Main Points :

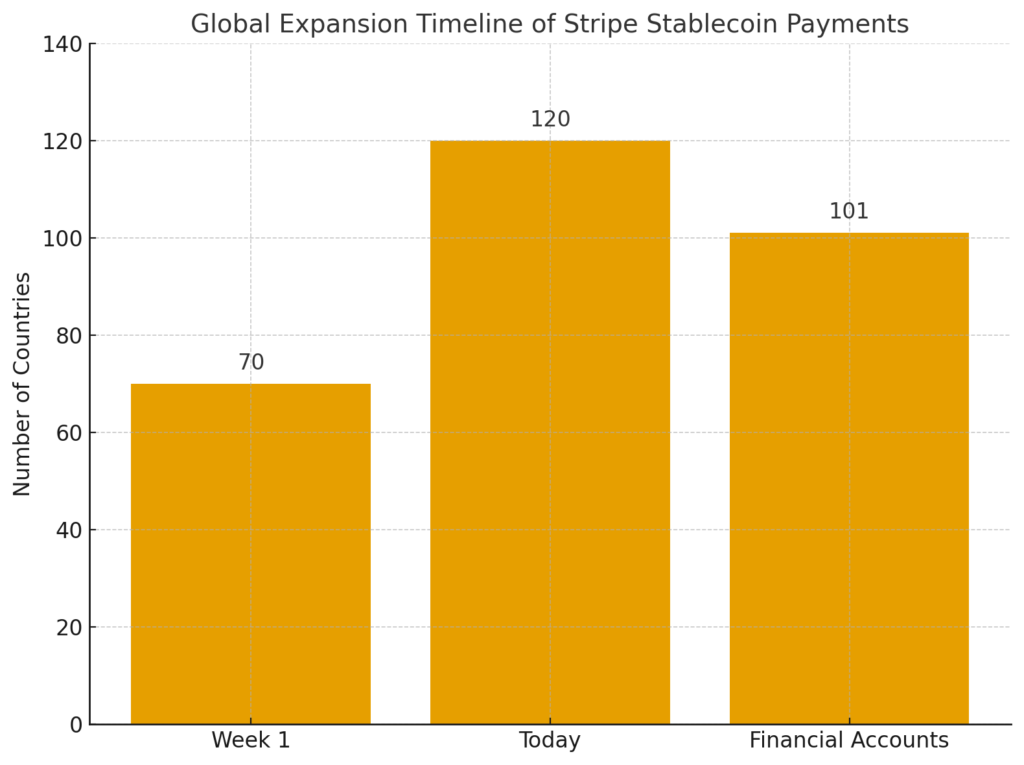

- Stripe’s Bridge-powered stablecoin payments reached 70 countries in the first week and now span 120 countries.

- Growing use cases: Remitly for remittances; Remote for payroll in 68 countries.

- Stripe launched Stablecoin Financial Accounts in 101 countries, enabling holding, receiving, and sending USDC and USDB.

- Strategic acquisitions: Bridge (US$1.1B, Feb 2025) and Privy wallet provider.

- Visa partnership: stablecoin-linked Visa cards in Latin America and expansion planned globally.

- Stripe and Paradigm released Tempo, a high-throughput payments-focused Layer-1 blockchain with partners like Visa, Shopify, OpenAI, Deutsche Bank.

- Critics warn of centralization risks and echo concerns from Libra’s legacy.

- Stablecoin ecosystem backed by regulatory shifts: U.S. GENIUS Act, EU MiCA, Hong Kong Bill.

- Academic research supports stablecoins as “Banking 2.0,” hybrid fiat-private monetary systems.

1. Rapid Global Reach via Bridge

Recently, Stripe CEO Patrick Collison and other executives highlighted staggering global uptake of stablecoin payments after leveraging Bridge’s infrastructure. Within just the first week of launch, Stripe enabled transactions from 70 countries, which have since expanded to 120 countries.

2. Real-World Use Cases

Several leading companies are already deploying stablecoin payments:

- Remitly uses USDC via Bridge for seamless international remittances.

- Remote, a global hiring platform, pays contractors in 68 countries using USDC, with client adoption doubling month over month.

3. Stablecoin Financial Accounts

In May 2025, Stripe introduced Stablecoin Financial Accounts, now available in 101 countries. These accounts allow businesses to hold balances in USDC and USDB, receive amounts via fiat (ACH, SEPA) or crypto, and send stablecoins globally—facilitating treasury operations and inflation hedging for users in volatile regions.

4. Strategic Acquisitions Powering Expansion

Stripe completed its acquisition of Bridge for approximately US$1.1 billion in February 2025, marking its most significant fintech acquisition to date. Later, it acquired crypto wallet provider Privy, further bolstering its stablecoin payment infrastructure.

5. Visa Partnership: Bridging Crypto and Everyday Purchases

Stripe’s Bridge is now powering stablecoin-linked Visa cards in Latin America—offered in Argentina, Colombia, Ecuador, Mexico, Peru, and Chile—with expansion into Europe, Africa, and Asia forthcoming. Bridge handles the backend conversion from stablecoin holdings to local currency at the point of sale.

6. Tempo: A Blockchain Built for Payments

On September 4, 2025, Stripe and Paradigm unveiled Tempo, a new Layer-1 blockchain optimized for stablecoin payments. It’s being developed with partners including Visa, Deutsche Bank, Shopify, Revolut, Nubank, OpenAI, and Anthropic; Tempo aims to support very high-throughput, low-latency payment workflows. Stripe’s CEO described it as a payments-first blockchain essential for global businesses.

7. Centralization Critiques: Lessons from Libra

However, not all reactions are rosy. Christian Catalini, co-creator of Meta’s Libra/Diem, compared Tempo—and Circle’s Arc—to past centralized crypto initiatives, warning that they risk reviving financial hierarchies under new corporate leadership, potentially sidelining decentralization ideals.

8. Regulatory Frameworks Fueling Adoption

Stablecoins are backed by a growing ecosystem of regulation:

- In the U.S., the GENIUS Act, passed in July 2025, enables banks and institutions to issue fiat-backed stablecoins, propelling stablecoin issuance.

- In the EU, the MiCA regulation (effective mid-2024) governs stablecoin issuance and trading.

- Hong Kong passed its Stablecoins Bill in mid-2025, with issuance licenses expected in early 2026.

9. Stablecoins as “Banking 2.0”

Academic research underscores stablecoins’ transformative potential:

- “Banking 2.0” redefines global finance by merging crypto programmability with fiat trust—addressing fragmentation, fraud, and latency in legacy systems.

- A hybrid monetary model, where stablecoin issuers are backed with central bank reserves, offers scalable, resilient infrastructure for cross-border digital payments.

- Another study highlights stablecoins’ role in real-world asset tokenization and presents frameworks for performance evaluation and governance.

10. Conclusion: A New Era for Global Payments

Stripe’s aggressive push into stablecoin infrastructure—through the Bridge acquisition, global product launches, Visa integrations, and the Tempo blockchain—signals a tectonic shift in how money moves across borders. For businesses and developers exploring novel digital revenue streams or practical blockchain applications, Stripe’s suite of tools offers an unprecedented combination of programmability, scale, and regulatory alignment. Yet, as corporatized blockchains rise, balancing innovation with decentralization principles—and remaining watchful of centralizing trends—is vital. Stablecoins are redefining the frontier of digital finance. End of English article.