Main Points :

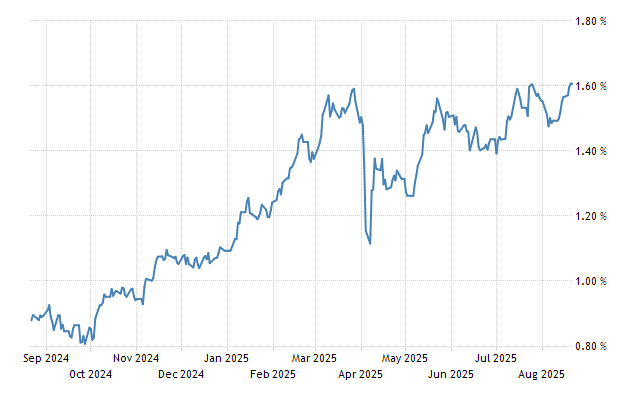

- Japan’s 10‑year JGB yield rose to over 1.61%, the highest since 2008, reflecting fiscal and policy concerns.

- Super‑long bond yields (20‑ and 30‑year) also surged—20‑year at ~2.64%, 30‑year at ~3.19%—raising volatility.

- Political uncertainty and weak bond auction results intensify investor wariness and could reduce demand for risk assets like crypto.

- BOJ faces pressure to raise rates amid inflation and yield spike; U.S. officials warn Japan is “behind the curve.”

- Despite bond-market fears, Japan equities and certain funds may still offer attractive valuations versus bonds or U.S. equities.

- Global bond markets are affected as yields rise synchronously; Fed cut expectations and crypto rallies suggest shifting investor appetite.

1. Yield Spike and Investor Concerns

Japan’s 10‑year government bond (JGB) yield climbed above 1.61% around August 20, 2025—the highest level since 2008—triggered by weak demand at a 20‑year JGB auction, coupled with worries over increased government spending and tax cuts. Data from TradingView shows 20‑year yields reached ~2.64%, and 30‑year yields soared to ~3.19%. This upward pressure stems from reduced support for longer-dated bonds and heightened fiscal risk.

2. Political Uncertainty and Fiscal Pressure

The sell-off in JGBs follows Prime Minister Ishiba’s political setback, fueling concerns about increased spending and tax relief, which would exacerbate Japan’s already large debt-to-GDP ratio at around 2.5×. Weak investor interest in super-long bonds—the weakest in over a decade—reflects market unease regarding fiscal management.

3. BOJ’s Dilemma: Normalization vs Stability

With JGB yields rising and surface volatility increasing, BOJ Governor Ueda warned that swings in super-long yield could influence shorter-term rates and economic conditions. BOJ has ended yield curve control and raised short-term rates to 0.5%, but cautious about further hikes without clear wage-driven inflation. U.S. Treasury Secretary Scott Bessent criticized Japan for being “behind the curve” and likely to raise rates, pressuring the BOJ to act.

4. Global Bond Market Contagion

The spike in long-term Japanese yields has rippled into global markets. U.S. and German long bond yields have risen—e.g., U.S. 30-year Treasuries surged by ~81 bps, Germany’s by ~36 bps. Reduced Japanese investment abroad—due to domestic bond allure—may lift yields elsewhere.

5. Implications for Risk Assets and Crypto

Higher yields on JGBs dampen the appeal of risk assets, including crypto and equities, as investors may shift toward safer fixed income. Still, global developments are tempering risk aversion: Reuters notes bitcoin recently soared to a record above US$124,000, fueled by crypto-friendly U.S. regulation and institutional flows. Lowering U.S. dollar strength underpins that move, as rate-cut expectations grow in the U.S.

6. Japan Equities: Still Attractive ?

Despite bond-market instability, analysts argue Japan equities remain compelling due to structural reforms and favorable valuations. Funds like WisdomTree Japan Opportunities and Japan Hedged Equity offer forward earnings yields that outperform domestic bonds and even U.S. equities, positioning them as attractive alternatives.

Summary

In late August 2025, Japan’s 10‑year JGB yield climbed above 1.61%—a 17‑year high—amid weak demand in long-term auctions and mounting political and fiscal unease. Super‑long bond yields also spiked, stirring volatility and investor caution. The Bank of Japan stands at a crossroad: normalize policy or preserve stability amid global contagion risks. Higher yields ripple globally, elevating developed sovereign yields and potentially dampening demand for riskier assets.

Yet, burgeoning developments—like crypto’s rally amid U.S. Fed rate-cut bets—suggest selective risk appetite persists. Meanwhile, Japan equities, bolstered by reforms and relative valuations, might offer strategic value for investors exploring new sources of returns.