Main Points:

- Asian banks are piloting government-pegged stablecoins to stem deposit erosion and boost cross-border trade.

- In Korea, a consortium of eight major banks aims to issue a won-backed stablecoin by 2026.

- Japanese banking giants MUFG, SMBC, and Mizuho are exploring a yen-pegged coin for trade finance and payments.

- Hong Kong’s Bank of East Asia has launched trials of dollar and HKD stablecoin networks.

- Payment service providers are shifting from traditional rails to stablecoins for cost savings and customer demands.

- E-commerce platforms like JD.com and PSPs such as Tazapay are using stablecoins to streamline supplier payouts and gig-economy remittances.

- U.S. regulatory developments, notably the Senate’s GENIUS Act, are fueling global stablecoin momentum.

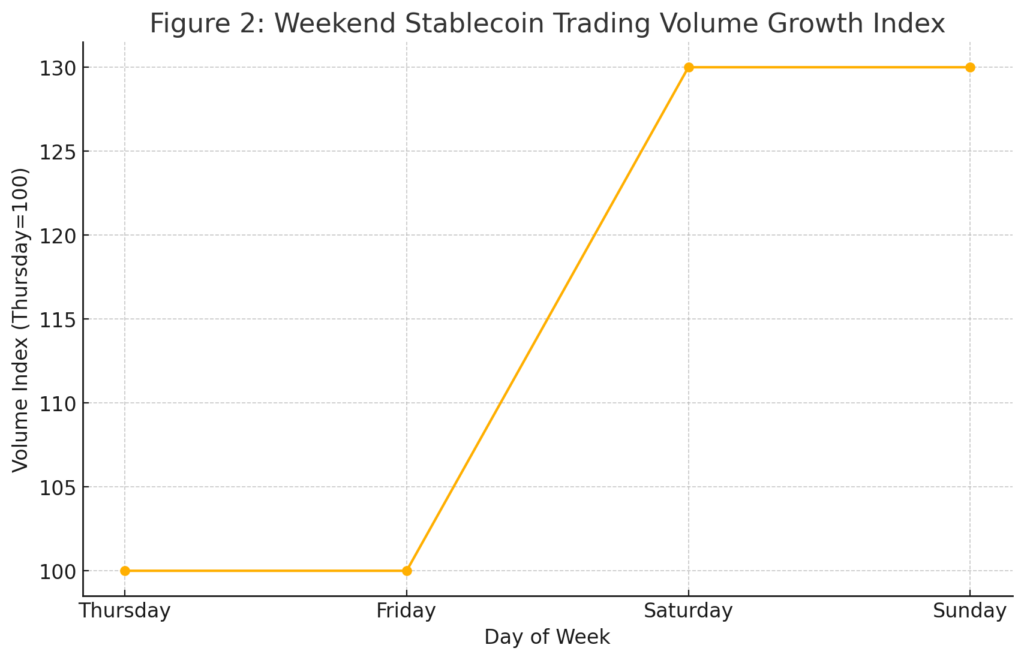

- Stablecoins already account for nearly half of Fireblocks’ $3 trillion in digital asset volume, and weekend trading volumes jumped ~30% per Visa Analytics.

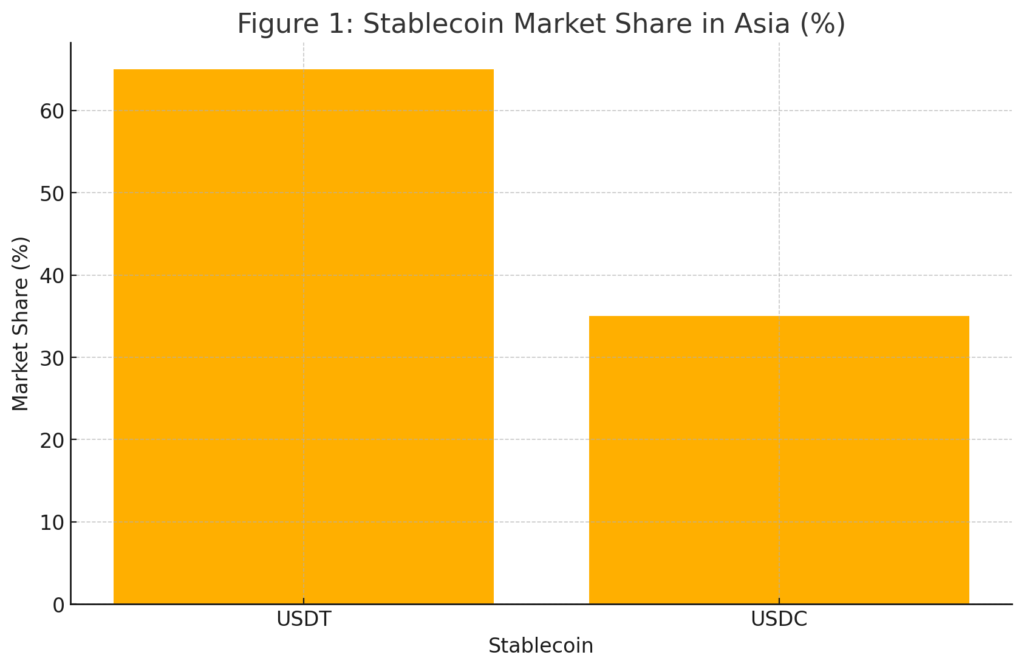

- USDT dominates Asian emerging markets, while USDC gains traction in regulated hubs like Singapore and Hong Kong.

- As banks move defensively, stablecoins could reshape Asia’s cross-border financial infrastructure.

Introduction

Asia’s leading financial institutions face mounting pressure from deposit outflows and declining transaction revenue. To fortify their balance sheets and modernize cross-border settlement, banks across Korea, Japan, and Hong Kong are eyeing stablecoins pegged to local currencies. Though much of this activity remains under the radar, pilots and consortiums are laying the groundwork for a transformation of trade finance and corporate payments. This article delves into these strategic moves, examines broader market drivers—including U.S. regulatory shifts—and considers the implications for banks, payment providers, and corporate users.

1. Defending Against Deposit Outflows

Banks in Asia worry that corporate clients, in search of yield and cross-border convenience, may park funds in crypto rails—particularly in stablecoins like USDT and USDC—rather than leave deposits on-balance-sheet. Amy Zhang, Fireblocks’ Head of Asia, warns: “If you’re not trading with Circle or Tether, you risk losing deposits”. By issuing their own central bank–peppered stablecoins, banks aim to retain client funds while offering instant, low-cost global transfers.

2. Korea’s Won-Backed Stablecoin Consortium

In April 2025, eight of South Korea’s largest lenders—including KB Kookmin Bank and Shinhan Bank—formed a consortium targeting issuance of a KRW-backed stablecoin by 2026. This initiative directly addresses the rapid growth of USDT and USDC in Korean cross-border trade corridors. By anchoring the coin to the won and integrating it into domestic payment systems, Korean banks hope to mitigate capital flight and enhance remittance efficiency.

3. Japan’s Push into Yen-Pegged Coins

Three banking behemoths—Mitsubishi UFJ Financial Group (MUFG), Sumitomo Mitsui Banking Corporation (SMBC), and Mizuho Bank—are jointly exploring a yen-denominated stablecoin for trade finance and corporate payments. These pilots aim to streamline syndication processes, automate documentary credits, and reduce foreign exchange risk in Asia-Pacific supply chains.

4. Hong Kong’s Dual-Currency Trials

Hong Kong’s Bank of East Asia recently began testing both USD- and HKD-pegged stablecoin networks for institutional clients. These trials focus on real-time settlement, lower transaction fees, and interoperability with existing token-based payment channels. The bank’s move signals growing acceptance of stablecoins as complementary to traditional RTGS systems.

5. PSPs Accelerating Stablecoin Adoption

Payment service providers (PSPs) in Asia have rapidly shifted from “Should we consider stablecoins?” to “Our users need enterprise-grade wallets” within a year, according to Fireblocks. PSPs like Tazapay leverage USDC to facilitate instant USD and HKD payouts across emerging Asian markets—serving content creators, gig-economy workers, and SMEs. These platforms bypass costly correspondent banking, offering sub-1% fees and near-instant settlement.

6. E-Commerce Use Cases

China’s JD.com has publicly acknowledged pilot programs that use stablecoins to pay suppliers, reducing liquidity costs by up to 20%. By tokenizing payables on a permissioned network, JD.com shortens settlement cycles and consolidates working capital. This model is catching on among regional e-tailers looking to optimize cash flow and minimize FX slippage.

7. U.S. Regulatory Catalysts

On June 18, 2025, the U.S. Senate passed the GENIUS Act, establishing the first comprehensive federal framework for stablecoins. This bipartisan legislation classifies stablecoins as payment systems, mandates transparent reserves, and imposes consumer safeguards. Circle’s USDC issuer, Circle Internet Group (CRCL), saw share prices rise over 30% on the news. Although the bill must still clear the House, its passage signals growing legitimacy for stablecoins worldwide, encouraging Asian banks to move from pilots to production.

8. Market Data and Analytics

Fireblocks reported managing over $3 trillion in digital assets last year (approximately ¥432 trillion at $1=¥144), with stablecoin transactions comprising roughly half of that volume. Weekend stablecoin trades spiked 30% per Visa Analytics, underscoring strong retail and gig-economy demand for programmable money.

Figure 1: Stablecoin Market Share in Asia (USDT vs USDC)

Figure 2: Weekend Stablecoin Trading Volume Growth Index

9. Token Leadership: USDT vs. USDC

In emerging Asian markets, Tether’s USDT commands around 65% of stablecoin turnover, prized for deep liquidity and wide exchange listings. Conversely, Circle’s USDC—backed by short-term U.S. Treasury bills—is gaining traction in regulated hubs like Singapore and Hong Kong, thanks to its transparent reserve disclosures and compliance credentials.

10. Future Outlook: From Defense to Offense

Initially defensive, Asian banks view stablecoins as a hedge against deposit flight. Yet as pilots mature, these tokens could become core infrastructure, enabling programmable finance, automated trade instruments, and real-time corporate treasury management. Integration with CBDC initiatives and tokenized asset platforms may further accelerate stablecoin adoption, driving a paradigm shift in Asia’s financial architecture.

Conclusion

Asia’s banking sector stands at a crossroads: cling to legacy rails or embrace tokenized liquidity. With deposit outflows mounting and cross-border demands rising, stablecoins pegged to local currencies offer a compelling solution. From Korea’s consortium and Japan’s banking giants to Hong Kong’s pilot networks and PSP-driven use cases, the groundwork is laid for a stablecoin-powered financial ecosystem. Regulatory signals from the U.S. and market data on transaction surges amplify the momentum, suggesting that stablecoins may soon transition from tactical defenses to strategic enablers of Asia’s next-generation banking services.