Main Points :

- Japan Post Bank will introduce a blockchain‑based tokenized deposit currency, DCJPY, for depositors starting fiscal 2026.

- DCJPY is a tokenized deposit, not a stablecoin, issued on a permissioned blockchain by DeCurret DCP, part of the IIJ Group.

- Users can convert yen deposits into 1 yen = 1 DCJPY and use it for instant settlement of security tokens (STs), NFTs, and potentially public subsidies.

- The potential base of issuance includes around 120 million accounts and ¥190 trillion (~ $1.29 trillion) in deposits.

- Pilot use cases already include settling renewable energy certificates and digital bonds using DCJPY.

- Broader implications: Enhancing settlement efficiency, enabling programmable money for real‑world assets, and integrating digital payments into public finance.

1. Introduction

Japan Post Bank, one of the nation’s largest deposit holders, is gearing up to introduce a tokenized digital version of its deposit currency, called DCJPY, for retail depositors as early as fiscal 2026. This marks a significant stride in integrating blockchain‑based, programmable money into Japan’s mainstream financial infrastructure. The initiative targets digital asset enthusiasts and blockchain practitioners—offering a fresh avenue toward revenue generation and real‑world asset (RWA) utilization.

Japan Post Bank plans to enable customers to link a dedicated DCJPY account to their existing savings, allowing them to convert a portion of their yen deposits into DCJPY at a straightforward 1 yen = 1 DCJPY rate. Once converted, this digital yen can be used for settling security token (ST) transactions, NFTs, and potentially for disbursing local government grants and subsidies.

2. What Is DCJPY and How It Differs from Stablecoins

Unlike typical stablecoins, DCJPY is categorized as a “tokenized deposit”, meaning it represents actual yen deposits held at a bank—and is not treated legally as an “electronic payment instrument” like JPYC. Instead, DCJPY remains a deposit on a permissioned (private) blockchain run by regulated financial entities.

This contrasts with stablecoins (e.g., JPYC), which run on public blockchains and are broadly accessible. DCJPY is inherently restricted to authorized participants—embedded within Japan Post Bank’s ecosystem—rather than broadly transferable across public crypto networks.

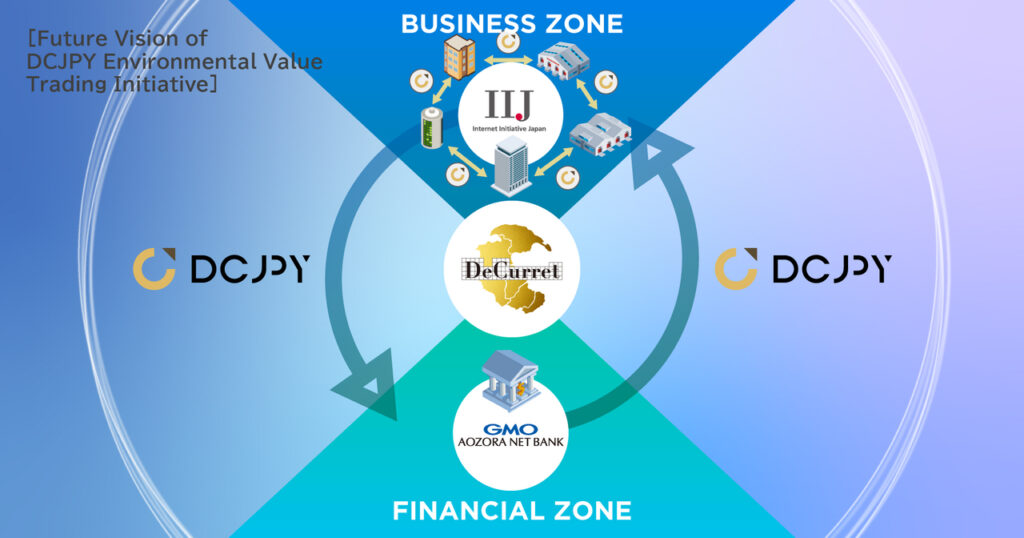

3. Technical Foundation and Pilot Use Cases

DCJPY is developed by DeCurret DCP, part of the IIJ Group, which has been launching DCJPY since mid‑2024. Production testing began in July 2024, and the platform officially entered production in late August 2024 in partnership with Internet Initiative Japan (IIJ) and GMO Aozora Net Bank, the first bank to tokenize deposits on DCJPY.

In an initial pilot, IIJ converted renewable energy certificates into blockchain‑based digital assets and settled payments using DCJPY held at GMO Aozora Net Bank—showcasing programmable settlement and environmental asset tokenization.

Separately, DeCurret DCP teamed with SMBC and BOOSTRY to run a Proof of Concept using DCJPY for digital bond settlement, achieving DVP (Delivery versus Payment) settlement with the fastest domestic corporate bond settlement in Japan (trade date +1 business day) .

4. Scale and Market Potential

Japan Post Bank holds roughly 120 million accounts with combined deposits amounting to approximately ¥190 trillion (~ $1.29 trillion). This enormous base becomes a potential springboard for DCJPY issuance, potentially elevating its prominence in Japan’s digital asset and tokenized deposits landscape.

Japan’s regulatory momentum is also building. With JPYC having received the first domestic stablecoin license in 2025, and the future tokenization market projected to grow from $600 billion in 2025 to $18.9 trillion by 2033 (per BCG and Ripple), the DCJPY initiative aligns with a broader shift toward digital, programmable finance.

5. Strategic Benefits and Future Implications

- Instant Settlement: DCJPY allows for near‑instantaneous conversion and settlement of financial digital assets, solving lag issues in traditional processes.

- Programmability: Through smart contracts, DCJPY enables automated transaction flows—for example, digital bonds, NFTs, or environmental credit settlements.

- Public Finance Integration: Local governments may use DCJPY to distribute grants or subsidies digitally, reducing administrative friction.

- Trusted Infrastructure: As a deposit-backed asset issued by a regulated institution, DCJPY offers high security and trust for users.

- Financial Innovation Leadership: Japan Post Bank’s move places Japan at the cutting edge of integrating blockchain tokens with traditional banking.

6. Summary

In summary, Japan Post Bank’s plan to roll out DCJPY—a blockchain‑based, deposit‑backed digital currency—in fiscal 2026 represents a notable stride in integrating FinTech with mainstream banking. Backed by DeCurret DCP and tested through real‑world pilots (including environmental assets and digital bond settlements), DCJPY offers near‑instant, programmable settlement while remaining secure and closely regulated.

The immense scale of Japan Post Bank’s deposits, combined with evolving regulatory frameworks and booming tokenized asset markets, suggests DCJPY could significantly reshape Japan’s financial infrastructure. From enabling seamless digital payments to embedding programmable finance into public services, DCJPY emerges as a promising development for blockchain innovators and crypto-savvy users alike.