Main Points :

- The Basel Committee is signaling a need to revisit its strict crypto risk-weighting rules as stablecoins become increasingly central in global financial markets.

- Current Basel rules assign Bitcoin and similarly volatile assets a 1,250% risk weight, effectively requiring banks to hold $1 in capital for every $1 of crypto exposure.

- Major regulators including the U.S. Federal Reserve and Bank of England now say the Basel crypto framework is “unrealistic” and may not be implemented in its current form.

- The U.S. recently passed the Genius Act, creating a clear regulatory structure for stablecoins and accelerating institutional adoption.

- Mega-banks including MUFG, Citi, Goldman Sachs, and Bank of America are already exploring G7-currency-linked stablecoins.

- Japan also approved a pilot project for three mega-banks to jointly issue regulated stablecoins.

- The global conversation is now shifting: Is permissionless blockchain really as risky as once assumed?

I. Introduction — A New Phase in Global Crypto Regulation

On November 19, 2025, the Financial Times reported a significant shift in tone from Eric Thedéen, Chair of the Basel Committee on Banking Supervision (BCBS). For years, Basel’s treatment of crypto assets has been defined by exceptionally conservative assumptions. Bitcoin, Ethereum, and any token with substantial price volatility have been assigned a 1,250% risk weight, the highest category possible.

This essentially prohibits meaningful crypto exposure by banks.

But the world has changed since the rules were drafted three years ago. At that time, Bitcoin dominated public conversation; today, institutional finance is far more interested in regulated, fiat-backed stablecoins, tokenized deposits, and permissionless blockchain infrastructure that can support programmable finance.

Accordingly, Thedéen now says the Basel framework must be re-evaluated urgently.

“Are permissionless ledgers truly as risky as we thought? Or is there another way to look at them?”

— Eric Thedéen, Basel Committee Chair

This marks one of the strongest signals to date that the global regulatory architecture around crypto is entering a revisionary stage.

II. Basel’s Current Crypto Rules — Why They Are So Restrictive

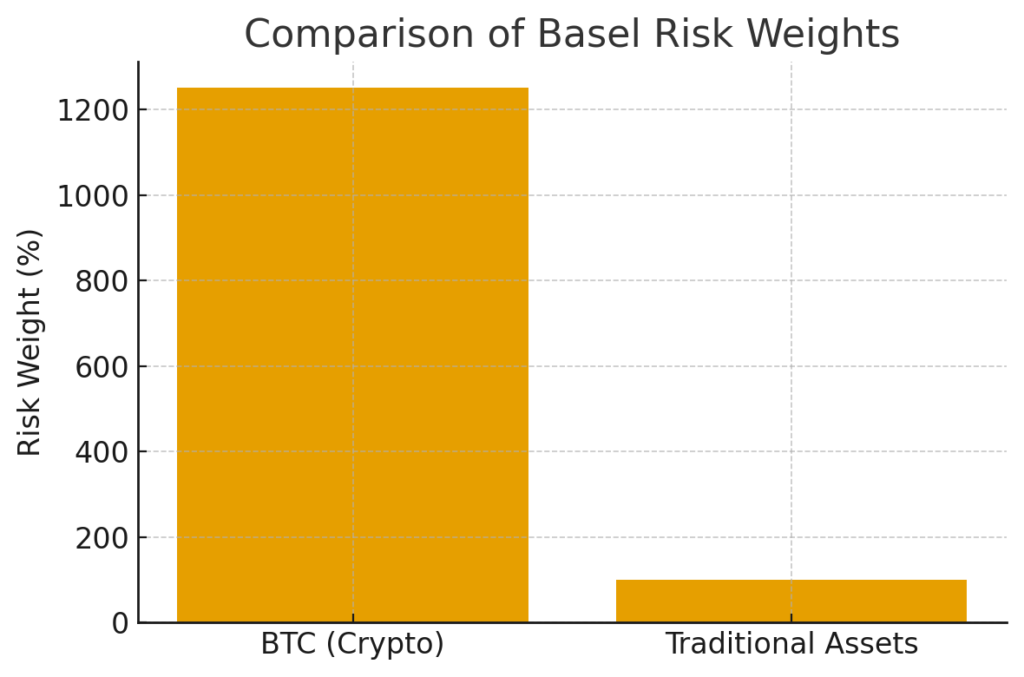

1. The 1,250% Risk Weight Explained

Under Basel’s existing rule (scheduled to take effect January 1), any bank holding volatile crypto assets must apply a 1,250% risk weight.

This means:

- A bank holding $100 in Bitcoin exposure

→ must reserve $100+ in capital

→ making the economic incentive essentially zero.

Traditional corporate bonds, by comparison, often carry a 100% risk weight.

This extreme treatment reflects concerns in 2020–2022:

• exchange collapses,

• insufficient auditing of stablecoin reserves,

• high volatility,

• limited transparency in crypto markets.

But the market has evolved dramatically:

- On-chain reserve attestation

- Regulated stablecoin issuers

- Real-time blockchain auditability

- Institutional custody infrastructure

- Bank-issued stablecoin projects

Thedéen argues that a rule built for the 2021 environment may no longer fit the realities of 2025.

III. The Global Regulatory Shift — U.S. and U.K. Reject Basel’s Approach

1. U.S. Federal Reserve: Basel’s Approach Is “Unrealistic”

Michelle Bowman, Vice Chair for Supervision at the Federal Reserve, announced in October that the U.S. would not adopt Basel’s crypto risk-weight standards as written.

The reason:

Basel overestimates risk and underestimates the rise of high-quality, fully reserved stablecoins and tokenized bank liabilities.

2. U.K. (Bank of England): Same Direction

Insider reports confirm that the Bank of England will also decline implementation of the Basel crypto framework.

This is crucial because the U.K. is aggressively positioning itself as a global fintech and digital-asset hub.

This means the world’s two most influential banking jurisdictions are rejecting Basel’s model.

Basel’s rules only have power when countries implement them domestically.

If major economies do not follow them, pressure builds for revision.

IV. The Stablecoin Revolution — Why Regulators Are Rewriting the Rules

1. The Genius Act: The First Clear U.S. Stablecoin Law

The newly passed U.S. Genius Act provides:

- licensing rules

- reserve requirements

- redemption standards

- cybersecurity obligations

- consumer protection rules

This law effectively clears the path for banks and payment institutions to issue stablecoins backed 1:1 with U.S. dollars.

Because the world’s largest capital markets now have a functional legal framework for stablecoins, institutional adoption is accelerating.

2. G7-Linked Bank Stablecoins Under Study

In October, 10 global mega-banks began a joint study into issuing stablecoins pegged to G7 currencies such as:

- U.S. dollar

- British pound

- Japanese yen

- Euro

Participants include:

- Bank of America

- Goldman Sachs

- Citi

- MUFG

- And others

Although details remain confidential, the banks are already coordinating with regulators.

This represents the first cross-border stablecoin collaboration by major banks in history.

3. Japan: Government-Approved Mega-Bank Stablecoin Tests

On November 7, Japan’s Financial Services Agency approved a proof-of-concept project involving:

- Mizuho Bank

- MUFG

- SMBC

Their goal: issue compliant Japanese-yen stablecoins for domestic and cross-border payment use.

Japan appears to be preparing for a world in which regulated banks and fintech players jointly operate a stablecoin infrastructure.

V. Why Permissionless Ledgers Are Back in the Conversation

Eric Thedéen’s comment about permissionless ledgers is significant.

For years, regulators assumed permissionless systems (Bitcoin, Ethereum, etc.) were inherently too risky to integrate with the banking system.

But three developments are changing the discussion:

1. On-Chain Audits Improve Transparency

Stablecoins now publish real-time or daily reserve data on-chain.

2. Banks Want Interoperability

Bank-issued stablecoins need to interact with the broader crypto ecosystem; siloed systems limit adoption.

3. Capital Markets Are Tokenizing Assets

U.S. Treasuries, money-market funds, and repo markets are beginning to issue tokenized versions on public chains.

If the capital markets are moving on-chain, permissionless blockchains become part of the financial infrastructure.

Thus, the original assumption—“public chains = too risky”—is being challenged at the highest regulatory levels.

VI. Implications for Crypto Investors and Builders

The audience of your publication—those interested in new crypto assets, revenue opportunities, and practical blockchain applications—should pay close attention.

1. Bank-Issued Stablecoins Will Create New On-Chain Liquidity

If G7-linked stablecoins become widely issued, they will form the deepest and safest liquidity pools in crypto.

These assets will enable:

- low-cost cross-border remittances

- institutional DeFi

- FX trading on-chain

- high-grade collateral for lending protocols

- corporate treasury tokenization

2. Risk-Weight Revisions Could Open the Door for Bank Crypto Custody

If regulators soften the 1,250% rule, banks will:

- hold crypto directly

- provide custody services

- expand institutional OTC trading

- integrate stablecoins in settlement systems

The institutional wall could break rapidly.

3. Developers Should Expect Strong Demand for Reg-Tech and Compliance-Tech

As stablecoins become regulated like commercial bank money, new opportunities emerge:

- blockchain-based AML frameworks

- travel rule automation

- on-chain KYC systems

- programmable compliance tokens

Crypto developers who understand both tech and regulation will be uniquely valuable.

VII. Conclusion — A Turning Point for Crypto Regulation

The Basel Committee’s admission that its crypto rules may be outdated marks a pivotal moment.

What began as a rigid framework built around the volatility of Bitcoin has collided with a stablecoin-driven reality. As the U.S., U.K., Japan, and global mega-banks move forward with regulated stablecoin infrastructure, the world’s banking regulators can no longer treat crypto as a fringe asset.

The next phase of global finance will merge banking and blockchain, not separate them.

If Basel softens its stance, the transformation could accelerate dramatically—unlocking institutional adoption, global liquidity, tokenized finance, and new revenue opportunities for builders and investors alike.