Key Points :

- The American Bankers Association (ABA) challenges the White House view that banning stablecoin yields has minimal impact.

- The Council of Economic Advisers (CEA) estimates only a ~$2.1B increase in bank lending if yields are banned.

- ABA argues the real risk is deposit flight from banks if yield-bearing stablecoins are allowed.

- Stablecoin market growth toward $1–2 trillion could significantly reshape liquidity and lending dynamics.

- Regulatory frameworks like the CLARITY Act may define the future balance between crypto and traditional finance.

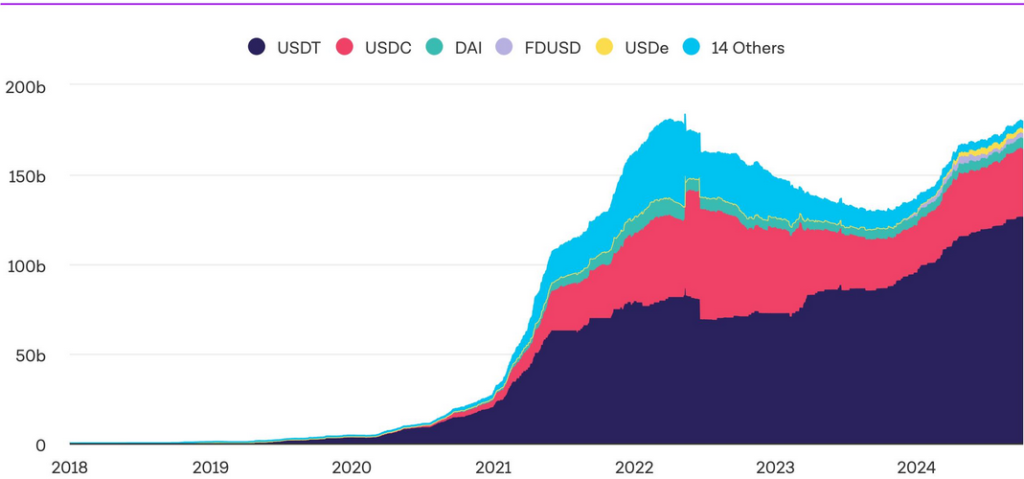

Stablecoin Market Growth Projection

1. Introduction: A Debate That Defines the Future of Money

The debate over stablecoin yields has rapidly evolved from a niche policy discussion into a defining issue for the future of global finance. At its core lies a fundamental question: Should digital dollars behave like bank deposits—or something entirely new?

In April 2026, the American Bankers Association publicly challenged a White House-backed study conducted by the Council of Economic Advisers. The study concluded that banning yield-bearing stablecoins would have only a marginal impact on traditional banking—estimating an increase of just $2.1 billion in lending, or approximately 0.02% growth.

To policymakers, this suggested that stablecoin yields are not systemically important. But to banks—especially smaller regional institutions—the conclusion misses the point entirely.

The ABA’s counterargument reframes the discussion: the real question is not what happens if yields are banned, but what happens if they are allowed at scale.

2. The White House Position: Minimal Impact, Limited Concern

The CEA’s analysis is grounded in the current state of the market. With stablecoins totaling roughly $300 billion, the report assumes that even if yield mechanisms are restricted, the reallocation of funds back into banks would be modest.

From a macroeconomic perspective, this argument is logical. Stablecoins today represent only a fraction of total bank deposits. Even aggressive regulatory changes appear unlikely to dramatically alter lending capacity in the short term.

However, this framework is inherently static. It assumes:

- Limited growth in stablecoin adoption

- Minimal behavioral change among users

- Stable relationships between digital assets and traditional banking

These assumptions are precisely what the ABA disputes.

3. The ABA Counterargument: The Wrong Question Entirely

According to ABA economists Sayee Srinivasan and Yikai Wang, the White House analysis is flawed not in its calculations, but in its framing.

The key concern is not:

“Will banning yields increase bank lending?”

But rather:

“If yields are allowed, will deposits leave the banking system?”

This distinction is critical. Yield-bearing stablecoins effectively transform digital tokens into interest-generating cash alternatives—competing directly with savings accounts.

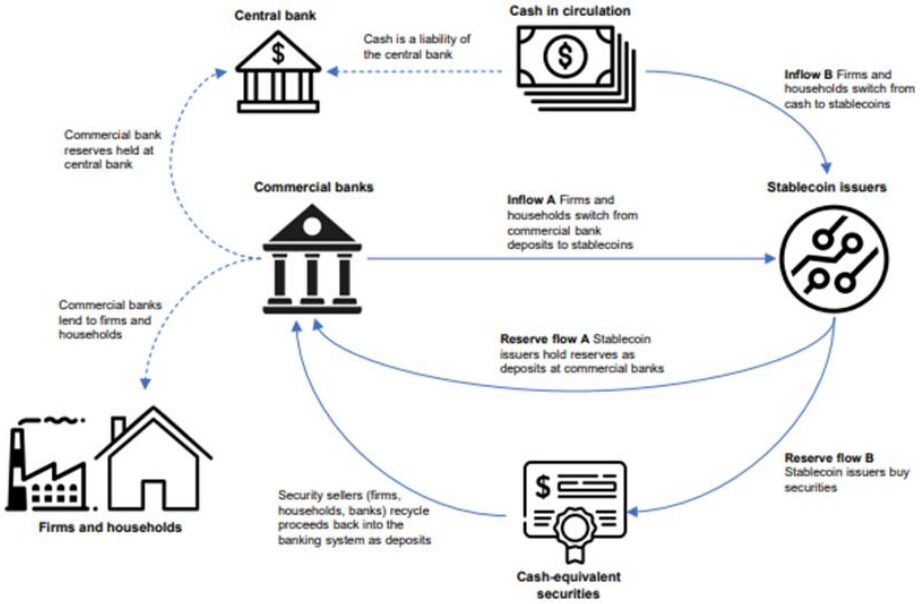

Deposit Flow Dynamics

4. The Real Risk: Deposit Flight from Community Banks

The ABA highlights a structural vulnerability: community banks.

Unlike large financial institutions, smaller banks rely heavily on local deposits to fund loans. If yield-bearing stablecoins offer higher returns with comparable liquidity, depositors may shift funds away from these banks.

This creates a cascading effect:

- Deposit Outflow → Reduced funding base

- Wholesale Borrowing → Higher funding costs

- Tighter Lending → Reduced credit availability

- Local Economic Impact → Slower regional growth

In essence, stablecoins could indirectly compress credit supply in local economies, even if national-level metrics appear stable.

5. Scaling the Scenario: From $300B to $2 Trillion

The Treasury’s projection of a $1–2 trillion stablecoin market fundamentally changes the equation.

At that scale:

- Stablecoins become a core liquidity layer

- Yield-bearing models resemble shadow banking systems

- Traditional deposit structures face direct competition

Even a modest shift—say, 10% of deposits moving into stablecoins—could represent hundreds of billions of dollars leaving the banking system.

This is where the ABA’s warning becomes most relevant: the future impact is nonlinear.

6. The Crypto Industry Perspective: Innovation and Efficiency

From the crypto sector’s standpoint, yield-bearing stablecoins are not a threat—but an evolution.

They offer:

- Programmable interest models

- Global accessibility

- Real-time settlement

- Integration with DeFi ecosystems

Platforms already demonstrate this through:

- On-chain lending protocols

- Tokenized Treasury products

- Automated yield distribution mechanisms

In this context, stablecoins are not merely digital dollars—they are financial infrastructure.

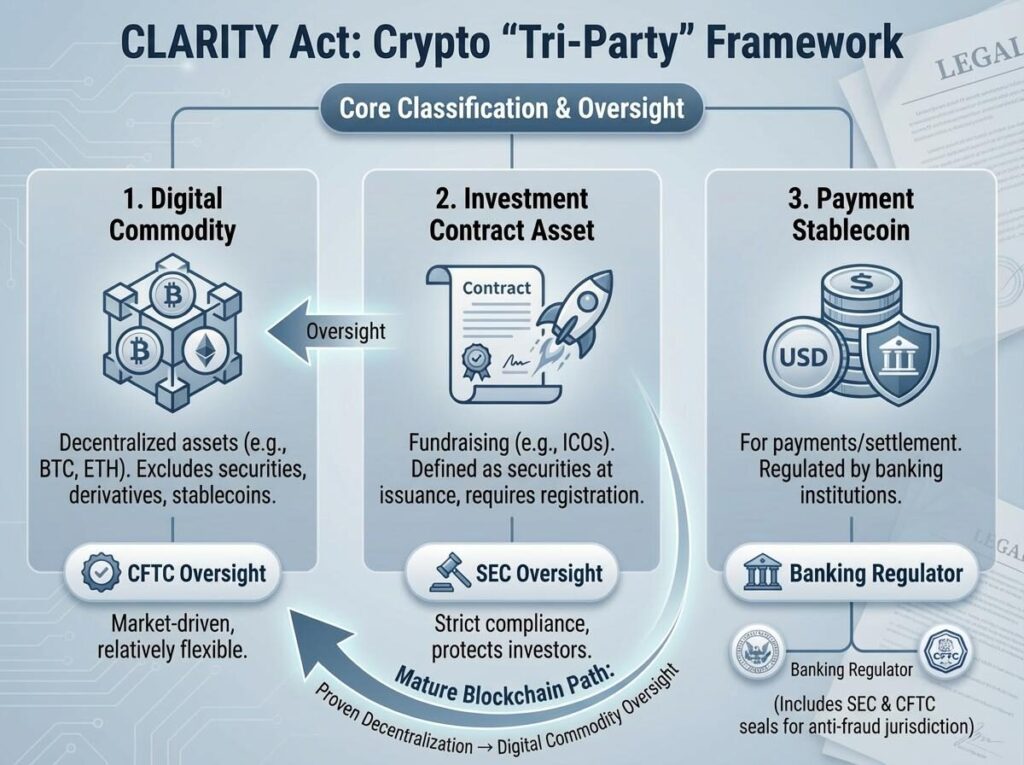

7. Regulatory Battleground: The CLARITY Act

The ongoing negotiations around the CLARITY Act represent a pivotal moment.

Key issues include:

- Whether stablecoin issuers can offer yield

- How reserves are managed and disclosed

- The classification of stablecoins (bank-like vs. securities-like)

The outcome will determine:

- The competitive balance between banks and crypto firms

- The pace of institutional adoption

- The global positioning of the U.S. in digital finance

Regulatory Impact Framework

8. Strategic Implications for Investors and Builders

For readers seeking new opportunities in crypto and blockchain applications, this debate highlights several key trends:

A. Yield as a Core Narrative

Yield-bearing stablecoins could become the default savings layer in digital finance.

B. Infrastructure Plays

Projects enabling:

- Compliance

- On/off ramps

- Risk monitoring

may see increased demand.

C. Regional Arbitrage

If U.S. regulations restrict yields, capital may flow to:

- Offshore stablecoin issuers

- Alternative jurisdictions

D. Banking-Crypto Convergence

Traditional institutions may:

- Launch their own stablecoins

- Integrate blockchain rails

- Compete directly with DeFi platforms

9. Conclusion: A Structural Shift, Not a Marginal Change

The disagreement between the ABA and the White House is more than a technical debate—it reflects two fundamentally different visions of the financial system.

The White House sees stablecoins as incremental tools within an existing framework.

The ABA sees them as transformational forces capable of reshaping deposit structures, lending markets, and economic stability.

As the market moves toward the trillion-dollar threshold, the question is no longer whether stablecoins matter—but how deeply they will redefine money itself.