businesses

However, beneath the surface, the market tells a different story. Equal-weighted indices still lag behind, indicating that the rally is narrow and concentrated. This divergence introduces a structural risk: if capital concentration unwinds, the broader market may not have sufficient strength to sustain current levels.

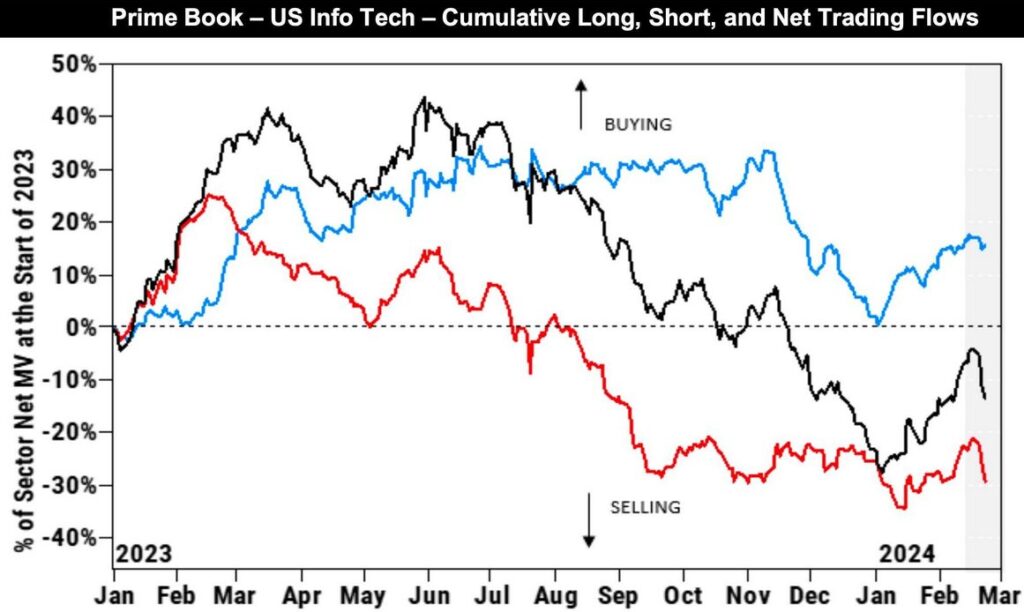

3. Algorithmic Capital and the Acceleration of Momentum

Algorithmic Trading Flow Impact

Another critical driver of the rally is the reactivation of systematic and algorithmic funds.

After reducing exposure during the geopolitical uncertainty, these funds are now rapidly re-entering the market. Unlike discretionary investors, algorithmic strategies respond to:

- Volatility compression

- Trend confirmation

- Liquidity conditions

As these signals turned positive, large-scale buybacks were triggered, creating a feedback loop:

Price increase → trend confirmation → more algorithmic buying → further price increase

This mechanism explains the speed and intensity of the recovery. Importantly, it also implies that:

- The current rally is mechanically reinforced, not purely fundamentally driven

- Downside risks can re-emerge quickly if signals reverse

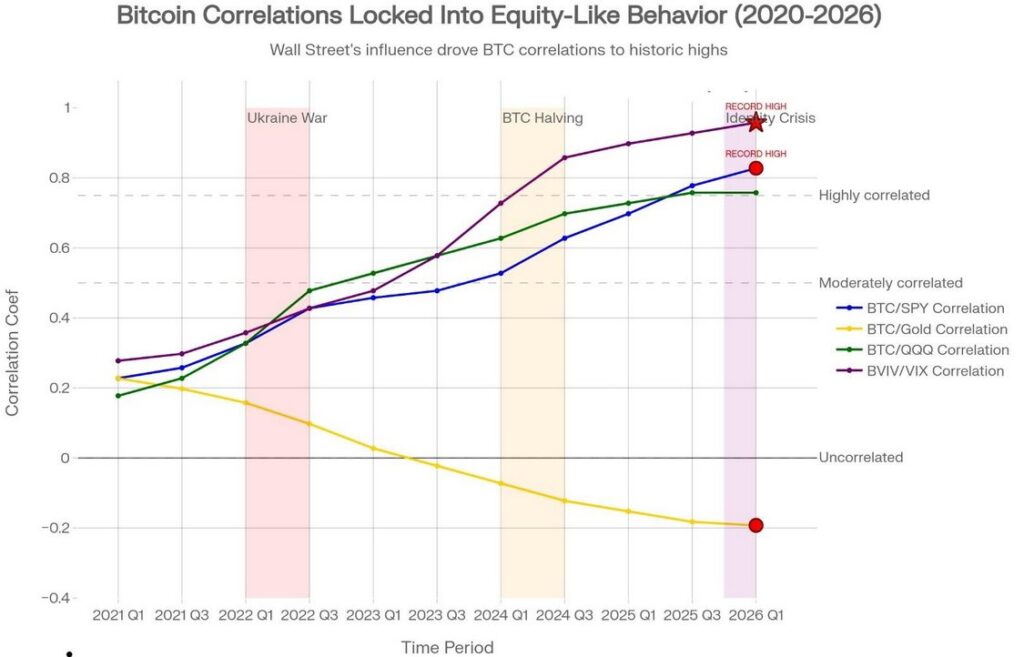

4. Crypto Market Response: Stabilization, Not Full Rotation

Bitcoin and Risk Asset Correlation

The cryptocurrency market has mirrored macro sentiment shifts, but with important nuances.

Bitcoin initially declined during peak geopolitical tension, reflecting its increasing correlation with risk assets. However, as tensions eased and oil prices fell, Bitcoin rebounded.

Yet, unlike previous cycles, the recovery in crypto has been selective rather than broad-based:

- Large-cap assets show resilience

- Many altcoins continue to underperform

- Liquidity remains concentrated

This aligns with a broader trend observed in recent months:

The era of indiscriminate crypto rallies is over. Capital is becoming more selective, favoring infrastructure, utility, and real-world integration.

5. Capital Rotation: From Web3 Speculation to AI and Real Assets

A defining feature of the current cycle is capital reallocation.

Institutional and venture capital flows are increasingly shifting toward:

1. AI Infrastructure

- Data centers, chips, and compute platforms

- Tokenization opportunities around AI agents

2. Real World Assets (RWA)

- Tokenized bonds, real estate, and commodities

- Stable yield generation mechanisms

3. Financial Infrastructure

- Cross-border settlement

- Compliance-integrated blockchain systems

This shift reflects a deeper structural evolution:

- Early crypto cycles were driven by narrative and speculation

- The current phase is driven by cash flow, yield, and real-world integration

6. The Hidden Risk: Narrow Breadth and Overconfidence

Despite bullish momentum, caution remains warranted.

Legendary investor Warren Buffett has pointed out that recent declines were relatively shallow compared to historical crises. This suggests:

- The market has not undergone a true capitulation

- Risk may be underpriced

Key risks include:

- Over-reliance on a small number of mega-cap stocks

- Reversal of algorithmic flows

- Re-acceleration of inflation if oil prices spike again

7. Strategic Implications for Crypto and Blockchain Builders

For builders and investors in the crypto space, the implications are clear:

1. Focus on Real Utility

Projects must demonstrate:

- Revenue models

- Integration with financial systems

- Regulatory compatibility

2. Align with Macro Trends

Opportunities lie at the intersection of:

- AI + Blockchain

- RWA + Tokenization

- Compliance + Infrastructure

3. Prepare for Selective Capital

Funding is still available—but only for:

- High-quality teams

- Clear product-market fit

- Scalable architecture

Conclusion: The Next Cycle Is Not Speculative — It Is Structural

The S&P 500 crossing 7,000 is more than a milestone—it is a signal.

Markets are transitioning from a phase of reactive volatility to one of structural capital allocation, where:

- AI defines productivity and earnings growth

- Real-world assets anchor yield

- Crypto evolves into financial infrastructure

For those seeking the next opportunity, the lesson is clear:

The future will not reward speculation alone—it will reward systems that connect capital, technology, and real-world value.