Main Points :

- The U.S. Office of the Comptroller of the Currency (OCC) has issued a Notice of Proposed Rulemaking (NPRM) to implement the GENIUS Act, the first comprehensive federal framework for payment stablecoins.

- Banks, foreign issuers, and non-bank companies seeking federal qualification will fall under the regulatory regime.

- Stablecoins must maintain 1:1 reserve backing, publish redemption policies, and disclose reserve compositions monthly.

- Non-compliant stablecoins may face exclusion from major exchanges and custodians.

- The global stablecoin market, currently around $310 billion, could exceed $500 billion by the end of 2026.

- Regulatory clarity may accelerate institutional adoption but compress speculative DeFi yields.

1. Introduction: Regulatory Clarity Arrives for Dollar Stablecoins

On February 26, 2026, the U.S. Office of the Comptroller of the Currency (OCC) announced a proposed rule to implement the “GENIUS Act,” legislation enacted in July 2025 establishing the first comprehensive federal framework governing payment stablecoins in the United States.

This development marks a structural inflection point for the global digital asset industry. For years, stablecoins—digital tokens pegged to the U.S. dollar—have functioned as the backbone of crypto trading, DeFi liquidity, and cross-border settlement. Yet their regulatory treatment remained fragmented across federal and state jurisdictions.

The GENIUS Act changes that. It defines who may issue payment stablecoins, how reserves must be structured, what disclosures are mandatory, and how redemption must operate. In short, it transforms stablecoins from a regulatory gray zone into a federally supervised financial product class.

For readers seeking new crypto assets, yield opportunities, or practical blockchain applications, this moment deserves close attention. Regulatory clarity often precedes capital inflows.

2. Scope of the Proposed Rule: Who Is Covered?

2.1 Banks and Their Subsidiaries

The proposed rule applies to:

- National banks

- Federal savings associations

- Their subsidiaries

- Federal branches of foreign banks

Under the framework, banks may issue, custody, and settle payment stablecoins without prior individualized approval, provided they comply with prudential requirements.

This provision significantly lowers entry barriers for traditional financial institutions. Banks that previously hesitated due to regulatory ambiguity can now deploy stablecoin products as part of core operations—potentially integrating them into deposit services, treasury management, and cross-border payments.

2.2 Foreign Issuers and Non-Bank Entrants

The framework also captures:

- Foreign payment stablecoin issuers operating in the U.S.

- Non-bank companies seeking “federal qualified stablecoin issuer” status

This is particularly important. It creates a pathway for fintech and crypto-native companies to compete directly with banks—provided they meet reserve, governance, and transparency standards.

This dual-track model—banks and federally qualified non-banks—signals that the U.S. does not intend to reserve stablecoin issuance exclusively for deposit-taking institutions. Instead, it fosters competition within a defined compliance perimeter.

3. Core Requirements Under the GENIUS Act

3.1 1:1 Reserve Backing

Payment stablecoins must be fully backed on a 1:1 basis with high-quality liquid assets.

While the rule leaves technical reserve composition details to be refined, the intent is clear: eliminate algorithmic or partially collateralized structures for payment-class stablecoins.

This effectively narrows the playing field to cash, short-term U.S. Treasuries, and similar low-risk instruments.

3.2 Mandatory Redemption Policy Disclosure

Issuers must publicly disclose redemption policies, ensuring holders understand:

- Whether redemption is direct or intermediary-based

- Timeframes for settlement

- Any fees or thresholds

This provision aims to prevent the kind of opacity that fueled past stablecoin crises.

3.3 Monthly Reserve Composition Reporting

Issuers must disclose reserve compositions monthly.

This mirrors current practices by leading compliant issuers but makes transparency a statutory obligation rather than a voluntary practice.

3.4 AML, BSA, and OFAC Integration

Anti-money laundering (AML), Bank Secrecy Act (BSA), and OFAC sanctions compliance will be implemented through joint rulemaking with the U.S. Treasury.

This integration ensures that stablecoin issuers are embedded within the same financial crime compliance architecture as banks.

4. Timeline and Transition

- The final rule must be published by July 18, 2026.

- It will take effect 120 days after publication or January 18, 2027—whichever comes first.

- Exchanges and custodians will receive a three-year transition period.

- Public comments are accepted for 60 days following Federal Register publication.

This phased approach reduces market disruption while signaling inevitability: non-compliance will eventually carry operational consequences.

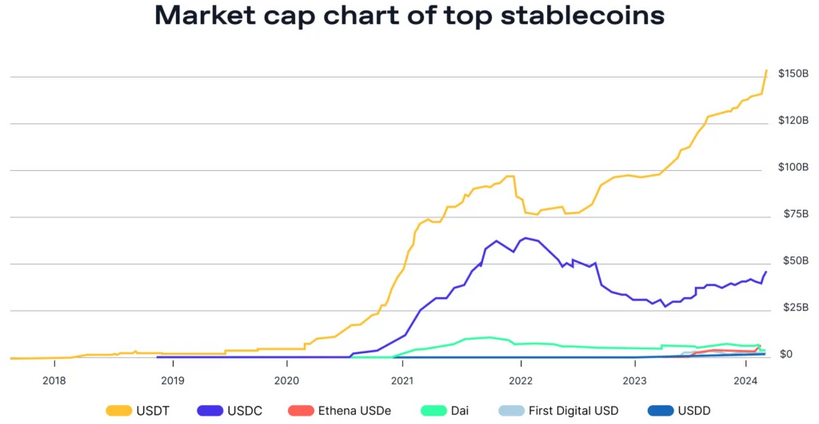

5. Market Impact: Toward a $500 Billion Stablecoin Ecosystem

The global stablecoin market currently stands at approximately $310 billion.

Forecasts suggest it could surpass $500 billion by the end of 2026.

5.1 Institutional Acceleration

Regulatory certainty reduces compliance risk.

Banks may:

- Issue proprietary stablecoins

- Custody third-party stablecoins

- Integrate stablecoin settlement into payment rails

This opens pathways for:

- On-chain treasury management

- 24/7 cross-border corporate settlement

- Tokenized deposit competition

5.2 Competitive Pressure on Deposits

If stablecoins become yield-neutral but frictionless, banks may face deposit competition.

Conversely, banks issuing stablecoins could internalize this flow, preventing disintermediation.

6. Risks and Structural Shifts

6.1 Liquidity Concentration

Liquidity may concentrate into federally compliant stablecoins.

Smaller, offshore, or algorithmic tokens could lose exchange listings.

6.2 DeFi Yield Compression

As reserve backing tightens and speculative leverage declines:

- Risk-adjusted yields may compress.

- High-yield unstable structures may disappear.

DeFi protocols may pivot toward:

- Real-world asset (RWA) tokenization

- Treasury-backed lending

- Permissioned liquidity pools

6.3 Delisting Risk for Non-Compliant Coins

Major platforms may exclude non-compliant stablecoins to avoid supervisory exposure.

This could lead to rapid market share redistribution.

7. Geopolitical and Strategic Implications

Recent reports suggest discussions around deploying U.S. dollar stablecoins in reconstruction and cross-border development contexts.

If federal regulation strengthens confidence in dollar-backed tokens, they may function as instruments of monetary influence.

Stablecoins could become:

- A digital extension of U.S. dollar hegemony

- A settlement layer for emerging markets

- A geopolitical payment tool

8. Strategic Implications for Investors and Builders

For readers seeking opportunity:

8.1 Focus Areas

- Compliant stablecoin issuers

- Infrastructure providers (custody, compliance tech, analytics)

- Tokenized U.S. Treasury platforms

- Bank-crypto integration middleware

8.2 Revenue Opportunities

- Stablecoin arbitrage across chains

- On-chain corporate settlement services

- Institutional DeFi strategies using compliant collateral

9. Conclusion: Regulation as a Catalyst, Not a Constraint

The OCC’s proposed rules under the GENIUS Act represent more than regulatory housekeeping.

They mark the institutionalization of stablecoins as a recognized financial instrument class.

While speculative yield may decline, systemic legitimacy rises.

For builders, the message is clear:

- Compliance is now a competitive advantage.

- Transparency is mandatory.

- Institutional capital is preparing to enter.

The next phase of crypto growth may not be driven by algorithmic experimentation—but by regulated digital dollars embedded into global finance.

And if projections toward a $500 billion market materialize, compliant stablecoins will sit at the center of that expansion.