Key Takeaways :

- Japan plans to require crypto exchanges to hold a dedicated “responsibility reserve” to compensate customers rapidly after hacks or asset leaks.

- The reserve will likely cover assets even in cold wallets, closing a gap where large offline balances were historically treated as “safe but uncompensated” if compromised.

- The move follows major incidents at DMM Bitcoin (≈$308 million) and Bybit (≈$1.5 billion), both linked to sophisticated state-backed attackers.

- Exchanges may respond with higher fees, stricter listings, more proof-of-reserves, and new insurance-like products, creating both constraints and fresh opportunities for projects.

- For traders and builders, Japan is becoming a laboratory for “regulation-first” Web3, where compliant, insured venues and infrastructure providers could be rewarded with institutional capital and sticky retail users.

1. What the New “Responsibility Reserve” Is About

Japan’s Financial Services Agency (FSA) is reportedly moving to mandate a dedicated “responsibility reserve” for crypto-asset exchange service providers. The idea is straightforward: if customer assets are stolen through hacking or other unauthorized access, there should already be a pot of money and/or valid insurance that allows for rapid, full compensation without waiting for years of bankruptcy proceedings.

Japan already has one of the world’s strictest frameworks for crypto:

- Crypto is regulated under the Payment Services Act (PSA).

- Exchanges must register with the FSA and meet requirements on asset segregation, AML/CFT, and disclosure.

- Existing guidelines expect at least 95% of customer crypto to be held in offline cold wallets, with strict segregation of customer and corporate funds.

However, even this model has a blind spot:

What happens when cold wallets themselves are compromised?

The new reserve regime aims to fix exactly this. According to discussion papers and commentary, the FSA is considering:

- A mandatory reserve fund sized with reference to:

- Past hacks (like DMM and Bybit)

- Large domestic securities firms’ customer protection schemes

- Allowing insurance policies to count toward the required reserve, so exchanges can mix capital buffers and external coverage.

- Imposing clear rules for returning assets when an exchange fails, including mechanisms for court-appointed or lawyer-appointed administrators to distribute assets even if management disappears.

In practice, this pushes crypto exchanges closer to traditional financial institutions, where customer compensation schemes (like deposit insurance or investor protection funds) are standard.

2. Why Japan Is Moving Now: The DMM Bitcoin and Bybit Shock

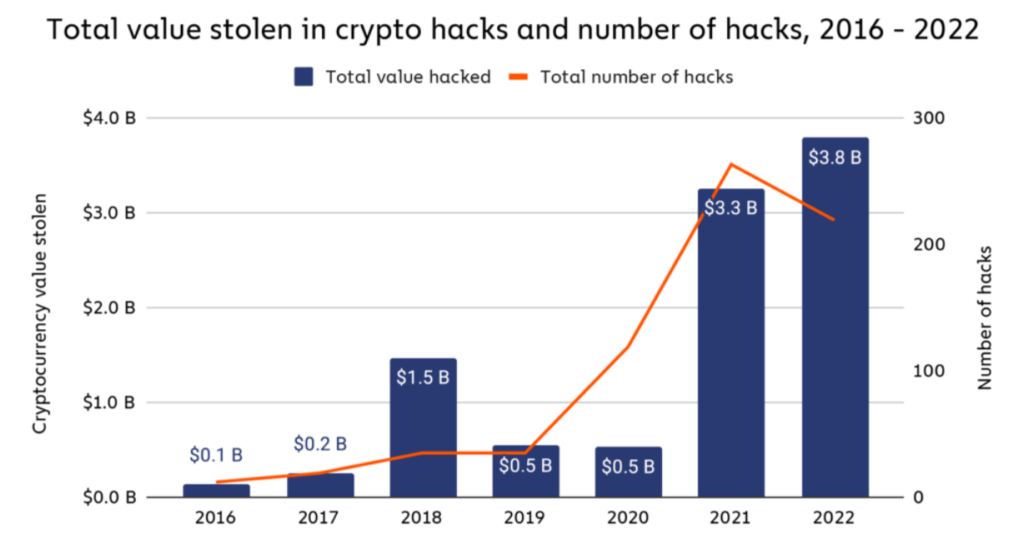

The FSA’s move is not happening in a vacuum. It follows a series of large-scale incidents that revealed how costly—and reputationally damaging—major hacks can be.

2.1 DMM Bitcoin: A $308 Million Wake-Up Call

In May 2024, Japanese exchange DMM Bitcoin suffered a hack worth about $308 million in crypto assets, involving roughly 4,502 BTC at the time.

Investigations by law enforcement and blockchain analytics firms later linked the attack to North Korean-backed actors, who used sophisticated laundering techniques, routing funds through intermediate addresses and mixing services.

Key lessons from DMM:

- Cold wallets are not magically invulnerable. Attackers targeted infrastructure and operational processes, not just online wallets.

- The loss magnitude—hundreds of millions of dollars—highlighted how single-event risk can threaten an exchange’s solvency.

- Regulators realized that even with strict cold-wallet requirements, customers could still face long delays or haircuts if a large theft pushed an exchange into distress.

2.2 Bybit: The “Biggest Digital Heist Ever”

Then, in February 2025, Bybit, one of the world’s largest exchanges, was hacked for around $1.4–1.5 billion worth of ETH and other assets, again apparently linked to North Korean “TraderTraitor” actors.

Although Bybit is not a Japanese exchange, its incident had a direct impact on global regulators:

- It set a new record for the largest ever exchange hack by dollar value.

- It demonstrated that even massive cold-wallets can be drained through clever manipulation of transaction approval workflows.

- It showed how quickly attackers can disperse and launder funds across chains.

For Japan’s policymakers, both the DMM and Bybit hacks reinforced one message:

Large, professional adversaries are here to stay—and they target exactly the kind of cold-wallet-heavy, high-value exchanges that Japanese rules have encouraged.

Hence, the logic behind the responsibility reserve: if you know major incidents are statistically inevitable, you must pre-fund the damage.

3. How the Responsibility Reserve Fits into Japan’s Broader Crypto Rules

Japan has taken a regulation-first approach to crypto since at least 2016, when it introduced a legal framework for exchanges earlier than almost any other major jurisdiction.

Already in place:

- Registration requirement for crypto-asset exchange service providers

- Stringent AML/CFT obligations, including Travel Rule implementation with no minimum threshold—info must be shared regardless of transaction size

- Segregated custody, with offline cold storage for the vast majority of customer assets

- Ongoing discussions about reclassifying crypto assets as financial assets and potentially making their tax treatment more investor-friendly.

The responsibility reserve proposal sits on top of this stack as an additional layer:

- Operational Security: Minimize attack surface through cold wallets, multi-sig, secure hardware, and system provider oversight.

- Regulatory Oversight: Registration, Travel Rule, AML/KYC, asset segregation.

- Financial Backstop: Responsibility reserve (plus insurance) to make customers whole even if layer 1 and 2 fail.

For exchanges serving Japanese residents, this means their capital structure and risk management must look more like a bank or securities broker than a pure tech startup.

4. Practical Impacts for Exchanges, Tokens, and Yield Products

From the perspective of investors, builders, and liquidity providers, the new reserve rule is both a constraint and a new opportunity surface.

4.1 Higher Costs and Tighter Margins for Exchanges

Exchanges operating in Japan—or any venue that wants Japanese listings—may face:

- Higher capital and liquidity requirements to fund the reserve.

- The need to buy insurance in USD terms large enough to cover extreme-loss scenarios, which is not cheap.

- More conservative risk management: fewer highly leveraged products, tighter controls on collateral types, and stricter counterparty limits.

This can compress short-term profit margins. But it also raises the barrier to entry, potentially benefiting larger, better-capitalized platforms at the expense of thin-capitalized competitors.

4.2 Listing Standards and Project Readiness

If exchanges are on the hook for rapid compensation, their incentives change:

- They may prefer tokens with deeper liquidity, less technical attack surface, and robust on-chain governance.

- Smart-contract risk becomes more than a disclosure issue; it becomes a capital drain risk on the reserve.

- New altcoins seeking listing may be asked to demonstrate security audits, bug bounty programs, and robust treasury/DAO governance as a condition for being onboarded.

For builders, that means:

- Projects with serious security posture (audits, formal verification, multi-sig governance) gain a competitive edge.

- “High-APY but opaque” DeFi tokens may see harder listing conditions, especially on regulated Japanese venues.

4.3 Emergence of Insurance-Like Products and New Revenue Streams

Because the responsibility reserve can be satisfied partly through insurance contracts, there is a natural opening for:

- Crypto-specific insurance and reinsurance products denominated in USD or stablecoins.

- Hybrid structures where exchanges allocate a portion of their yield from staking, liquidity provision, or basis trading into a dedicated safety fund.

- On-chain insurance protocols that can provide parametric coverage to centralized exchanges, bridges, and custodians.

For DeFi builders and institutional investors, this is an opportunity:

- Design risk-tokenized structures where investors earn yield by underwriting part of an exchange’s reserve requirement.

- Create reg-compliant, capital-efficient insurance vaults that satisfy FSA expectations but still operate on chain.

None of this is simple—but players who solve it in a compliant way could unlock new fee streams while becoming critical infrastructure for Japan-facing crypto business.

5. What This Means for Traders and Long-Term Crypto Users

From a user’s perspective, the message is mixed but ultimately positive.

5.1 Safer Funds, More Documentation

On the plus side:

- Customers get a stronger promise of full recovery in USD terms if their exchange is hacked.

- They benefit from better governance and oversight of system providers, cold-wallet operations, and asset segregation.

On the minus side:

- Expect more KYC, more forms, and more detailed disclosures—because regulators will demand evidence that exchanges truly understand and manage their risks.

- Fees may increase slightly as exchanges pass some reserve funding costs to users.

For long-term holders who care about counterparty risk, this is largely a net win: you might pay a bit more per trade, but your risk of being caught in a multi-year bankruptcy with uncertain recovery drops significantly.

5.2 Opportunities in “RegTech-Native” Tokens and Platforms

Regulation-heavy environments tend to reward:

- Infrastructure tokens that power KYC/KYT, Travel Rule, risk scoring, and compliance analytics.

- Layer-1s and L2s that integrate hooks for compliance (whitelists/blacklists, enterprise identity modules) without fully sacrificing decentralization.

- Custody, MPC, and wallet infrastructure projects that reduce the attack surface for cold-wallet operations.

For yield hunters and token pickers, Japan’s direction suggests:

- Assets that are “compliance-ready” and partner with regulated exchanges may see more stable volumes and institutional flows.

- Protocols that focus explicitly on security, monitoring, and risk transfer (rather than pure leverage or unsustainable APYs) could become the backbone of the next regulatory cycle.

6. Global Context: Japan as a Preview of Future Rules

Japan is not regulating in isolation. The move to introduce responsibility reserves sits alongside:

- The EU’s MiCA framework, which tightens requirements for crypto-asset service providers, stablecoin issuers, and custodians.

- Ongoing discussions in the US, UK, and other G20 countries about capital requirements and customer protection schemes for digital assets.

By anchoring its approach in familiar financial concepts—segregated assets, investor compensation mechanisms, systemic-risk awareness—Japan is creating a template that other regulators can adapt.

For builders targeting global markets:

- Designing your products, custody models, and treasury policies to meet Japan-grade standards is becoming a smart default.

- If your token, exchange, or protocol can survive Japanese compliance, chances are it will be well-positioned when similar rules emerge elsewhere.

7. Conclusion: Regulation as an Alpha Source?

Japan’s planned responsibility reserve is more than another compliance box. It marks a philosophical shift in how regulators think about crypto exchanges:

- From: “Make them segregate assets and secure cold wallets”

- To: “Assume breaches will happen—and pre-fund the damage so users are made whole quickly.”

For traders and investors searching for new assets and revenue streams, this environment can be used strategically:

- Favor exchanges and tokens that lean into strong regulatory frameworks rather than treating them as a burden.

- Look for protocols that enable risk transfer, insurance, security, and compliance tooling, as these are becoming core infrastructure for regulated crypto venues.

- Use Japan as an indicator jurisdiction: rules that work here are likely to spread.

In the medium term, this may reduce some high-risk, high-yield opportunities. But it simultaneously opens a new frontier: earning yield by underwriting, securing, and insuring the very rails on which regulated Web3 will run. For builders who can bridge regulation and innovation, that frontier may be one of the most durable sources of crypto “alpha” in the coming cycle.