Key Takeaways :

- Fed Governor Christopher Waller argues that stablecoins are essential to the future of U.S. payments, positioning them alongside cash, deposits, and card networks.

- The newly enacted GENIUS Act establishes the first federal regulatory framework for payment stablecoins in the U.S., requiring full reserve backing and consumer protections.

- Waller and other Fed officials emphasize that innovation in payments should be led by the private sector under appropriate regulation.

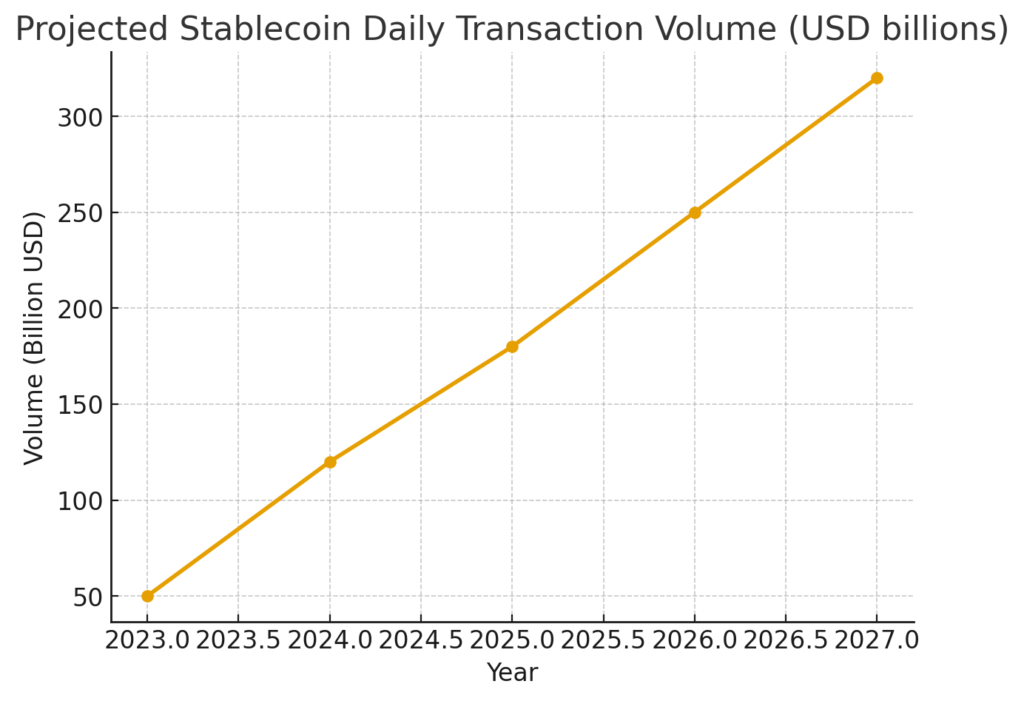

- Stablecoins may dramatically reduce payment and settlement costs, especially cross-border, and could drive ~$250 billion daily transaction volume within a few years.

- Institutional interest is rising: e.g. Visa is piloting stablecoin-based cross-border payments.

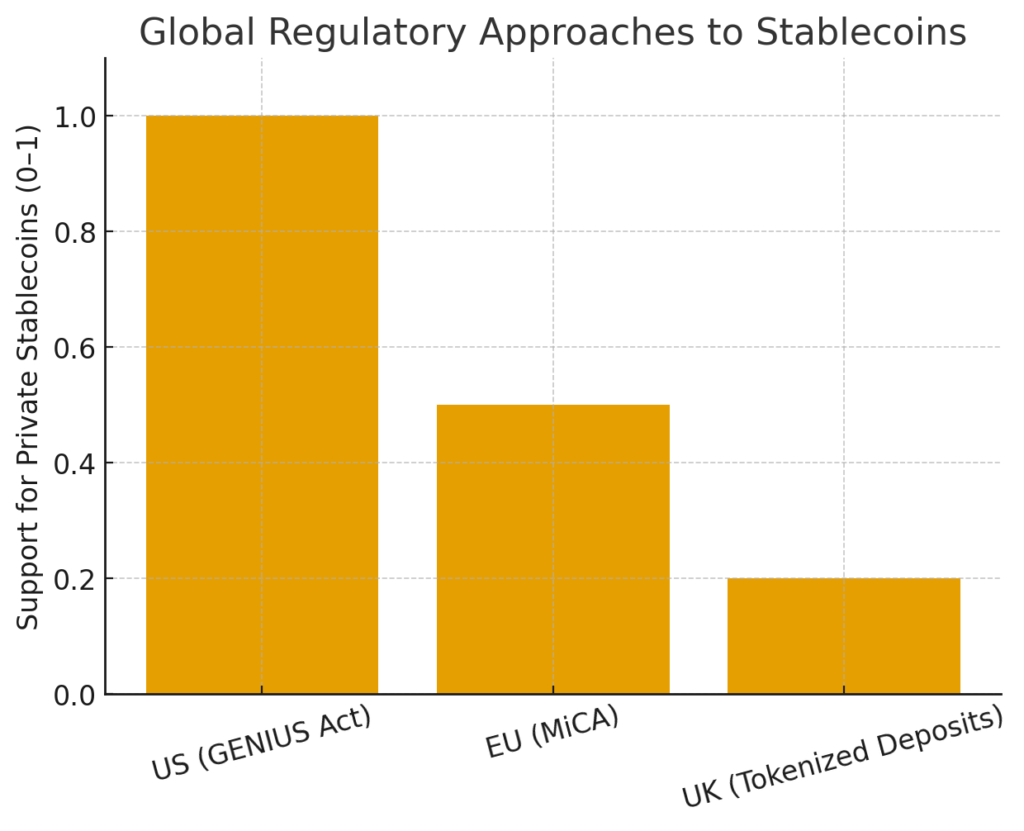

- But across the Atlantic, European and central bank officials are more cautious—some are pushing for central bank digital currencies or “tokenized deposits” instead of private stablecoins.

1. Waller’s Vision: Stablecoins as a Legitimate Payment Medium

During the Sibos 2025 conference in Frankfurt, Federal Reserve Governor Christopher Waller delivered a keynote that underlined a bold vision: stablecoins are not a fringe crypto experiment but a new form of private money that should coexist with cash, deposits, and card networks—so long as they earn consumer trust through safety and regulation.

Waller stressed that if stablecoins can deliver lower-cost, higher-speed payments, then the Fed is “all in.” He likened them to card payments: they too are innovations of the private sector integrated into the broader payments, clearing, and settlement infrastructure.

He also emphasized that innovation drivers should come from private sector efforts rather than being centrally mandated, while the Fed and regulatory bodies play a supporting role.

This is a striking shift in tone: historically, central banks have been skeptical of private money-like instruments, wary of monetary control and systemic risk. Waller’s remarks suggest a more accommodating posture—conditional on stability, transparency, and oversight.

2. GENIUS Act: The U.S. Steps into Stablecoin Regulation

Origins and Purpose

In July 2025, President Donald Trump signed into law the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act), making it the first federal statute to provide a comprehensive legal and regulatory framework for payment stablecoins in the United States.

Until now, stablecoin regulation in the U.S. has been fragmented, falling partly under banking, securities, money transmission, or state-level licensing. The GENIUS Act consolidates and clarifies roles, laying down rules for issuance, reserves, consumer protection, and oversight.

Core Requirements and Protections

Some of the key features of the Act include:

- 100% reserve backing: Payment stablecoins must be backed one-for-one with liquid assets (U.S. dollars or short-term U.S. Treasuries).

- Monthly public disclosure: Issuers must publicly disclose reserve composition to promote transparency.

- Consumer protection and anti-misrepresentation rules: Issuers cannot claim their stablecoins are insured by the U.S. government or are legal tender.

- Hierarchy of claim priority: In the event of issuer insolvency, stablecoin holders’ claims have priority over other creditors.

- Regulatory alignment: State and federal regulation are aligned; small issuers under $10 billion in outstanding stablecoins can follow state-level regimes if substantially similar to the federal framework.

- Issuance eligibility and licensing: Only “permitted” payment stablecoin issuers may issue stablecoins. Nonbanks must be federally licensed.

- Rulemaking timeline & oversight roles: The Act empowers regulators to issue rules and jointly supervise state-level and federal-level issuers.

Agencies like the Office of the Comptroller of the Currency (OCC) are expected to assume oversight over nonbank issuers, and the Act expands the OCC’s authority accordingly.

Limitations and Transition

- The Act explicitly states stablecoins cannot be backed by the full faith and credit of the U.S. government, or be misrepresented as deposit insurance–protected.

- Issuers crossing $10 billion in aggregated supply must transition to full federal oversight within a year or pause new issuance.

- The Act takes effect either 18 months after enactment or 120 days after final implementing regulations are issued (whichever comes first).

In sum, the GENIUS Act attempts to bring legal certainty to stablecoin issuance and operations in the U.S., promoting both growth and guardrails.

3. The Use-case Pull: Payments, Settlement, and Cross-Border Potential

Cost and Efficiency Gains

One of the strongest use cases for stablecoins is reducing cost and latency in payments, especially across borders. Waller highlighted that blockchain-based settlement could lower costs for both consumers and enterprises.

In support of this, McKinsey has estimated that at current growth rates, daily stablecoin transaction volumes could hit $ 250 billion in coming years—surpassing volumes in legacy card networks—particularly for high-efficiency and cross-border use cases.

Institutional Adoption

Reflecting growing institutional confidence, Visa announced a pilot to use stablecoins for cross-border payments. Under this model, businesses pre-fund tokens for transaction settlement, potentially streamlining capital flows.

Meanwhile, global financial infrastructure providers respond. For example, Swift is now exploring its own blockchain to support tokenized payments, including stablecoins, enabling cross-border rails with smart contract validation and ledger transparency.

These signs point to stablecoins being woven into the plumbing of global payments and finance—not just used by retail or crypto-native actors.

4. Risks, Challenges & Counterpoints

Financial Stability and Monetary Policy

One major critique of private stablecoins is their potential to undermine central banks’ control over money supply and destabilize monetary policy. Eurozone officials, notably Bundesbank’s Joachim Nagel, have voiced such concerns, warning of “systemic risks” and the erosion of central bank sovereignty if private stablecoins become dominant.

Waller’s argument is that with appropriate regulation (i.e. full reserve, transparency, priority of claims), many systemic risks can be mitigated.

Regulatory Overreach & Innovation Chilling

Overly heavy-handed regulation could stifle innovation. Waller and others have made it clear: regulation must be “right-sized.”

Still, critics argue that insisting on 100% backing, rigid compliance rules, and heavy licensing could deter smaller or experimental players from entering the space.

Operational and Counterparty Risks

Even with full reserves, questions remain: how liquid are those reserves? How are they audited? What happens under extreme market stress? Some stablecoin failures (e.g. algorithmic collapses) exposed hidden fragility in reserve mechanisms.

Additionally, stablecoin issuers are exposed to operational risk (e.g. software bugs, smart contract exploits), and counterparty risk in banking or custody relationships.

Regulatory Cross-border Friction

Because finance is global, inconsistent regulation between jurisdictions may create arbitrage or compliance friction. The U.S.’s embrace of private stablecoins (via GENIUS Act) contrasts sharply with Europe’s orientation toward CBDCs or tokenized deposits.

5. Trends and Developments Beyond the Waller Speech

Tether’s Plan for USAT

Tether, issuer of the dominant USDT, announced it will launch a U.S.-based stablecoin named USAT, to comply with GENIUS frameworks. Issuance is expected via Anchorage Digital Bank, a chartered U.S. trust bank.

This signals how large-scale stablecoin issuers are preparing to adapt to new regulatory landscapes and internalize compliance. USAT is not planned to offer yield, aligning with conservative reserve-backed stablecoin models.

Euro-area Banks Launching Euro-denominated Stablecoin

In reaction to U.S. momentum, nine European banks (including ING and UniCredit) recently announced a joint venture to issue a euro-denominated stablecoin, with targeted launch in H2 2026. The project intends to operate under EU’s MiCA regulatory regime.

This marks a push to preserve European monetary autonomy and reduce dependence on dollar-based private stablecoins.

Tokenized Deposits in the UK

In the UK, major banks (HSBC, NatWest, Lloyds, Barclays, Nationwide, Santander) are pushing ahead with tokenized deposits slated for rollout in 2026. This is seen as an alternative to stablecoins, maintaining integration with traditional banking.

Governor Bailey and the Bank of England have signaled preference for tokenized banking deposits rather than private stablecoins, to avoid money leaving regulated bank systems.

6. Implications for Crypto Investors, Builders, and Enterprises

For New Crypto Projects & Tokens

- Stablecoin-backed tokens (e.g. utility or governance tokens issued atop a stablecoin base) now stand on firmer legal ground in the U.S. with the GENIUS Act.

- Projects might focus more on real-world asset tokenization (e.g. tokenizing bonds, real estate), using stablecoins as a programmable settlement layer.

- There’s growing importance of reserve transparency, auditability, and aligning with regulatory frameworks to attract institutional adoption.

For Payment & Fintech Businesses

- Integration of stablecoins into payment rails may cut costs and improve global reach. Visa’s pilot is a case in point.

- Companies can consider issuing or facilitating stablecoin flows (e.g. wallets, settlement services) under the new U.S. regulatory clarity.

- For cross-border remittance or B2B settlement, stablecoins may displace parts of correspondent banking.

For Enterprises & Blockchains

- Blockchains could see increased demand as settlement backbones for tokenized commerce and stablecoin-mediated value transfer.

- Enterprise solutions might build hybrid systems: stablecoin rails for liquidity, traditional rails for fallback or settlement.

For Investors

- Stablecoin projects and infrastructure startups (exchanges, custody, auditing) may become attractive targets in this newly legitimized space.

- Compliance, regulatory alignment, and reserve practices will become key metrics to evaluate stablecoin projects.

Conclusion

Christopher Waller’s recent remarks and the passage of the GENIUS Act mark a turning point in how stablecoins are perceived: no longer fringe curiosities, but foundational infrastructure for modern payments. The U.S. is moving toward legitimizing private stablecoin issuance under guardrails, setting a precedent that could unlock enormous value in payments, settlement, remittance, and tokenized commerce.

Yet, challenges remain. The balance between regulation and innovation is delicate. Europe is pushing back with CBDCs and tokenized deposits. Operational and liquidity risks must be managed. And cross-border regulatory alignment is still a work in progress.

For entrepreneurs, developers, and investors in crypto and blockchain, stablecoins are now a signal worth heeding—not just as a bridge currency, but as a core component of next-generation financial systems. Under the right regulatory and technical foundations, stablecoins may indeed become the backbone of global payments in the years ahead.