Main Points :

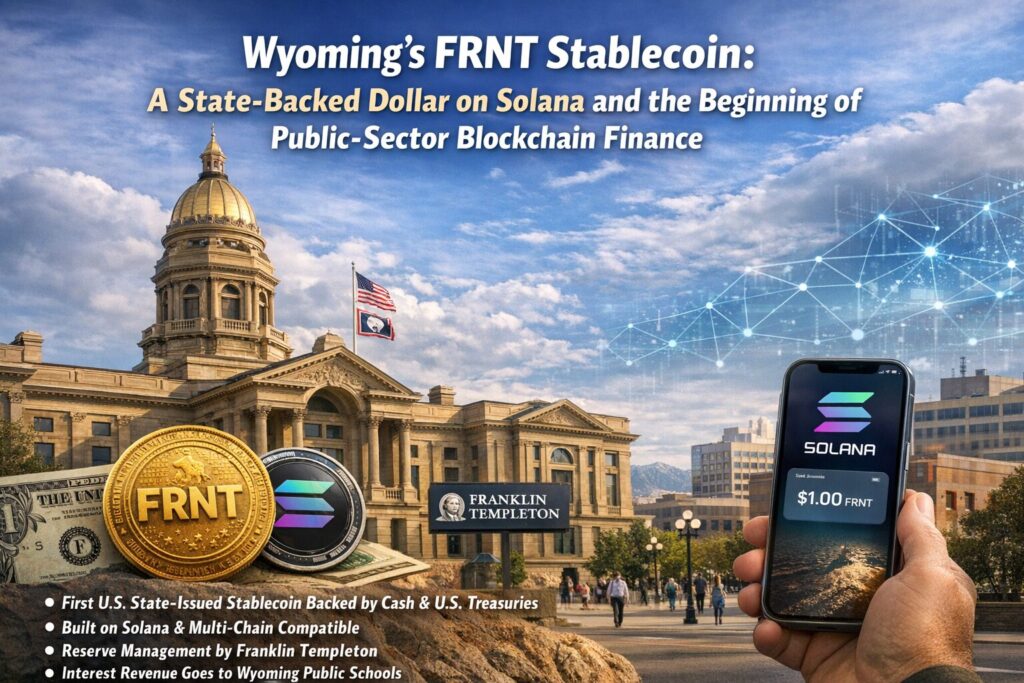

- Wyoming has launched FRNT, the first U.S. state-issued and state-backed stablecoin, fully backed by cash and U.S. Treasuries.

- FRNT is issued on Solana and designed as a multi-chain asset, transferable across Ethereum-compatible and other major networks.

- Asset management of reserves is handled by Franklin Templeton, while interest revenue flows to Wyoming public schools, not token holders.

- The project positions Wyoming as a live testbed for how blockchain-based money can operate inside public finance.

- Yield is intentionally excluded to avoid U.S. regulatory ambiguity around securities and banking products.

Introduction: A Turning Point for Stablecoins and Public Finance

In early January 2026, the State of Wyoming quietly crossed a historic threshold. For the first time in the United States, a state government issued its own dollar-pegged stablecoin and released it directly into the open cryptocurrency market. The token, named Frontier Stable Token (FRNT), is not a pilot confined to a private sandbox or limited to institutional experimentation. It is live, purchasable by the public, and integrated into real blockchain infrastructure.

This move places Wyoming at the forefront of an emerging debate: whether stablecoins should remain predominantly private instruments issued by fintech firms and crypto companies, or whether public institutions can and should play a direct role. In a market currently dominated by private issuers, FRNT represents a fundamentally different model—one where a U.S. state guarantees the backing, controls governance, and channels economic benefits into public goods.

For readers seeking new crypto assets, revenue models, or practical blockchain applications, FRNT is more than another stablecoin. It is an experiment in public-sector monetary infrastructure.

What Is FRNT? Wyoming’s State-Issued Stablecoin Explained

FRNT is a U.S. dollar-pegged digital token issued and backed by the State of Wyoming. Each FRNT is redeemable at a 1:1 ratio with the U.S. dollar and is fully collateralized by cash and short-term U.S. Treasury securities.

Unlike most stablecoins, which are issued by private companies under varying regulatory interpretations, FRNT is issued by a state authority. The project is overseen by Wyoming’s Stable Token Commission and was publicly announced in cooperation with state media.

Key structural characteristics include:

- 100% reserve backing in cash and U.S. Treasuries

- Public-sector issuance and oversight

- On-chain transparency consistent with modern blockchain standards

- Open market availability, rather than restricted institutional use

This design is intentional. Wyoming legislators and regulators have spent years building a legal framework for digital assets, including DAO recognition, crypto custody statutes, and special-purpose depository institutions. FRNT is the culmination of that groundwork.

Why Solana? Infrastructure Choices and Performance Considerations

The initial issuance of FRNT takes place on Solana, a high-throughput, low-latency blockchain known for its speed and low transaction costs. For a state-issued payment-oriented token, these characteristics matter.

Solana offers:

- Near-instant transaction finality

- Extremely low transaction fees (fractions of a dollar)

- High scalability suitable for payment and settlement use cases

For public finance experimentation—such as potential tax payments, disbursements, or inter-agency transfers—these attributes are essential. High fees or network congestion would undermine the practicality of a government-backed digital dollar.

Wyoming’s choice of Solana reflects a pragmatic engineering decision, not ideological alignment. The state is less concerned with chain maximalism and more focused on operational reliability.

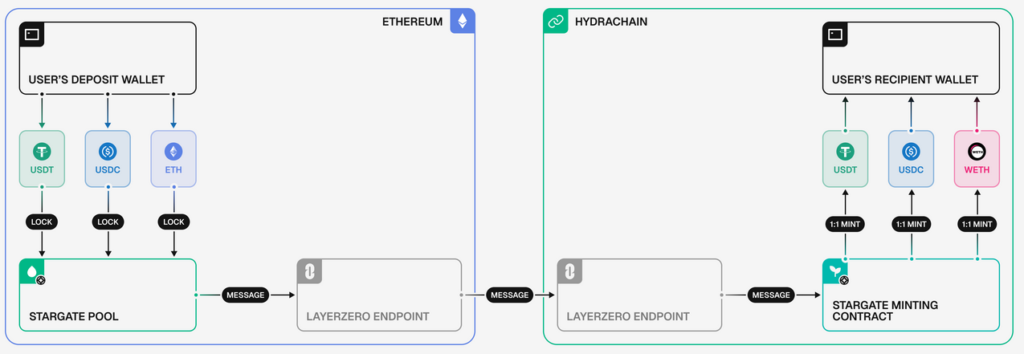

Multi-Chain by Design: FRNT Beyond a Single Ecosystem

Although Solana is the launch chain, FRNT is explicitly designed as a multi-chain stablecoin. Using Stargate, FRNT can be transferred across several major networks, including:

- Ethereum

- Arbitrum

- Avalanche

- Base

- Optimism

- Polygon

This approach ensures that FRNT is not locked into a single ecosystem. Instead, it can circulate across DeFi protocols, payment systems, and exchanges wherever users operate.

For developers and businesses, this dramatically increases utility. A state-backed stablecoin that can move freely across chains begins to resemble neutral digital public infrastructure rather than a proprietary product.

Distribution and Market Access: Kraken as the Initial Gateway

At launch, FRNT is available for public purchase through Kraken, a U.S.-based exchange with a strong regulatory reputation and a historical connection to Wyoming’s crypto-friendly policies.

Kraken’s involvement serves multiple purposes:

- Provides compliant fiat on- and off-ramps

- Ensures liquidity and price stability at launch

- Signals regulatory seriousness to institutional observers

By choosing an established exchange rather than a niche DeFi-only rollout, Wyoming appears focused on credibility and accessibility, not speculative hype.

Reserve Management: Franklin Templeton and Institutional-Grade Custody

One of the most distinctive aspects of FRNT is how its reserves are managed. The underlying assets—cash and U.S. Treasuries—are overseen by Franklin Templeton, one of the world’s largest and most respected asset managers.

This arrangement addresses one of the largest concerns in the stablecoin market: trust in reserve quality and management.

Key implications include:

- Institutional-grade risk management

- Conservative asset allocation

- Reduced counterparty risk compared to crypto-native issuers

Crucially, interest generated by these reserves does not go to token holders. Instead, it is allocated to Wyoming public schools, effectively turning stablecoin float into a public revenue source.

This flips the traditional stablecoin model on its head.

Why FRNT Does Not Pay Yield to Holders

At launch, FRNT is strictly a non-yield-bearing stablecoin. This decision is not technical—it is regulatory.

In the United States, yield-bearing digital assets sit in a gray area between:

- Securities

- Banking products

- Money market instruments

By excluding yield, Wyoming aims to avoid triggering federal securities laws or banking regulations before clear guidance exists. State officials have openly stated that this structure could change in the future if and when regulatory clarity improves.

For now, FRNT prioritizes legal durability over competitive yield.

FRNT as a Public Finance Experiment

Wyoming has allocated approximately $6 million to the FRNT initiative so far, with discussions ongoing about additional funding. This positions FRNT not merely as a crypto product, but as a policy experiment.

Potential long-term applications include:

- State-level payments and settlements

- Blockchain-based grant distribution

- Faster inter-governmental transfers

- Transparent treasury operations

If successful, FRNT could become a reference model for other U.S. states—or even national governments—seeking alternatives to private stablecoin dominance.

Implications for the Broader Stablecoin Market

FRNT’s launch comes at a moment of intense global scrutiny of stablecoins. Regulators worldwide are debating reserve requirements, issuer licensing, and systemic risk.

Wyoming’s approach offers a third path:

- Not a central bank digital currency (CBDC)

- Not a private fintech issuance

- But a state-backed, open-network digital dollar

For investors and builders, this raises important questions:

- Could state-issued stablecoins coexist with private ones?

- Will public issuers set new standards for transparency?

- Could DeFi protocols eventually integrate government-backed liquidity?

FRNT does not answer these questions yet—but it makes them unavoidable.

Conclusion: A Small State, a Large Signal

Wyoming’s FRNT stablecoin is not about speculation, high yields, or meme-driven narratives. It is about institutional experimentation at the boundary of public finance and open blockchain systems.

By issuing a fully backed, non-yield-bearing, multi-chain stablecoin and directing economic benefits to public schools, Wyoming has created a model that challenges assumptions about who should issue digital money and why.

For those seeking practical blockchain use cases, FRNT represents one of the clearest signals yet that governments are no longer just regulating crypto—they are beginning to build on it.