Main Points :

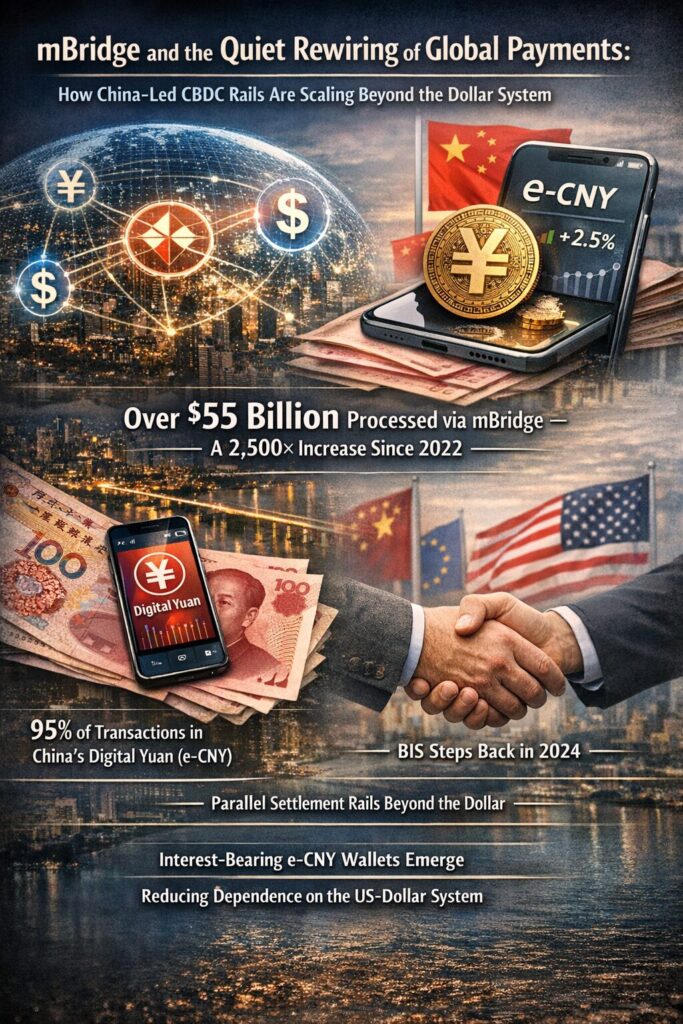

- mBridge, a China-led multi-CBDC platform, has processed more than $55 billion in cross-border transactions, a roughly 2,500× increase since its 2022 pilot phase.

- Around 95% of settlement value is estimated to involve China’s digital yuan (e-CNY), underscoring China’s central role in the network.

- China is expanding e-CNY functionality by allowing interest payments on wallet balances, signaling a shift from “digital cash” toward a deposit-like monetary instrument.

- Rather than directly replacing the US-dollar system, mBridge represents the construction of parallel settlement rails that reduce dependency on dollar-centric infrastructure.

- Geopolitical sensitivities led the Bank for International Settlements (BIS) to step back from mBridge in 2024, while Western central banks refocused on alternative initiatives.

Introduction: From Pilot Experiment to Systemic Signal

In discussions about the future of money, central bank digital currencies (CBDCs) often appear as long-term experiments—important in theory but slow to materialize in practice. The rapid expansion of mBridge, however, challenges this assumption. What began as a limited proof-of-concept for cross-border CBDC settlement has quietly evolved into a platform that has already processed more than $55 billion in international payments.

This growth matters not only because of the scale involved, but because of where and how these transactions are occurring. mBridge operates largely outside traditional dollar-centric correspondent banking systems, offering an alternative model for international settlement that is faster, more direct, and potentially less exposed to geopolitical constraints. For readers interested in emerging digital assets, new revenue models, and practical blockchain use cases, mBridge provides a real-world example of how state-backed digital money is moving from theory into production.

What Is mBridge? A Multi-CBDC Settlement Network

mBridge is a cross-border digital currency platform designed to connect multiple CBDCs on a single interoperable ledger. Instead of routing international payments through layers of correspondent banks, the system allows participating central banks and commercial banks to settle transactions directly using their respective digital currencies.

The platform currently involves the central banks of China, Hong Kong, Thailand, the United Arab Emirates, and Saudi Arabia. According to data compiled by the Washington-based Atlantic Council, mBridge has facilitated more than 4,000 cross-border transactions, with cumulative settlement volume reaching approximately $55.5 billion.

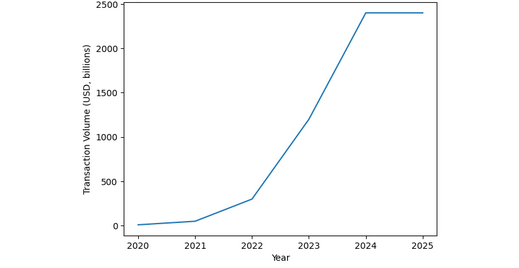

The most striking feature is the pace of adoption. Compared with the early pilot stage in 2022, transaction volume has increased by roughly 2,500 times, suggesting that mBridge is no longer a laboratory experiment but an operational settlement rail used for real economic activity.

The Dominance of the Digital Yuan (e-CNY)

While mBridge is a multilateral platform, its activity is heavily concentrated around China’s digital yuan (e-CNY). Analysts estimate that roughly 95% of total settlement value on mBridge involves e-CNY, reflecting China’s advanced domestic CBDC infrastructure and its proactive push to internationalize the currency through digital channels.

Domestically, the scale of e-CNY adoption is already enormous. According to the People’s Bank of China, cumulative e-CNY transactions exceed $2.4 trillion, representing more than 3.4 billion individual transactions. This marks an increase of over 800% compared with 2023 levels.

[“Growth of e-CNY Transaction Volume (USD)” — a line chart showing exponential growth from pilot phase to current scale.]

This domestic foundation gives China a unique advantage. By first normalizing digital currency usage at home, the country can then extend those capabilities outward, embedding e-CNY into cross-border trade, energy settlement, and regional financial flows.

Paying Interest on e-CNY: A Structural Shift

One of the most consequential recent developments is China’s decision to allow commercial banks to pay interest on e-CNY wallet balances. Originally designed to function like digital cash—non-interest-bearing and primarily for payments—the digital yuan is now being repositioned as a “digital deposit currency.”

This change has major implications:

- Balance Sheet Integration

Banks can now incorporate e-CNY into their asset-liability management frameworks, treating it more like a deposit than a payment token. - User Incentives

Interest-bearing balances increase the attractiveness of holding e-CNY, encouraging users and corporates to keep funds in digital form rather than converting back to traditional deposits. - Cross-Border Utility

An interest-bearing digital currency is more suitable for trade settlement, treasury management, and international liquidity operations.

As a deputy governor of the People’s Bank of China explained, e-CNY is evolving beyond daily payments to include store-of-value and cross-border settlement functions. This evolution blurs the line between traditional bank money and programmable digital cash, creating new opportunities for financial innovation—and new challenges for regulators.

Parallel Rails, Not a Dollar Overthrow

A common narrative frames mBridge as a direct challenge to US-dollar dominance. In reality, the strategy appears more nuanced. Rather than attempting to displace the dollar outright, China and its partners are building parallel settlement infrastructure that reduces reliance on dollar-based systems such as SWIFT and correspondent banking networks.

As analysts at the Atlantic Council have noted, this approach lowers exposure to geopolitical risk and operational bottlenecks without forcing countries to abandon the dollar entirely. In practice, this means:

- Faster settlement with fewer intermediaries

- Lower transaction costs for cross-border trade

- Reduced vulnerability to sanctions or payment disruptions

For emerging markets and energy-exporting nations, these features are particularly attractive. They offer optionality—a way to diversify settlement channels while maintaining access to existing systems.

BIS Steps Back: Geopolitics Enters the Room

The geopolitical sensitivity of mBridge became explicit in 2024, when the Bank for International Settlements stepped back from the project. The BIS had been involved through its Innovation Hub since 2021 but announced what it described as a “graduation,” not a withdrawal.

Behind the diplomatic language were concerns that mBridge could be used to circumvent international sanctions, particularly if adopted by BRICS countries or other sanctioned states. BIS General Manager Agustín Carstens publicly emphasized that mBridge was “not a bridge for BRICS” and that BIS-operated systems could not be used by sanctioned entities.

Following this shift, the BIS redirected its focus toward another initiative, often referred to as Project Agora, which involves a broader group of Western central banks and emphasizes compliance with existing international norms.

Practical Implications for Blockchain and Digital Asset Professionals

For practitioners and investors focused on blockchain’s real-world applications, mBridge offers several important lessons:

- CBDCs Are Becoming Operational Infrastructure

This is no longer about white papers or pilots. Billions of dollars are moving through digital rails today. - Interoperability Is the Key Value Layer

mBridge’s core innovation is not any single CBDC, but the interoperable settlement layer connecting them. - Revenue Opportunities Will Be Indirect

Unlike public crypto networks, CBDC platforms do not generate yield through mining or staking. Instead, opportunities arise in integration services, compliance tooling, liquidity management, and cross-border treasury optimization. - Private and Public Systems Will Coexist

CBDCs will not eliminate stablecoins or permissionless blockchains. Instead, we are likely to see a layered system where different rails serve different risk, speed, and regulatory requirements.

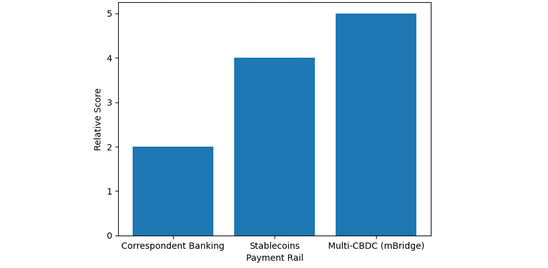

[“Global Payment Rails Comparison” — a diagram comparing traditional correspondent banking, stablecoins, and multi-CBDC platforms like mBridge.]

Strategic Outlook: A Multipolar Monetary Future

mBridge signals a broader shift toward a multipolar global monetary system, where no single currency or infrastructure monopolizes cross-border settlement. In such a system:

- The dollar remains dominant but less exclusive

- Regional currencies gain functional international roles

- Digital infrastructure becomes a strategic asset

For China, mBridge complements long-standing goals of renminbi internationalization, now accelerated through digital means. For participating countries, it provides practical benefits without requiring ideological alignment.

Conclusion: Why mBridge Matters Now

The rise of mBridge is not about headlines or ideological confrontation. It is about plumbing—the underlying infrastructure that determines how money moves across borders. By quietly scaling to more than $55 billion in settlements, mBridge demonstrates that CBDCs can function as real, high-value payment rails today.

For readers seeking the next wave of digital asset opportunities and practical blockchain use cases, the key takeaway is this: the future of finance will be shaped as much by state-backed digital infrastructure as by open crypto networks. Understanding how these systems interact—and where value can be created at their intersections—will be essential in the years ahead.