Main Points:

- Mastercard and Thunes now enable real-time stablecoin transfers in over 200 markets globally.

- Stablecoin wallets are officially added as payout destinations in Mastercard Move.

- This marks a major step toward merging traditional finance (cards, banks, cash) with digital assets.

- Stablecoins reduce FX volatility, settlement delays, and infrastructure gaps in emerging markets.

- The partnership signals mass adoption of stablecoins as a cross-border payment standard.

1. Introduction — A New Phase in Global Payments

The world of cross-border payments is undergoing its most dramatic transformation in decades. On November 13, 2025, Mastercard announced a strategic expansion with Thunes, enabling stablecoin-based real-time transfers in more than 200 global markets. This upgrade integrates stablecoin wallets directly into the company’s payment ecosystem, placing digital assets alongside traditional payout channels like cards, bank accounts, and cash.

For investors and builders seeking opportunities in new cryptocurrencies, blockchain utilities, and decentralized payment infrastructure, this development signals a structural shift: stablecoins are no longer experimental—they are entering the global payment mainstream.

2. Thunes Partnership Brings Stablecoin Transfers to 200 Markets

Mastercard’s partnership with Thunes marks the inclusion of stablecoin wallets as official payout endpoints on Mastercard Move, the company’s flagship global transfer network. Mastercard Move already supports:

- 150+ fiat currencies

- 200+ countries/markets

- Over 1 billion potential payout destinations

The newest addition—stablecoin payout rails—expands the breadth of options available to banks, enterprises, and fintech developers. It means users worldwide could receive funds not only into bank accounts or cards but also into digital stablecoin wallets such as USDC-compatible or region-specific tokens.

This rollout is significant because Thunes specializes in delivering payments to hard-to-reach markets where traditional banking infrastructure is limited. With stablecoins, Mastercard can bypass inefficient rails and improve accessibility.

3. Mastercard’s Strategy to Strengthen Stablecoin Infrastructure

3.1 Eliminating Regional Payment Gaps

Stablecoins solve a long-standing problem in global finance: inconsistent infrastructure and FX instability across regions.

Mastercard’s integration highlights key advantages:

- 24/7 real-time settlement, even across borders

- No dependency on domestic banking hours or intermediaries

- Reduced currency volatility exposure for emerging markets

- Greater financial inclusion for users without reliable bank access

This aligns with Mastercard’s broader mission of creating an interoperable, always-on payment network bridging fiat and digital asset ecosystems.

3.2 Market Structure Changes Driven by Stablecoins

Stablecoin-enabled transfers reshape traditional remittance and payment models by:

- Removing the need for multiple correspondent banks

- Reducing settlement time from days to seconds

- Lowering FX management and hedging costs

- Enabling programmable, automated payments via blockchain

For markets with weak infrastructure, stablecoins act as a neutral settlement asset independent of local financial bottlenecks.

Mastercard positions itself as a trusted bridge between traditional rails and digital currency networks, ensuring compliance, AML monitoring, and licensing remain intact.

4. Ripple’s RLUSD Testing and BTC Payment Expansion

This announcement follows other recent Mastercard initiatives:

4.1 RLUSD Card Payment Testing

Mastercard is testing card payments powered by Ripple’s RLUSD stablecoin, indicating the company’s willingness to incorporate multiple digital asset ecosystems—not just USDC or USDT.

4.2 Bitcoin Payments at 150+ Million Merchants

Earlier, Mastercard partnered with Kraken to enable BTC payments at more than 150 million merchants worldwide. While settlements are typically off-chain, this further demonstrates Mastercard’s push into crypto-powered commerce.

These moves signal that Mastercard is positioning digital assets not as competitors but as complementary instruments within global payments.

5. Indicators of Mass Stablecoin Adoption

The Mastercard-Thunes partnership exemplifies a broader trend:

- Major enterprises are adopting stablecoins as settlement layers

- Banks and fintechs are adding digital assets to payout options

- Regulated payment networks are integrating directly with blockchains

Stablecoins such as USDC and RLUSD are becoming functionally equivalent to fiat in cross-border scenarios. The number of markets where users can receive payments in stablecoins will expand rapidly through 2026–2030.

6. Recent Trends from External Sources (2024–2025)

To provide context for investors and industry participants, here are additional developments:

6.1 Circle’s Expansion into Asia and the Middle East

Circle has partnered with regional banks in Japan, Singapore, UAE, and Hong Kong to expand USDC on- and off-ramps.

6.2 Global FX Stress Pushing Corporates Toward Stablecoins

A 2025 BIS report indicates over $350B/month in B2B payments now leverage stablecoins for interim settlement, largely due to FX hedging costs and unpredictable clearing times.

6.3 UN and World Bank Research on Remittances

Stablecoin rails can cut remittance fees from 6% to less than 1%, a major benefit for markets like the Philippines, India, Nigeria, and LATAM.

6.4 Bank Adoption Growing Faster Than Crypto Exchanges

Banks are beginning to use stablecoins internally for treasury and inter-branch settlements—possibly the biggest catalyst for adoption after 2026.

These developments reinforce Mastercard’s timing and strategic direction.

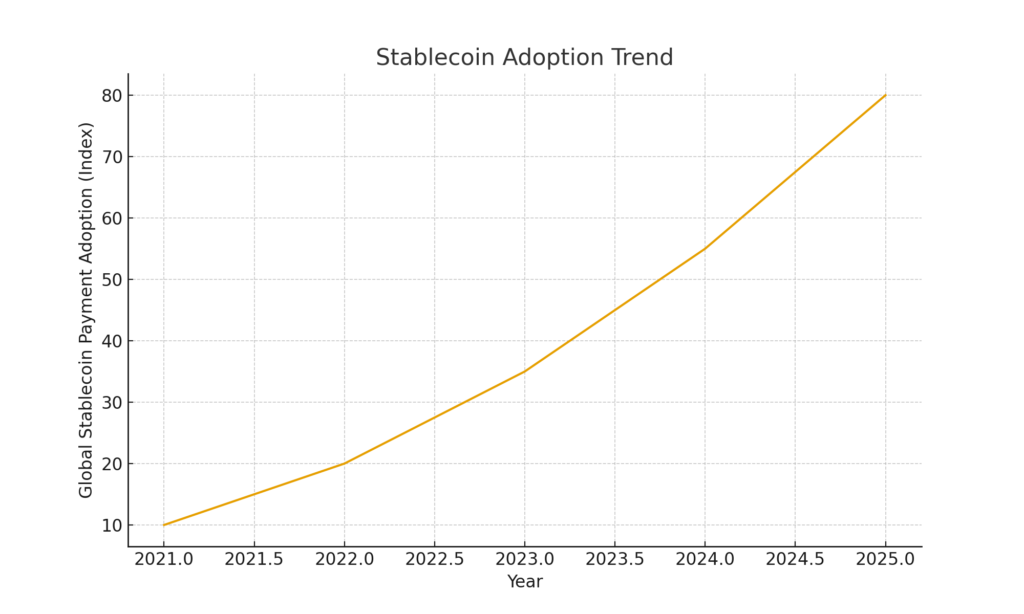

7. Chart: Global Stablecoin Adoption Trend (2021–2025)

8. Conclusion — Stablecoins Enter the Global Financial Mainstream

Mastercard’s integration of stablecoin transfers into 200 markets through Thunes is not a small update—it is a landmark shift in the global payments landscape. It demonstrates that:

- Traditional payment giants now see stablecoins as core infrastructure

- The barriers between fiat and digital currency ecosystems are dissolving

- Real-time, low-cost cross-border payments are becoming the new standard

- Investments in stablecoin-related assets and blockchains will likely grow sharply

- Emerging markets may leapfrog legacy rails directly into digital settlement

For readers seeking new crypto opportunities, this trend highlights where the future is headed: stablecoin utility, payment integration, and infrastructure linking traditional finance tmある2o blockchain.

Bank-backed and enterprise-grade adoption is accelerating, and Mastercard’s move signals the beginning of mainstream stablecoin payment networks on a global scale.