Main Points :

- SoFi becomes the first nationally chartered U.S. bank to offer crypto trading under clarified OCC/FDIC guidelines.

- A major shift: traditional banking opens fully regulated access to digital assets.

- SoFi re-enters crypto after exiting in 2023 due to licensing requirements.

- The bank plans to issue a fully backed stablecoin “SoFi USD,” entering the stablecoin settlement market.

- This move may accelerate institutional adoption, raise compliance standards, and reshape consumer crypto access.

- For investors: new revenue opportunities emerge around regulated retail crypto, bank-issued stablecoins, and compliance-native fintech.

1. Introduction — A Turning Point for Crypto in U.S. Banking

In November 2025, SoFi Technologies, a U.S.-based fintech and nationally chartered bank, officially became the first national bank in American history to provide retail cryptocurrency trading under the clarified guidelines issued by the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC). This milestone marks a major shift in the relationship between regulated banking and digital assets, representing a new era where crypto is no longer confined to exchanges, neobanks, or unregulated platforms. Instead, it is now embedded directly within the core infrastructure of U.S. financial institutions.

The event is widely viewed as a signal that U.S. regulators—after years of ambiguity—have defined a clear operational boundary for banks who wish to store, execute, or settle digital assets. For investors looking for new opportunities in emerging cryptocurrencies, yield-generating models, or blockchain-based remittances, SoFi’s re-entry into crypto marks the beginning of a new competitive phase.

CEO Anthony Noto described the moment as:

“SoFi is the first nationally chartered bank where consumers can buy, sell, and hold cryptocurrencies.”

From a compliance perspective, this shift also indicates the normalization of digital assets within the prudential supervision of federal banking standards, including AML/KYC, capital controls, liquidity monitoring, and risk frameworks.

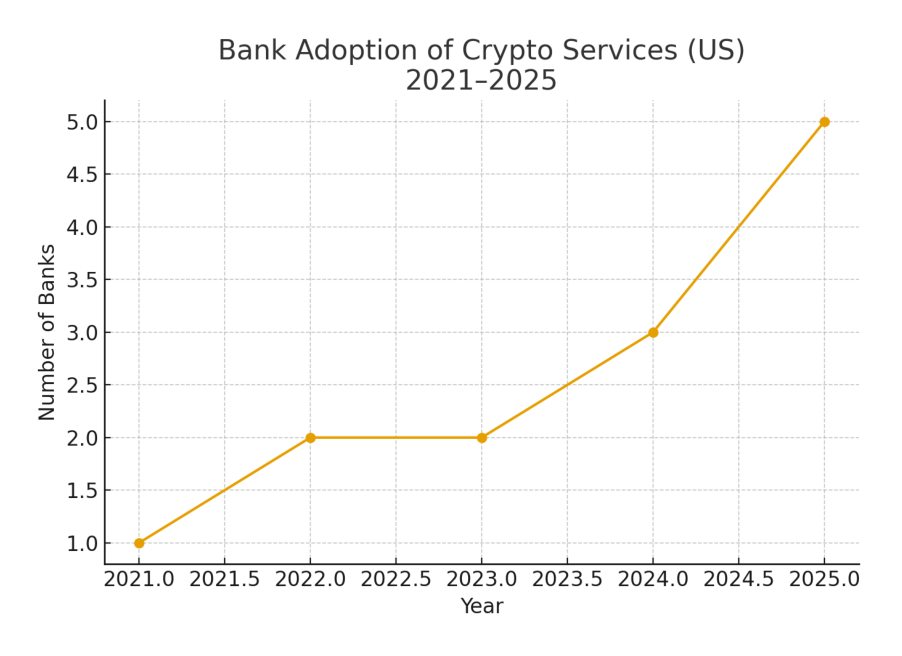

2. Why SoFi’s Move Matters — Banking Enters the Crypto Era

2.1 Regulatory Approval Signals a New Consensus

For years, U.S. regulators struggled to find a balance between innovation and risk. The uncertainties made many banks avoid offering digital asset services.

This changed in May 2025 when:

- OCC formally confirmed that U.S. banks may provide crypto custody and execution services.

- FDIC aligned its instructions, allowing insured banks to support crypto activities under appropriate controls.

This created a legally solid framework: banks can now treat crypto as another financial service—just like deposits, payments, lending, or wealth management.

SoFi is the first, but it will not be the last. Industry analysts expect more banks to follow, particularly those seeking to compete with Coinbase, PayPal, Cash App, Robinhood, and major exchanges.

The result?

A new wave of retail crypto adoption supported not by startups, but by tightly regulated financial institutions.

3. From Exit to Re-Entry — SoFi’s Crypto Timeline

3.1 Withdrawal in 2023

In its early days, SoFi provided crypto trading inside its mobile app.

But when applying for a national banking charter, regulators required it to discontinue crypto activity until licensing was complete.

SoFi exited crypto in 2023 due to:

- compliance requirements for national charter approval

- strict oversight on consumer investment products

- review of digital asset risk exposures

3.2 Conditions Change in 2025

In March 2025, the OCC adopted a more flexible posture to digital asset participation.

This opened the door for SoFi’s re-entry.

By June 2025, SoFi expanded further into blockchain infrastructure by launching:

- fiat-to-crypto conversion services

- blockchain-powered international remittances

- faster cross-border settlement rails

This allowed SoFi to integrate blockchain deeply into its payment and lending systems—moving from “crypto trading” to crypto-native financial architecture.

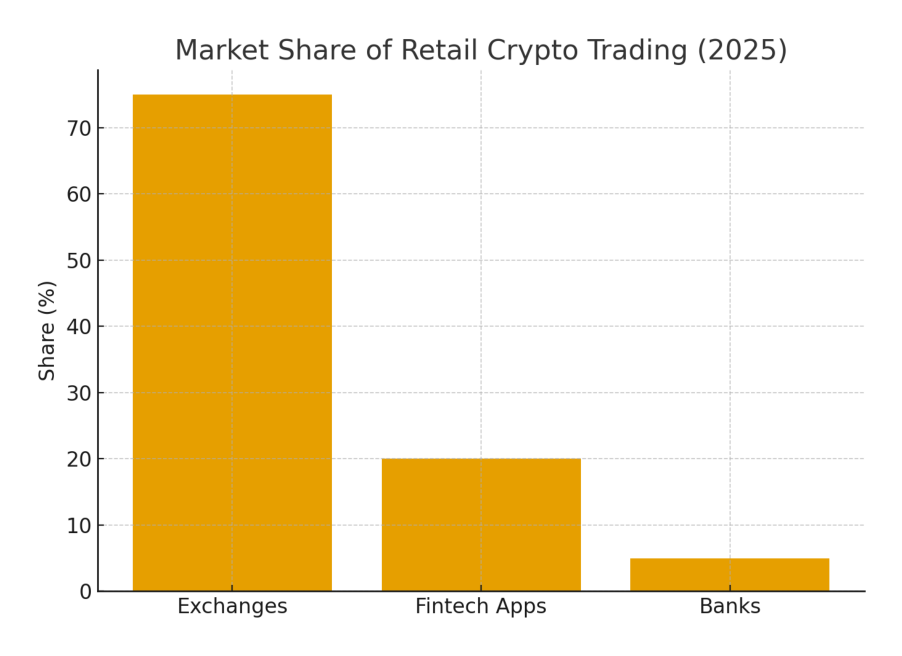

4. What SoFi Now Offers — Consumer Crypto Trading at Bank Level

4.1 Supported Assets

Customers can now trade dozens of cryptocurrencies, including:

- Bitcoin (BTC)

- Ethereum (ETH)

- Other major market assets

Full access will roll out to all customers over the following weeks.

As a bank, SoFi provides an advantage over exchange-only platforms:

- Federal oversight

- Strong AML/KYC and transaction monitoring

- Custody under banking-grade compliance

- FDIC-insured fiat accounts (not crypto, but surrounding liquidity)

This strengthens consumer protections compared with typical crypto exchanges.

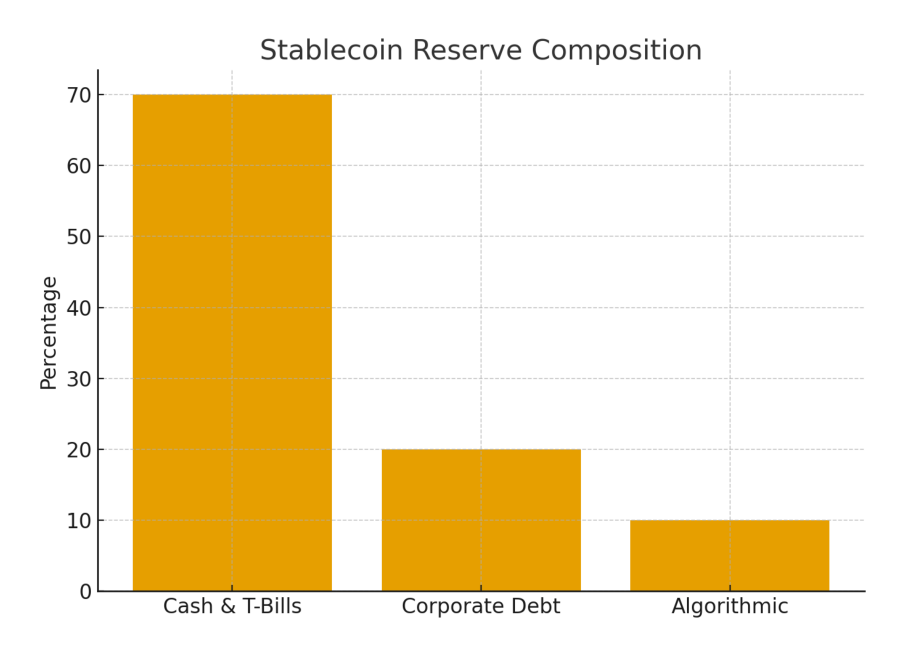

5. SoFi USD — A New Fully Backed Stablecoin

One of the most important components of SoFi’s roadmap is the development of a fully reserved stablecoin, SoFi USD.

This positions SoFi alongside:

- PayPal (PYUSD)

- Circle (USDC)

- Gemini (GUSD)

- And potentially future bank-issued stablecoins

5.1 Why This Matters

Stablecoins generate:

- settlement fee revenue

- remittance opportunities

- liquidity pool integration

- digital payments utility

- yield from underlying reserves

With SoFi’s national bank charter, SoFi USD may become one of the most compliant stablecoins ever issued in the United States.

5.2 Noto’s Warning About Non-Bank Stablecoins

CEO Anthony Noto emphasized concerns:

“Even if a stablecoin claims to be backed 1:1, that doesn’t guarantee the issuer always has the dollars on hand during redemption.”

He cited risks related to:

- liquidity shortages

- duration mismatches

- credit exposure in backing assets

This indirectly warns against non-bank stablecoin issuers susceptible to bank runs.

6. Market Impact — What This Means for Crypto Investors

6.1 Acceleration of Institutional Adoption

SoFi’s entry will pressure competing banks to enter digital asset services.

This may accelerate mainstream adoption of:

- crypto trading

- stablecoin payments

- tokenized deposits

- bank-issued digital assets

6.2 New Opportunities for Investors

For readers seeking new revenue streams, opportunities include:

- early-stage tokens positioned for bank integration

- yield strategies built around stablecoin liquidity

- cross-border payment tokens and Layer-2 rails

- compliance-native blockchain infrastructures

6.3 Rising Demand for High-Compliance Tokens

Tokens with strong compliance characteristics may benefit, including:

- KYC-friendly payment coins

- enterprise-use tokens

- tokenized treasury assets

- remittance-oriented blockchains (XLM, XRP, etc.)

For builders and investors in real-world blockchain utility, SoFi’s move validates the market direction: regulated, integrated, interoperable crypto.

7. Broader Trends — How Other Institutions Are Moving

SoFi’s action aligns with a global trend:

- Hong Kong authorizes licensed crypto exchanges

- UK tightens FCA crypto promotion rules

- Japan expands Web3 investment rules

- EU launches MiCA regulatory standards

- Singapore continues a licensing-first approach

Across the world, the theme is clear:

Regulatory clarity drives institutional participation.

SoFi is the U.S. prototype for this shift.

8. Conclusion — The Beginning of Bank-Integrated Digital Finance

SoFi becoming the first nationally chartered U.S. bank to offer crypto trading is more than a historical milestone.

It represents a structural shift where digital assets transition from an alternative financial system into the core regulated banking sector.

This development unlocks:

- stronger consumer protection

- deeper liquidity

- compliance-strengthened innovation

- scalable blockchain-based payments

- and entirely new revenue models for crypto entrepreneurs and investors

As more banks enter the space, the future of crypto will look less like “Wild West speculation” and more like a fully integrated digital financial system governed by global standards.

SoFi is simply the first mover.

The rest of the banking sector is now on the clock.