Main Points :

- The Financial Services Commission (FSC) of South Korea ordered a suspension of new crypto lending services at domestic exchanges, effective immediately.

- Existing loans remain active: borrowers may repay or extend under current terms, but no new lending is permitted.

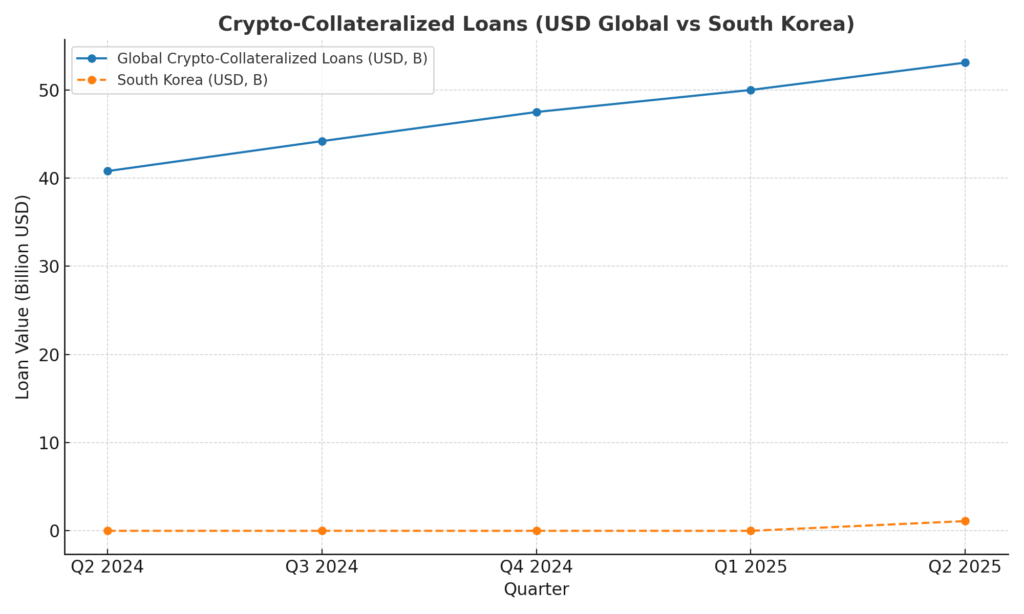

- Over roughly one month, about 27,600 users borrowed ₩1.5 trillion (~$1.1 billion); approximately 13% were liquidated due to price volatility.

- The FSC flagged unusual sell pressure on USDT, causing temporary deviations from the usual $1 peg, signaling systemic market risk.

- The lending boom occurred in a regulatory gray zone—lacking clear rules or licensing regimes.

- A new joint task force between the FSC and Financial Supervisory Service (FSS) is crafting formal guidelines, likely covering leverage limits, risk disclosures, and user eligibility.

- Analysts argue for safer expansion with better disclosures and controls, not a blanket shutdown.

- Simultaneously, regulatory direction is enabling broader crypto integration—such as spot crypto ETFs, won-pegged stablecoins, and institutional custody services.

- The FSC’s suspension is framed as a temporary “circuit breaker” to stabilize markets and protect investors amid new regulatory clarity.

Why the Suspension Is Unprecedented

South Korea’s Financial Services Commission (FSC) delivered a sweeping directive on August 19, 2025, instructing all domestic crypto exchanges to cease offering new lending products immediately. While not an outright ban, this forced pause signals deep regulatory concern. Existing loans are untouched—borrowers can repay or extend—but platforms are prohibited from issuing any new credit. Non-compliance may trigger on-site inspections, audits, and potential penalties.

Lending Frenzy and Liquidation Shockwaves

A dramatic burst of lending began in early to mid‑July. Upbit allowed loans up to 80% collateral value, accepting Bitcoin, XRP, or USDT as guarantees, while Bithumb extended loans up to 4x the users’ assets. In just one platform’s first month, about 27,600 users borrowed ₩1.5 trillion, around $1.1 billion. Market swings caused about 13% of those borrowers (around 3,600 people) to face forced liquidation due to collateral devaluation.

Stablecoin Stress Test

The FSC also flagged an unusual sell-off in USDT lending, which led to temporary de‑pegging of Tether from its $1 norm—an uncommon occurrence. This volatility highlighted that even ostensibly stable instruments like USDT can disrupt the market under stress, raising alarm bells for regulators about cascading effects ﹙stablecoins’ volatility risking broader instability﹚.

Regulatory Gray Zone and Institutional Momentum

Despite previous efforts—like the Virtual Asset User Protection Act in 2023 and AML mandates—the crypto lending sector remained largely unregulated, operating in a legal gray zone without firm licensing or operational standards. Yet, South Korea is also pushing toward greater crypto integration: plans include spot crypto ETFs, a won-pegged stablecoin, institutional custody services, and the legislative push of a Digital Asset Basic Act to establish long-term authority over lending products.

What Comes Next: Building the Framework

The FSC and the Financial Supervisory Service (FSS) formed a joint task force on July 31 to build a comprehensive regulatory framework for crypto lending. The forthcoming guidelines are expected to address:

- Leverage limits

- Mandatory risk disclosures

- Borrower eligibility criteria

- Transparency and reporting requirements

- Oversight and monitoring protocols

These guidelines aim to strike a balance between supporting innovation and ensuring investor protection.

Debate: Shutdown vs. Structured Reform

Some industry experts—including Bradley Park of DNTV Research—argue that upgrading user interfaces, improved disclosures, and implementing adequate LTV (loan-to-value) controls would have addressed risks more proportionately than a full suspension. The argument suggests the real concern may lie in market opacity—e.g., Upbit’s lending scale remains undisclosed—making oversight harder.

Industry Pivot Amid Regulatory Scrutiny

Although lending services face a halt, the broader crypto ecosystem in South Korea is evolving into a more regulated and institutional-ready environment. Dunamu (Upbit operator) launched institutional custody services, and authorities are drafting the Digital Asset Basic Act to formalize lending and broader market regulation. Concurrently, movement toward spot ETFs and stablecoin frameworks signals openness to regulated digital asset innovation.Insert Graph or Chart Here

【Suggested Graph: A line chart showing “Crypto-Collateralized Loans (USD, Global)”—highlighting Q2 2025 surge to $53.1 billion (30% increase) per Galaxy Digital report, and overlaying South Korea’s $1.1 billion lending boom for local context (compare against global scale).**]

Please place this graph right after the subheading “What Comes Next: Building the Framework.”

Summary and Final Thoughts

South Korea’s decision to freeze new crypto lending services reveals both the volatility of emerging crypto markets and the urgent need for regulatory clarity. The lending craze—driven by aggressive leverage products—mor strayed into murky legal waters and triggered direct harm to borrowers via mass liquidations and unstable stablecoin dynamics.

By halting lending, the FSC inserted a much‑needed pause, allowing time to formalize clear rules that ensure responsible innovation rather than outright suppression. This measured but firm response positions South Korea as a regulatory pioneer, committed to safeguarding investors while enabling the digital asset sector’s evolution.

Moving forward, the success of this approach will hinge on:

- The speed and quality of guideline delivery

- The effectiveness of oversight in enforcing new standards

- The market’s acceptance of a safer, more transparent lending infrastructure

- The growth of institutional and retail confidence under this new regulatory clarity