Main Points :

- Taiwan targets late 2026 for the launch of its first regulated stablecoin, potentially pegged to either the NTD or USD.

- The new Virtual Asset Service Act is expected to pass the Legislative Yuan after multi-stage review, with a six-month grace period before implementation.

- The issuer of Taiwan’s stablecoin is not yet defined, though regulators strongly prefer licensed financial institutions.

- Taiwan faces a strategic decision: allow a USD-pegged stablecoin for global usability or a NTD-pegged version that may complicate capital controls.

- Political momentum grows around adding Bitcoin to Taiwan’s national reserves, reflecting global trends toward digital asset diversification by 2030.

- Taiwan’s approach attempts to balance innovation, financial stability, and regulatory clarity, signaling a maturing digital-asset environment in East Asia.

Taiwan’s Road Toward a Regulated Stablecoin in 2026

Taiwan has entered a decisive phase in its digital-asset policy evolution. Following years of cautious observation and incremental oversight, the Financial Supervisory Commission (FSC) has openly confirmed that Taiwan’s first regulated stablecoin may launch as soon as late 2026, provided the legislative and regulatory processes proceed as planned.

The FSC Chairman, Peng Jin-long, stated that the new Virtual Asset Service Act—Taiwan’s foundational legislation for digital-asset supervision—has passed the initial ministerial-level review. The bill is expected to be submitted during the current session of the Legislative Yuan. If the legislative process advances without delay, the Act may clear its third reading in the next session.

Once passed, the FSC will begin drafting subordinate regulations. Peng estimated that a six-month grace period is necessary after regulatory publication before enforcement officially begins. Based on this schedule, the earliest stablecoin launch window falls in the second half of 2026.

This marks a turning point in Taiwan’s transition toward a regulated digital-asset economy, aligning more closely with global jurisdictions pursuing clear frameworks for exchanges, custodians, and stablecoin issuers.

Regulatory Structure and the Unresolved Question of Issuer Eligibility

A critical unresolved issue is who will be allowed to issue Taiwan’s first stablecoin.

While the draft legislation does not explicitly limit issuance to banks, both the FSC and the Central Bank of Taiwan have expressed a clear preference:

stablecoins should be issued only by qualified financial institutions, not fintech startups or unregulated private entities.

This stance reflects Taiwan’s long-standing approach to risk control, especially in capital flow management, banking oversight, and anti-money-laundering compliance.

If issuance is restricted to banks and licensed e-payment operators, Taiwan’s model would resemble Japan’s 2023 stablecoin law, which similarly reserved issuance for regulated institutions.

However, this raises strategic questions for Taiwan’s competitiveness:

- Will a bank-issued stablecoin innovate fast enough to compete with global stablecoins like USDT and USDC?

- Will financial institutions be willing to assume the operational burden of real-time reserve management, audits, redemption guarantees, and cybersecurity?

These questions remain open as policymakers navigate the balance between market vitality and regulatory conservatism.

Pegging the Stablecoin: USD or NTD?

One of the most politically sensitive debates surrounding Taiwan’s planned stablecoin concerns its peg asset. Regulators have not yet decided whether the stablecoin should be backed by:

- United States Dollar (USD)

- New Taiwan Dollar (NTD)

Each option introduces distinct benefits and challenges.

USD-Peg: Internationally Friendly, Domestically Safer

- Avoids complications arising from Taiwan’s strict controls on overseas distribution of NTD.

- Simplifies banking operations and cross-border compliance.

- Aligns with global norms, where USD-pegged stablecoins dominate liquidity markets.

However:

A USD-pegged stablecoin does little to promote NTD digitalization or monetary sovereignty.

NTD-Peg: A Step Toward Taiwan’s Own Digital Monetary System

- Enhances domestic fintech innovation.

- Provides an on-chain version of NTD for payments, banking integration, and local remittances.

- Could form the basis of a future retail or wholesale digital NTD ecosystem.

However:

Taiwan has historically restricted NTD outflow to prevent unofficial offshore pricing.

A widely used NTD stablecoin could undermine these controls unless stringent limitations are implemented.

This issue remains one of the largest unresolved policy questions before Taiwan finalizes its stablecoin direction

The Emerging Debate: Should Bitcoin Become Part of Taiwan’s National Reserves?

In a parallel but related development, Taiwan’s internal political dialogue is increasingly focused on whether Bitcoin should be included in national reserves.

Legislator Ko Ju-chun raised this proposal during a public hearing in November, citing growing global uncertainty and Taiwan’s exposure to macroeconomic cycles in the United States and China.

Taiwan’s current reserve composition includes:

- Approximately 80% U.S. Treasury holdings

- Significant gold reserves

- 0% digital assets

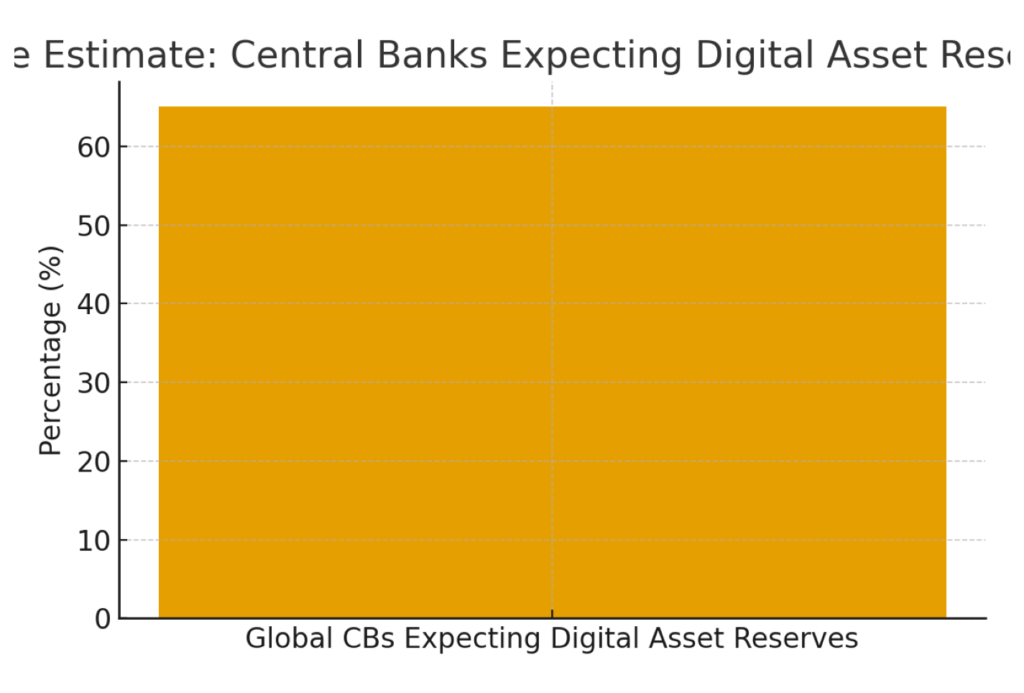

Ko argued that delaying digital-asset adoption until 2030—a timeline some global analysts anticipate for widespread central-bank crypto holdings—may leave Taiwan strategically behind.

Bitcoin’s properties as:

- a non-sovereign reserve asset,

- highly portable,

- deflationary, and

- resistant to external political pressure

make it a potential hedge against macro-financial disruption, according to proponents.

Critics, however, warn that:

- Bitcoin’s volatility may introduce unnecessary risk,

- its reserve classification is still unclear under international accounting standards,

- holding Bitcoin may provoke geopolitical sensitivity.

Regardless, Taiwan’s discussion reflects a global shift: central banks and sovereign funds are increasingly exploring small-scale allocations to digital assets to diversify risk and prepare for a more digitized financial landscape.

Regulatory Philosophy: Balancing Innovation and Financial Stability

Taiwan’s stablecoin initiative and Bitcoin-reserve debate form part of a broader national strategy:

build a clear regulatory framework for digital assets while ensuring market stability and investor protection.

Three priorities guide this approach:

1. Protecting Consumers and Preventing Misconduct

The Virtual Asset Service Act includes requirements for:

- mandatory segregation of customer and corporate assets,

- licensing for exchanges and custodians,

- transparent reserve audits for stablecoins.

2. Preserving Taiwan’s Sovereign Monetary Policy

By carefully regulating NTD-related products and offshore flows, regulators aim to maintain stability in Taiwan’s currency regime.

3. Encouraging Responsible Innovation

Taiwan intends to become a regional hub for compliant fintech innovation, particularly in:

- payments,

- programmable money,

- regulated tokenization,

- blockchain-based market infrastructure.

Unlike China’s strict prohibition model or Hong Kong’s aggressively open framework, Taiwan positions itself as a measured middle path, emphasizing clarity, licensing, and safeguards while still supporting digital-economic growth.

Market Implications for Investors and Builders

For investors seeking new opportunities, Taiwan’s regulatory advancements provide notable signals:

Stablecoin markets may open new opportunities

A regulated Taiwan-issued stablecoin—whether USD-pegged or NTD-pegged—could spark:

- new payment networks,

- regulated yield products,

- on-chain remittances,

- cross-border settlement solutions.

Institutional adoption may begin earlier than expected

If Bitcoin discussions gain traction, even a small national-reserve allocation could:

- influence regional central banks,

- legitimize sovereign digital-asset strategies,

- drive institutional capital into BTC and related infrastructure.

Regulated digital-asset providers will find a stable operating environment

Exchanges, custodians, Web3 developers, and payment companies may find Taiwan an attractive jurisdiction for:

- compliance-aligned operations,

- proof-of-reserve services,

- licensed fintech development,

- institutional partnerships.

Conclusion

Taiwan is entering a pivotal stage in its digital-asset transformation.

By moving toward a regulated stablecoin by late 2026 and engaging in national-level debate on Bitcoin reserves, the country demonstrates a clear commitment to redefining its financial future.

The decisions Taiwan makes over the next two years—particularly regarding stablecoin issuance, peg selection, and institutional adoption—will shape not only its domestic fintech trajectory but also its position within the broader Asian digital-asset landscape.

For investors, innovators, and financial institutions seeking compliant and forward-leaning markets, Taiwan is becoming a jurisdiction to watch closely.