Main Points :

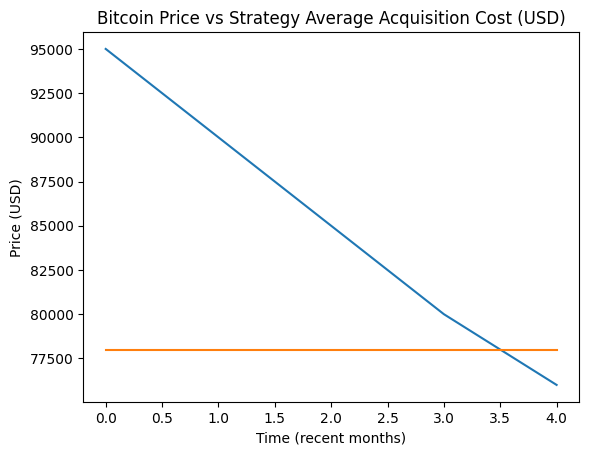

- Bitcoin briefly fell below $76,037, pushing Strategy’s average Bitcoin holdings into unrealized loss territory, but this does not translate into immediate financial distress.

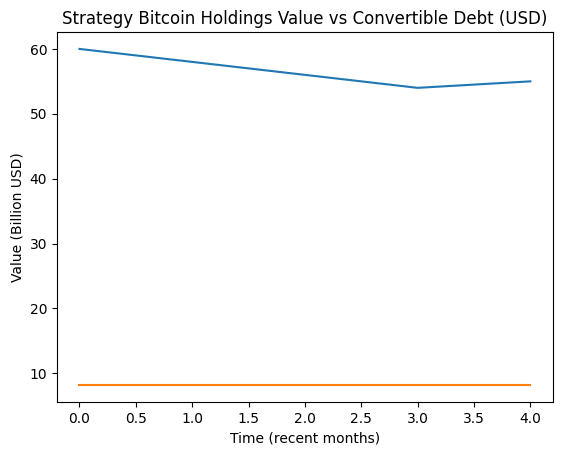

- Strategy holds 712,647 BTC, largely unencumbered and not pledged as collateral, giving it exceptional balance-sheet flexibility.

- Approximately $8.2 billion in convertible notes are structured with long maturities and strategic optionality, minimizing short-term liquidity risk.

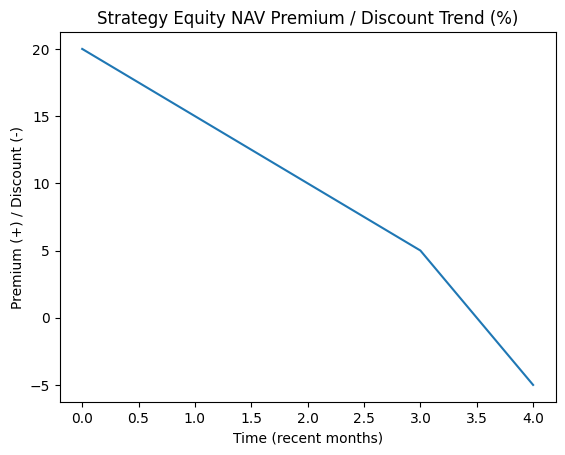

- The real pressure point is equity financing efficiency: issuing new shares to buy additional Bitcoin has become less attractive due to the stock trading at a discount to NAV.

- Broader market trends show a maturing “Bitcoin Treasury Strategy” across corporates, ETFs, and funds, reshaping how Bitcoin is used as a long-term financial asset rather than a speculative trade.

Introduction: When Unrealized Losses Don’t Mean Real Danger

In early February 2026, Bitcoin briefly dipped below $76,037, a psychologically and financially important level for corporate holders. This movement placed the massive Bitcoin treasury of Strategy—formerly known to the market as MicroStrategy—into slight unrealized loss territory.

At first glance, headlines suggesting that a company holding more than 700,000 BTC is “underwater” may sound alarming. However, a deeper examination of Strategy’s capital structure, debt maturity profile, and Bitcoin custody strategy reveals a very different picture. This is not a margin call scenario. Nor is it a forced-liquidation risk.

Instead, this moment highlights a transition phase: Bitcoin as a corporate reserve asset is no longer an experiment—it is becoming a stress-tested financial architecture.

1. Strategy’s Bitcoin Position: Scale, Structure, and Reality

1.1 The Numbers That Matter

As of early February 2026, Strategy holds approximately:

- 712,647 BTC

- Market value: fluctuating around $54–56 billion (USD-denominated)

- Average acquisition price: slightly above current spot levels

While the market price temporarily dipped below the firm’s average cost basis, this loss is unrealized. Under accounting rules, unrealized losses do not require cash outflows, margin postings, or asset sales unless specific triggers are breached—which, in this case, they are not.

1.2 Unencumbered Bitcoin Is the Key Difference

One of the most critical—and often misunderstood—points is that the majority of Strategy’s Bitcoin holdings are not pledged as collateral.

This means:

- No automatic liquidation thresholds

- No margin maintenance requirements

- No lender-driven forced sales

This structural choice separates Strategy from highly leveraged crypto firms of previous cycles. Bitcoin here functions more like digital gold in a vault, not collateral in a trading account.

2. Debt, Convertible Notes, and Why Liquidity Risk Is Low

2.1 Understanding the $8.2 Billion Convertible Note Stack

Strategy has issued approximately $8.2 billion in convertible notes across multiple tranches. Importantly:

- Maturities are staggered over several years

- Conversion prices are generally well above historical equity lows

- Notes are not directly collateralized by Bitcoin

This gives management optionality: convert, refinance, or repay depending on market conditions.

2.2 Why a Bitcoin Dip Doesn’t Trigger a Crisis

Unlike traditional leveraged structures, a decline in Bitcoin price does not automatically impair Strategy’s ability to service debt. Interest obligations are predictable, and principal repayment timelines are long.

This is a deliberate design: Bitcoin volatility was assumed from day one.

3. The Real Impact: Equity Issuance Becomes Less Efficient

3.1 NAV Discount Changes the Game

The most tangible consequence of Bitcoin’s pullback is not balance-sheet stress—it is capital efficiency.

Strategy historically used equity issuance to:

- Raise capital

- Purchase additional Bitcoin

- Increase BTC per share over time

However, when the stock trades at a discount to the value of Bitcoin per share, issuing new equity becomes dilutive.

3.2 Strategic Constraint, Not an Emergency

This does not force selling. It simply narrows future optionality:

- Fewer accretive equity raises

- More selective Bitcoin accumulation

- Greater reliance on operational cash flow or structured financing

In short, growth slows—but stability remains.

4. Broader Market Context: Bitcoin Treasury Strategy Is Maturing

4.1 From Experiment to Framework

Strategy is no longer alone. Over the past two years:

- Public companies have added Bitcoin as a strategic reserve, not a trade

- ETFs and custodial funds have normalized institutional access

- Accounting standards have improved transparency

Bitcoin treasury management is evolving into a repeatable corporate model.

4.2 Lessons from This Drawdown

This period reinforces several best practices:

- Avoid over-collateralization

- Match debt duration to long-term conviction

- Treat Bitcoin as a non-operating strategic asset, not working capital

Companies that followed these principles remain calm—even during downturns.

5. Practical Implications for Investors and Builders

5.1 For Investors Seeking New Yield Sources

- Volatility creates entry points, not automatic exits

- Treasury-style Bitcoin exposure behaves differently from spot trading

- Equity-Bitcoin hybrids require NAV-based valuation frameworks

5.2 For Blockchain Practitioners

- Corporate Bitcoin custody drives demand for:

- Multi-sig security

- Audit-friendly reporting

- Risk dashboards and treasury tools

This is a real, growing use case—not speculation.

6. Where This Leaves Strategy—and the Market

Strategy’s situation in February 2026 is not a warning sign. It is a case study in resilience.

Bitcoin can fall. Accounting losses can appear. Headlines can turn dramatic. Yet, without leverage traps or liquidity mismatches, the system holds.

This is what institutional-grade Bitcoin exposure looks like.

Conclusion: Calm in the Face of Volatility

Strategy’s unrealized losses do not signal panic—they signal design success. The company built a Bitcoin-centric balance sheet assuming volatility, not denying it.

For readers searching for:

- The next crypto opportunity

- Sustainable yield models

- Practical blockchain adoption

This episode offers a clear message: structure matters more than price.

Bitcoin as a treasury asset is no longer about hype. It is about discipline, duration, and conviction.