Key Points :

- The American Bankers Association challenges the White House’s analysis on stablecoin yield bans.

- The Council of Economic Advisers argues banning yield has minimal impact on bank lending (~$2.1B increase, ~0.02%).

- Banks warn the real risk is deposit outflow if yield is allowed, especially from community banks.

- Stablecoin market could expand from ~$300B to $1–2 trillion, amplifying systemic effects.

- Regulatory debates (e.g., CLARITY Act) may determine whether yield-bearing stablecoins are permitted.

- Institutional adoption and DeFi integration are accelerating demand for yield-generating digital dollars.

1. The Policy Clash: Yield Ban vs Market Reality

The debate surrounding stablecoin yields has rapidly evolved into one of the most critical battlegrounds in modern financial policy. At the center of this dispute lies a fundamental question: should stablecoins function merely as digital cash equivalents, or should they evolve into yield-generating financial instruments capable of competing directly with bank deposits?

The Council of Economic Advisers recently published an analysis suggesting that banning yield on stablecoins would have only a negligible effect on the traditional banking sector. According to their estimates, prohibiting yield would increase bank lending by approximately $2.1 billion, representing just 0.02% growth—statistically insignificant in the broader financial system.

However, this conclusion has been strongly challenged by the American Bankers Association. Their critique is not merely about numbers—it is about framing the wrong question. Instead of asking what happens if yield is banned, the ABA argues policymakers must consider the opposite scenario: what happens if yield is allowed.

This reframing shifts the conversation from marginal impacts to systemic transformation. Yield-bearing stablecoins are not just a technical feature—they represent a structural alternative to traditional banking deposits.

2. The Real Risk: Deposit Flight from Banks

The concern raised by the ABA is rooted in a fundamental economic principle: capital flows toward yield.

If stablecoins begin offering competitive returns—especially when combined with instant liquidity, programmability, and global accessibility—depositors may increasingly move funds out of traditional banks. This risk is particularly acute for smaller, community-based financial institutions that rely heavily on retail deposits as their primary funding source.

Unlike large banks with diversified funding channels, community banks may be forced to replace lost deposits with wholesale funding. This form of borrowing is typically more expensive and volatile, increasing their cost of capital.

The downstream effects are significant:

- Reduced lending capacity to local businesses

- Higher borrowing costs for consumers

- Contraction in regional economic activity

In essence, yield-bearing stablecoins could act as a parallel banking system, siphoning liquidity from traditional institutions while operating under a different regulatory framework.

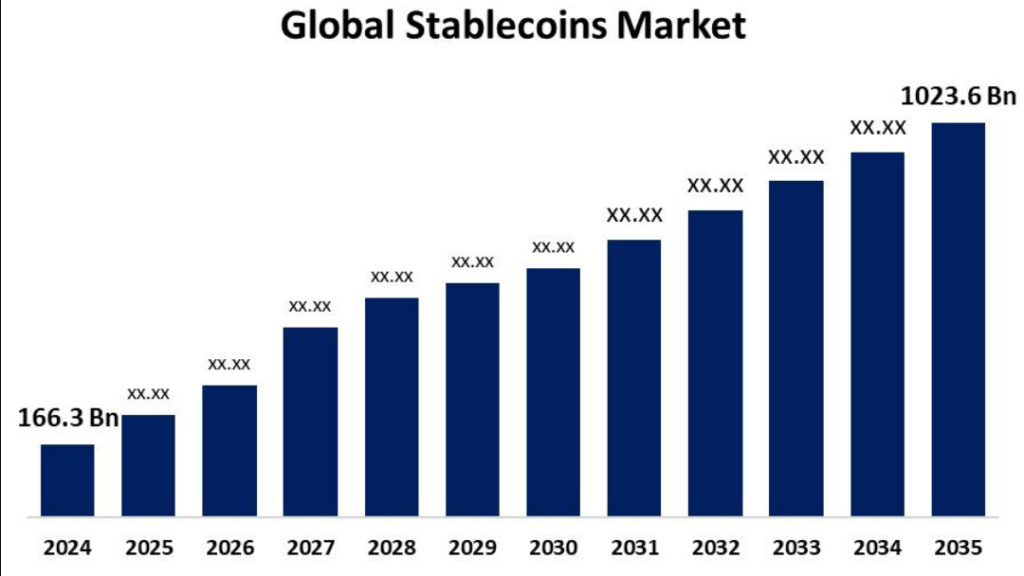

3. Market Expansion: From $300B to $2 Trillion

One of the most critical flaws identified in the White House analysis is its reliance on current market size. The stablecoin market today is estimated at around $300 billion, but projections from the U.S. Treasury suggest it could grow to between $1 trillion and $2 trillion in the coming years.

This projected growth fundamentally changes the scale of the problem.

Stablecoin Market Growth Projection

At a $2 trillion scale, even a modest shift of capital from bank deposits into stablecoins could trigger:

- Significant balance sheet contraction in banks

- Increased reliance on central bank facilities

- Structural shifts in monetary transmission mechanisms

This is no longer a niche crypto issue—it becomes a macroeconomic concern.

4. Yield as a Feature: Why It Matters in Crypto Economics

Yield is not just an incentive—it is the foundation of modern crypto finance.

In decentralized finance (DeFi), stablecoins are frequently used in:

- Lending protocols

- Liquidity provision

- Automated market making

- Cross-border settlement systems

Platforms built on networks like Ethereum have normalized the expectation that digital dollars should generate returns. Even centralized issuers are under pressure to remain competitive with DeFi yields.

This creates a structural tension:

- Regulators aim to preserve financial stability

- Markets demand capital efficiency and yield

The result is a policy dilemma with no easy resolution.

5. Regulatory Turning Point: The CLARITY Act

The ongoing discussions around the CLARITY Act may determine the future of stablecoin yields in the United States.

Negotiations between the crypto industry and banking sector are intensifying, with several key questions under consideration:

- Should stablecoin issuers be allowed to distribute yield?

- If so, under what regulatory framework?

- Should they be treated as banks, funds, or a new asset class?

The outcome of this legislation could set a global precedent, influencing regulatory approaches in Europe, Asia, and emerging markets.

6. Global Trends: Institutional Adoption and Stablecoin Demand

Beyond the U.S., stablecoins are gaining traction as a foundational layer of global finance.

Recent trends include:

- Increased use in cross-border payments

- Integration with fintech and remittance platforms

- Adoption by institutional investors seeking on-chain liquidity

Major financial players are exploring tokenized deposits and blockchain-based settlement systems, signaling that the line between traditional finance and crypto is rapidly blurring.

In regions with unstable currencies, stablecoins already function as a de facto alternative to local banking systems. Adding yield to these instruments could accelerate their adoption even further.

7. Strategic Implications for Investors and Builders

For readers seeking new crypto assets, revenue opportunities, and practical blockchain applications, this debate carries significant implications.

Opportunities

- Yield-bearing stablecoins as income-generating instruments

- Infrastructure for compliance, custody, and reporting

- Cross-border payment solutions leveraging stablecoins

Risks

- Regulatory uncertainty

- Potential restrictions on yield distribution

- Competition from bank-issued digital currencies

Projects that successfully navigate this regulatory landscape could become foundational components of the next financial system.

Conclusion: A Redefinition of Money and Banking

The debate over stablecoin yield is not merely a technical or regulatory issue—it represents a fundamental shift in how money functions in the digital age.

On one side, traditional banks seek to preserve deposit-based funding models that have underpinned financial systems for decades. On the other, the crypto ecosystem is building programmable, yield-generating alternatives that challenge those very foundations.

Whether yield is banned or allowed, the trajectory is clear: stablecoins are evolving from simple payment tools into full-fledged financial instruments.

The real question is not whether this transformation will happen—but how quickly, and under whose rules.