Key Takeaways :

- A renewed “Bye America” trade is emerging as investors reassess the safety and carrying cost of U.S. dollar–denominated assets.

- A potential liquidation of up to $1.7 trillion in U.S. Treasuries by European stakeholders could accelerate a structural shift away from the dollar.

- Bitcoin is increasingly positioned as a macro-alternative asset, not merely a speculative instrument.

- Four distinct transmission channels explain how dollar weakness translates into rising demand for Bitcoin.

- ETF inflows and spot-led demand are critical indicators separating sustainable growth from leverage-driven volatility.

Introduction: From “Buy America” to “Bye America”

For decades, the U.S. dollar has functioned as the unquestioned anchor of the global financial system. Its role as the world’s primary reserve currency allowed the United States to finance deficits cheaply, export inflation, and maintain unrivaled geopolitical influence. However, recent market behavior suggests that this dominance is no longer taken for granted.

A renewed wave of what analysts now call the “Bye America” trade is taking shape. This is not a political slogan, but an accounting-driven reallocation of capital based on yield differentials, currency risk, and hedging costs. As confidence in the long-term stability and cost-efficiency of holding dollar assets erodes, investors are increasingly searching for alternatives that sit outside the direct control of any single nation-state.

At the center of this reassessment stands Bitcoin, whose market capitalization and liquidity have grown to a scale where it can plausibly compete with traditional macro hedges such as gold.

The $1.7 Trillion Trigger: Europe, Geopolitics, and U.S. Treasuries

Recent reporting suggests that European Union leaders are considering the sale of as much as $1.7 trillion in U.S. Treasury holdings, potentially using these assets as leverage in broader geopolitical negotiations, including those related to Greenland. While the full execution of such a sale remains uncertain, even the discussion itself carries profound signaling effects.

U.S. Treasuries have long been treated as the world’s ultimate “risk-free” asset. A coordinated or symbolic reduction in holdings by major foreign stakeholders would undermine this perception and force global investors to confront an uncomfortable reality: the safety of Treasuries is inseparable from confidence in U.S. fiscal discipline and dollar stability.

If that confidence weakens, capital does not simply disappear—it seeks new reservoirs of perceived safety or asymmetric upside. Increasingly, Bitcoin is being evaluated as one such destination.

Channel One: Global Financial Easing and Risk Appetite Expansion

The first transmission channel linking dollar weakness to Bitcoin demand operates through global financial conditions. A declining dollar typically loosens financial constraints worldwide. Because a significant portion of global trade, debt, and commodities are priced in dollars, a weaker dollar reduces the real burden of dollar-denominated liabilities.

As financial conditions ease, investors’ risk tolerance expands. Historically, this has benefited equities, emerging market assets, and commodities. In the current cycle, it is also benefiting crypto assets—particularly Bitcoin, which sits at the intersection of risk asset and monetary hedge.

Bitcoin’s fixed supply narrative becomes more compelling when liquidity is abundant and the opportunity cost of holding non-yielding assets declines. In this environment, Bitcoin absorbs marginal capital flows that might previously have gone exclusively into high-growth equities or gold.

Channel Two: Real Interest Rates and the Opportunity Cost of Holding Bitcoin

The second channel is the trajectory of real interest rates—nominal rates adjusted for inflation. When real rates fall, the opportunity cost of holding assets that do not generate yield, such as gold or Bitcoin, declines.

Historically, gold has been the primary beneficiary of negative or declining real rates. However, Bitcoin introduces a new dynamic. While gold is mature, slow-moving, and largely driven by institutional and central bank flows, Bitcoin is younger, more liquid on a 24/7 basis, and far more sensitive to shifts in macro expectations.

This sensitivity cuts both ways, increasing volatility, but it also allows Bitcoin to respond faster to changing monetary regimes. In a prolonged environment of suppressed real yields, Bitcoin’s asymmetric upside becomes increasingly attractive relative to gold’s more defensive profile.

Channel Three: Hedging Costs and Cross-Border Portfolio Reallocation

The third channel is less visible but arguably more powerful: currency hedging costs faced by non-U.S. investors.

For European and Asian institutions, holding U.S. assets often requires hedging dollar exposure back into local currency. As interest rate differentials widen and volatility increases, the cost of these hedges rises. At a certain point, the net yield on U.S. Treasuries or corporate bonds becomes unattractive once hedging expenses are accounted for.

Bitcoin, by contrast, does not require currency hedging in the traditional sense. It is not a liability of the U.S. government or any central bank. This neutrality makes it an increasingly appealing diversification tool when traditional dollar assets lose their cost efficiency.

In this context, Bitcoin is less a bet on price appreciation and more a structural hedge against monetary fragmentation.

Channel Four: Crypto-Native Leverage and Market Structure

The fourth channel is internal to the crypto market itself: leverage mechanics.

Spot-driven rallies, supported by genuine demand such as ETF inflows, tend to be more stable and durable. In contrast, rallies dominated by futures leverage can amplify price movements but also increase fragility.

As Bitcoin integrates further into traditional financial infrastructure through regulated ETFs, custody solutions, and institutional-grade derivatives, the composition of demand matters more than ever. Monitoring ETF inflows provides insight into whether price appreciation is backed by long-term capital or speculative leverage.

ETF Flows as a Health Indicator

One of the most important developments in recent years has been the rise of Bitcoin ETFs. These vehicles allow capital to enter the Bitcoin market without requiring investors to manage private keys or interact directly with crypto exchanges.

Sustained ETF inflows suggest that Bitcoin is being accumulated as a strategic asset, not merely traded as a short-term speculation. This distinction is crucial when evaluating whether Bitcoin can genuinely rival gold as a macro store of value.

[Bitcoin ETF inflows vs. price performance]

Political Signals: Digital Dollars and Institutional Acceptance

Political rhetoric is also evolving. Figures such as Kevin Warsh, whose name has been mentioned in connection with senior roles at the Federal Reserve under a potential Donald Trump administration, have publicly acknowledged the technological merits of Bitcoin while exploring the concept of a digital dollar.

This dual-track approach—recognizing Bitcoin’s innovation while pursuing sovereign digital currency solutions—underscores a key reality: Bitcoin is no longer dismissible. Even policymakers who prioritize dollar dominance are forced to engage with it seriously.

Can Bitcoin Really Surpass Gold?

Gold’s market capitalization remains significantly larger than Bitcoin’s, but the gap is narrowing. Gold benefits from millennia of trust and central bank adoption, while Bitcoin benefits from portability, verifiability, and resistance to debasement.

In a world where capital moves at digital speed and geopolitical risk is increasingly financialized, Bitcoin’s characteristics align closely with the needs of modern portfolios. Whether it fully “overtakes” gold is less important than the fact that it is now firmly established as a parallel macro asset.

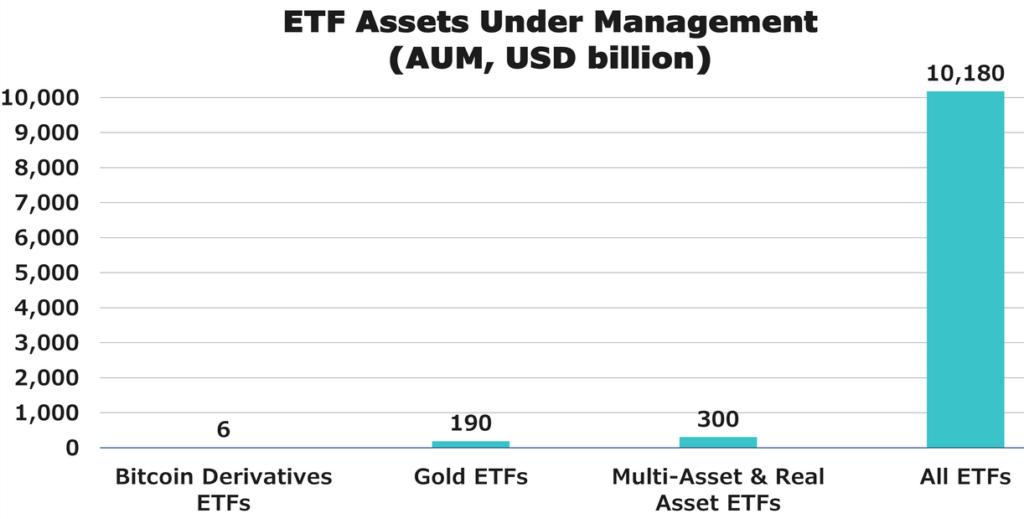

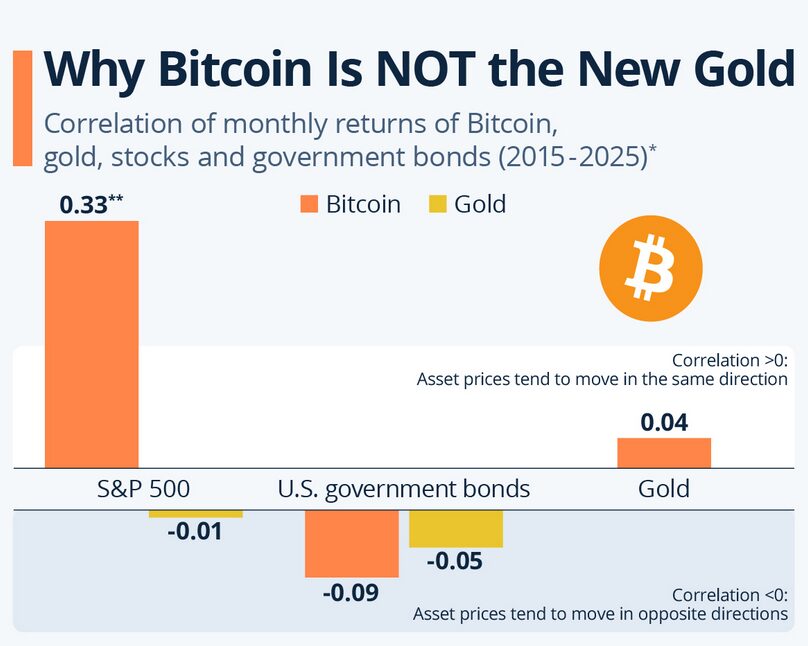

[Bitcoin vs. Gold market capitalization and correlation trends]

Conclusion: Bitcoin as a Macro Alternative Asset

The weakening of the dollar does not automatically guarantee Bitcoin’s ascent. However, when viewed through the lens of capital flows, real rates, hedging costs, and market structure, a coherent narrative emerges.

Bitcoin is no longer merely a speculative trade. It is increasingly a macro alternative asset, absorbing capital that once flowed almost exclusively into gold or U.S. Treasuries. As the global financial system transitions from unipolar dollar dominance toward a more fragmented landscape, Bitcoin’s role is likely to grow—not as a replacement for all traditional assets, but as a critical component of diversified, forward-looking portfolios.