Main Points :

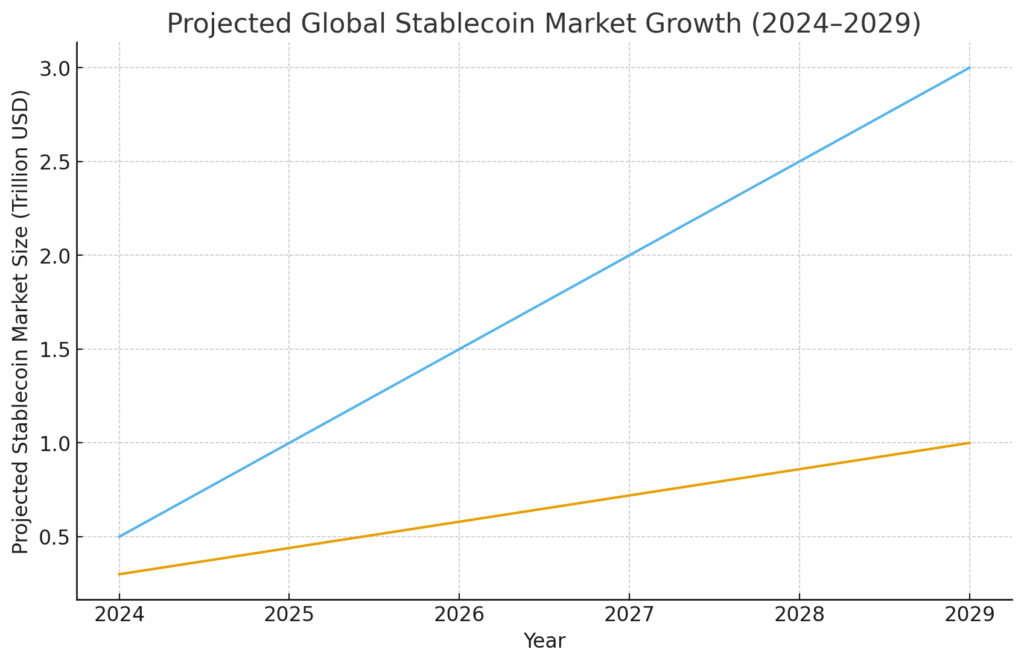

- Stablecoins may grow to $1–$3 trillion by 2029, according to internal Federal Reserve projections.

- New Fed Governor Stephen Miran warns that global demand—especially from foreign users—could materially alter U.S. monetary policy.

- Stablecoins are unlikely to drain U.S. bank deposits, but they may shift global USD demand flows.

- A global oversupply of USD-linked tokens may strengthen the dollar, influencing inflation and employment targets.

- The new U.S. stablecoin law (“Genius Act”) introduces structured oversight but prohibits interest-bearing stablecoins.

- Stablecoins may become a key pillar of U.S. financial infrastructure, accelerating global USD settlement and digital-dollar usage.

- Emerging trends show explosive adoption in Latin America, Africa, and Asia—driven by inflation, remittances, and lack of dollar banking access.

- The result: stablecoins could become the world’s largest “shadow demand engine” for U.S. Treasury assets.

1. The Federal Reserve’s New Warning Signs

When newly appointed Federal Reserve Governor Stephen Miran presented his New York policy address on November 7, he placed an unexpected topic at the center of monetary policy discussions: stablecoins. According to Miran, stablecoins—dollar-linked digital assets used globally—are no longer a niche tool for crypto traders. Instead, they represent a rapid, structural transformation in how the world accesses U.S. dollars.

Miran emphasized that Federal Reserve staff now project the global stablecoin market to expand from today’s levels to between $1 trillion and $3 trillion by 2029, driven largely by foreign users. In his words, this “cannot be dismissed as a marginal issue.” If these projections materialize, the size of stablecoin-backed U.S. Treasury holdings could rival the entire supply of short-term Treasury assets available today.

Such a development would carry vast implications. In Miran’s view, stablecoins may become a trillion-dollar external force affecting interest rates, liquidity, and the international role of the U.S. dollar.

He pointed out a striking comparison: currently, less than $7 trillion in U.S. Treasury bills are outstanding. If stablecoins generate a new $1–$3 trillion demand base, the pressure this places on Treasury markets—and the Federal Reserve’s balance sheet—could be substantial.

While these concerns are emerging only now in the U.S., other jurisdictions have already recognized stablecoins as instruments of macro-level importance. Japan, Singapore, Hong Kong, the UAE, and the EU have each positioned themselves to regulate stablecoin issuers as systematically important monetary players.

2. Why the Growth Is Driven by Foreign Users, Not Americans

Miran argues that contrary to popular belief in the banking sector, stablecoins do not meaningfully compete with U.S. bank deposits. The core reason is simple: U.S. banking customers already have access to dollar savings accounts with FDIC protection and interest-bearing products.

Instead, he argues that the majority of the demand originates from:

- regions suffering from inflation or currency instability,

- areas with capital controls,

- countries without meaningful access to U.S.-dollar accounts,

- cross-border commerce and remittances,

- crypto-native global payment rails.

In these markets, stablecoins function as synthetic offshore dollars (so-called “Euro-USD 2.0”) that enable users to store value and transfer funds at near-zero cost—without requiring approval from their local banking systems.

This forms a powerful structural trend: global users are drawing away from local currencies and rapidly shifting into USD-backed digital assets.

3. The Strong-Dollar Effect and Its Macroeconomic Implications

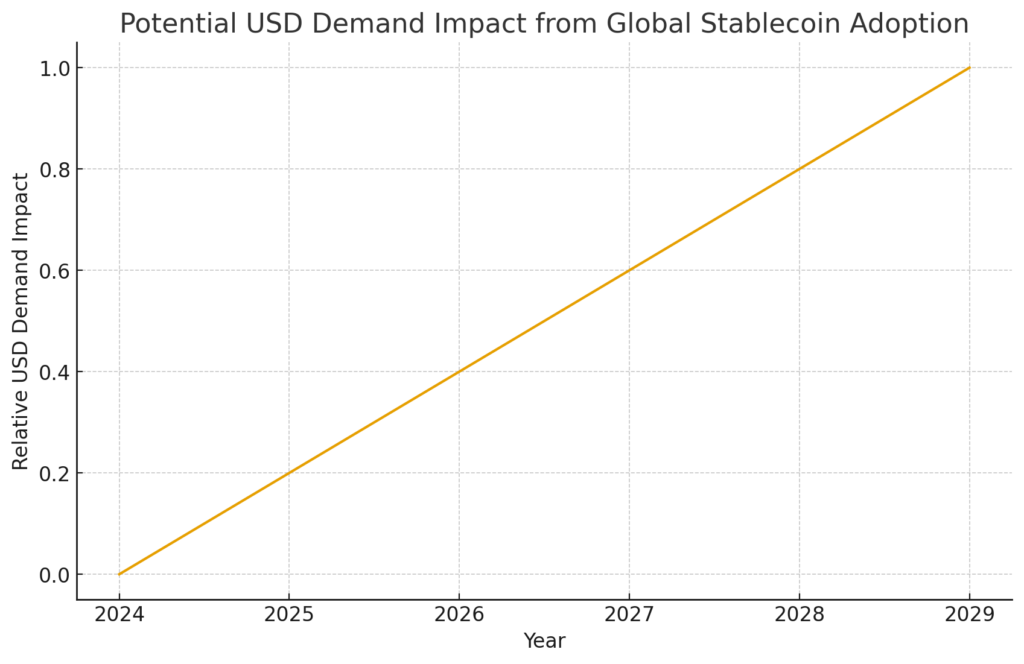

Miran highlights an important macroeconomic feedback loop: if foreign currency exits emerging markets and flows into USD-linked stablecoins, the dollar strengthens.

A stronger dollar affects:

- import prices,

- global liquidity,

- inflation targets,

- employment conditions.

Miran warns that if this stablecoin-driven USD appreciation exceeds the influence of other macroeconomic forces, the Federal Reserve may need to adjust policy more actively.

This possibility introduces an entirely new vector into monetary policy: digital-asset-driven dollar flows.

4. The Genius Act: The First Major U.S. Crypto Law

The recently enacted “Genius Act”—the first major U.S. federal law governing stablecoins—creates a framework for issuing compliant dollar-backed tokens.

Key elements:

- Stablecoins cannot pay interest directly to users, limiting their ability to compete with bank deposits.

- Issuers must only hold high-quality liquid assets, primarily U.S. Treasuries and cash.

- Monthly reserve disclosures are mandatory.

- U.S. Treasury and Fed oversight increases transparency.

- The framework invites major financial institutions to enter the market.

By prohibiting yield, the U.S. eliminates the risk that stablecoins could become a competitor to traditional savings accounts. At the same time, it positions stablecoins as a powerful new vehicle for non-U.S. users to hold digital dollars.

5. Stablecoins as the Next Generation of Financial Infrastructure

In his remarks, Miran argued that the U.S. financial infrastructure is “in need of a reboot.” He sees stablecoins as a key mechanism for enabling that modernization.

Today, global users rely heavily on stablecoins to perform:

- cross-border settlements,

- international e-commerce payments,

- gig-economy payouts,

- remittances,

- DeFi collateralization,

- dollarized savings in unstable economies.

The speed and scale of this adoption mirrors the early growth of mobile money in Africa or QR-based payments in Asia—but with USD becoming the universal settlement currency.

For the U.S., this means stablecoins may become the default global rail for distributing the dollar to billions of users.

6. The Explosive Global Adoption Trends

Beyond official forecasts, real-world adoption provides strong evidence of a massive wave forming.

Latin America (Brazil, Argentina, Venezuela)

Stablecoin usage has grown by 400–800% in three years, driven by inflationary local currencies. USDT is widely used for salaries, savings, and imports.

Africa (Nigeria, Kenya, Ghana)

A shortage of USD banking channels created one of the fastest-growing stablecoin markets in the world.

Stablecoins now account for 50%+ of crypto flows in Nigeria.

Asia (Philippines, Vietnam, South Korea)

The Philippines sees massive stablecoin demand through remittances and play-to-earn ecosystems.

Vietnam ranks among the highest in retail crypto adoption globally.

Onchain Data

USDT supply outside the U.S. has doubled in 18 months.

USDC is rapidly integrating into fintech applications, including Stripe, Visa, and major banks.

This shows that stablecoins are not a speculative crypto asset—they are a structural global monetary tool.

7. How $3 Trillion in Stablecoins Could Reshape the Treasury Market

A $3 trillion market—if backed predominantly by short-term U.S. Treasuries—would transform demand dynamics:

- Stablecoins become major non-sovereign holders of U.S. debt.

- Treasury yields may fall due to new demand.

- Government borrowing becomes cheaper.

- Short-term liquidity cycles become more sensitive to stablecoin issuance and redemptions.

This effectively turns stablecoins into a private-sector extension of the U.S. monetary base.

8. Implications for Crypto Investors and Builders

For those searching for new revenue opportunities and crypto assets with real-world utility, this shift presents several possibilities:

- Stablecoin infrastructure tokens may gain substantial demand.

- Treasury-based DeFi protocols could surge as compliant yields become standardized.

- Cross-border payment networks may rise as next-generation fintech rails.

- On-chain FX markets may emerge as stablecoins take market share from traditional remittances.

- Layer-1 and Layer-2 blockchains optimized for stablecoin settlement (Solana, Stellar, TON, etc.) may attract institution-grade flows.

- Non-custodial wallets enabling global USD access could become billion-user platforms.

Stablecoins represent one of the strongest revenue-positive ecosystems in blockchain today.

9. Conclusion

Stephen Miran’s warning may become a key turning point in U.S. monetary policy thinking. Stablecoins were once considered a niche tool for crypto traders. Today, they are becoming a global monetary engine shaping dollar demand, foreign exchange dynamics, and Treasury markets.

The U.S. now recognizes that stablecoins:

- expand dollar influence globally,

- support financial access for billions,

- modernize payments,

- and may reshape the monetary policy landscape.

Whether stablecoins reach $1 trillion or a staggering $3 trillion within this decade, their role in shaping the future of money is now undeniable.

For investors, builders, and global policymakers, this is not merely a crypto trend—it is the beginning of the next phase of the dollar’s evolution.