Main Points :

- Major global exchanges urge the U.S. SEC to reassess broad exemptions granted to crypto firms offering tokenized equities.

- Concerns center on investor protection, market integrity, and fair competition between regulated securities exchanges and lightly regulated crypto platforms.

- Tokenized securities markets are growing rapidly, but inconsistent oversight poses systemic risk.

- Recent developments—including Nasdaq’s application to enable tokenized securities trading—signal accelerating institutional interest.

- The World Federation of Exchanges (WFE) urges the SEC to impose narrow, temporary, purpose-specific exemptions, not broad permissions.

- These discussions will shape the framework for tokenized stocks, stablecoin-based settlement, and blockchain-enabled capital markets in the U.S.

Introduction: A Turning Point for Tokenized Securities

The accelerating development of tokenized financial instruments—including tokenized equities, treasury bills, and real-world assets—is reshaping global capital markets. Yet this rapid innovation has also raised urgent regulatory concerns. On November 21, the World Federation of Exchanges (WFE), whose members include Nasdaq, the Chicago Board Options Exchange, and the CME Group, issued a formal letter to the U.S. Securities and Exchange Commission’s (SEC) crypto task force. The letter requests a reassessment of broad exemptions currently granted to certain cryptocurrency platforms that offer tokenized stocks.

According to the WFE, these exemptions may allow crypto exchanges to function like regulated securities exchanges—without meeting the fundamental regulatory requirements that have shaped global markets for decades. As tokenized financial instruments expand into a multi-billion-dollar segment of the digital asset economy, this conflict between innovation and investor protection is becoming increasingly difficult to ignore.

Section 1: Why the WFE Is Raising the Alarm

The WFE’s letter highlights intensifying concerns over the rising number of crypto platforms offering tokenized U.S. equities. These products are often marketed as “stock tokens,” implying that they represent a true 1:1 share in the underlying equity. However, the WFE points out that many of these instruments are not actual stocks, but synthetic or derivative products lacking the full rights associated with traditional equity ownership.

This misalignment creates several risks:

1. Investor Risk Due to Lack of Disclosure

Traditional securities issuers must comply with stringent disclosure requirements designed to protect investors. Crypto platforms offering tokenized equities may bypass these rules entirely.

2. Uneven Competitive Landscape

Regulated exchanges must invest heavily in compliance systems, reporting frameworks, clearing mechanisms, and surveillance tools.

Crypto exchanges, exempt from these obligations, may offer similar products at lower cost—creating structural inequality.

3. Systemic Risk and Liquidity Concerns

Tokenized products often operate without standardized settlement rules, custody safeguards, or regulatory capital requirements.

The WFE makes it clear: exemptions should be used only sparingly—limited to cases where they genuinely benefit investors and ensure fair competition.

Section 2: Appropriate vs. Inappropriate Exemptions

The WFE acknowledges that exemptions can play an important role in enabling innovation. Reasonable exemptions include:

- Allowing blockchain-based firms to avoid paper-based record-keeping obligations.

- Allowing alternative custody structures that do not rely on traditional centralized custodians.

However, the WFE warns against exemptions that undermine decades-old regulatory principles. Specifically, exemptions should not be used to:

- Permit firms to avoid basic investor-protection rules.

- Allow crypto exchanges to operate de facto securities markets without oversight.

- Enable tokenized products to be sold as “equivalent to stocks” when they do not hold voting rights, dividend rights, or shareholder protections.

The letter explicitly recommends that the SEC adopt:

- Narrowly defined exemptions

- Time-limited waivers

- Gradual deployment phases designed for data collection and risk assessment

This phased approach would allow regulators to evaluate impacts before establishing permanent rules.

Section 3: Global Momentum—Tokenized Securities Enter the Mainstream

The timing of the WFE’s letter is not coincidental. In September, Nasdaq formally applied to the SEC for approval to list and trade tokenized securities. If granted, this would mark the first time a major U.S. securities exchange enters the tokenized asset market.

Other recent developments include:

- BlackRock and major issuers expanding tokenized U.S. Treasury markets.

- Stablecoin issuers exploring institutional settlement channels.

- Broker-dealers piloting blockchain-based settlement networks.

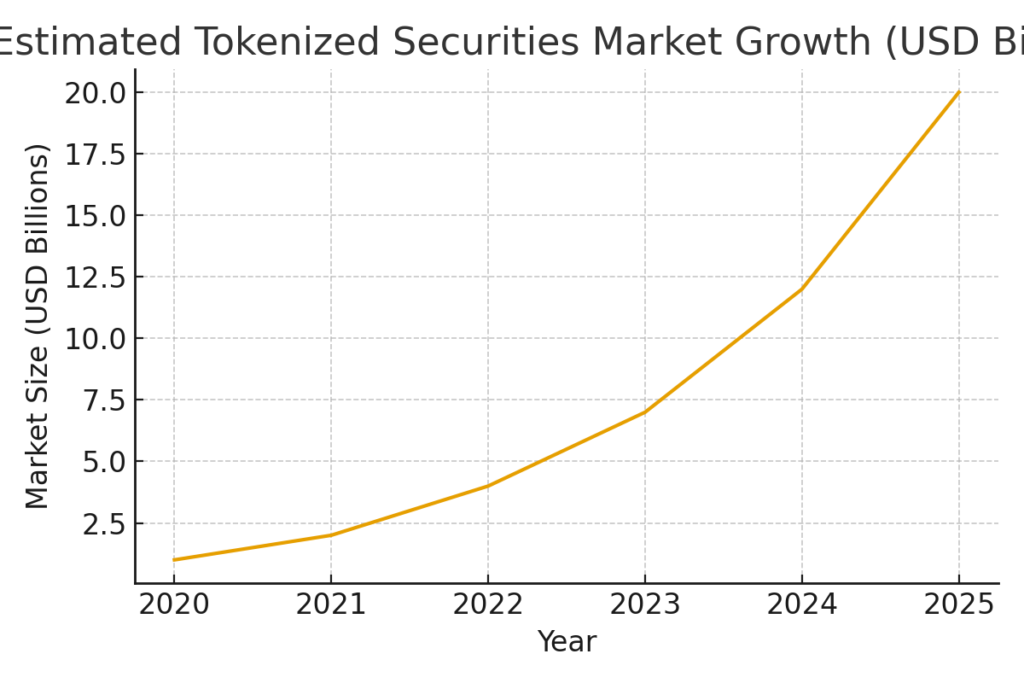

The tokenized asset market is projected to exceed $20 billion in 2025, driven by institutional demand.

Section 4: Recent Trends & Global Moves Toward Standardization

To provide additional context beyond the referenced article, recent developments across major jurisdictions highlight the growing need for standardized rules:

United States

- The SEC continues enforcement actions against platforms selling tokenized equities without registration.

- FINRA has begun reviewing digital asset communications and brokerage structures.

Europe

- The European Securities and Markets Authority (ESMA) is evaluating tokenization under MiCA.

- Germany allows tokenized investment funds and debt instruments under eWpG.

Asia

- Hong Kong is preparing a licensing framework for tokenized securities intermediaries.

- Singapore is piloting Project Guardian, a multi-bank tokenization initiative with JPMorgan and DBS.

Middle East

- The UAE is integrating tokenization rules within its virtual asset regulatory framework.

Across all jurisdictions, regulators are converging on three priorities:

- Investor Protection

- Market Integrity

- Fair Competition

These match the core principles emphasized by the WFE.

Section 5: Why Tokenization Is Expanding—Practical Use Cases

Tokenization offers several tangible benefits driving its adoption:

1. Fractional Ownership

Expensive assets such as U.S. equities, real estate, or T-bills can be split into smaller digital units, broadening investor access.

2. 24/7 Global Settlement

Unlike traditional markets, tokenized assets can settle instantly and operate globally without market-hour constraints.

3. Transparent On-Chain Records

Blockchain-based record-keeping reduces reconciliation errors and allows instant auditing.

4. Cost Efficiency

Tokenization reduces reliance on intermediaries and lowers settlement costs.

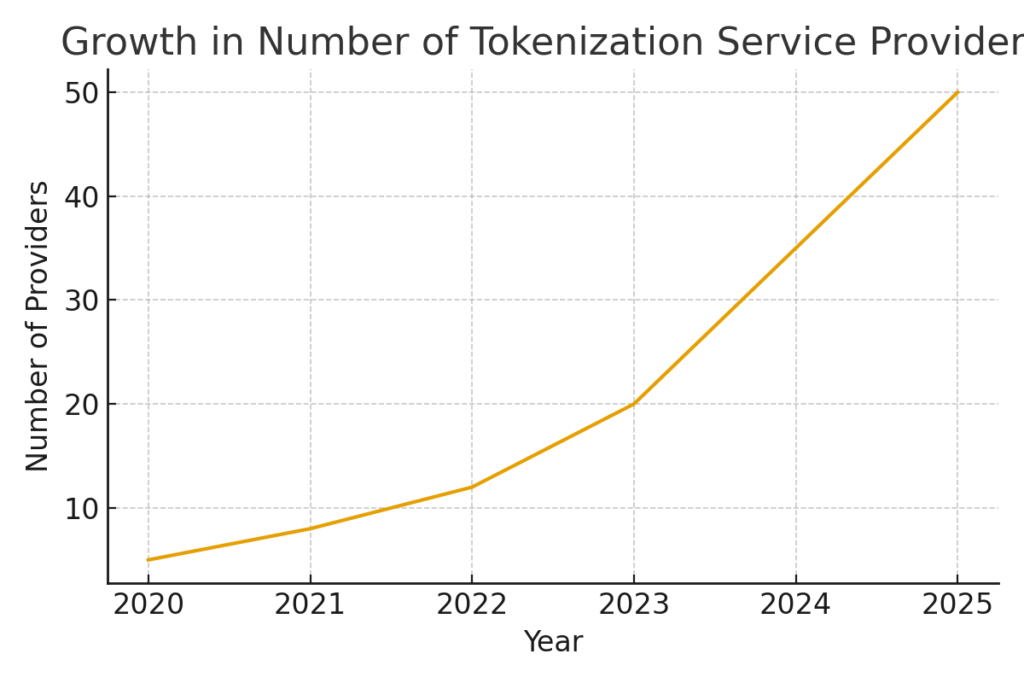

The number of tokenization platforms is estimated to have grown sharply over the last five years.

Section 6: What the WFE Wants from the SEC

The WFE’s proposals to the SEC include:

- Align crypto-asset exemptions with the principles of the International Organization of Securities Commissions (IOSCO).

- Implement rules ensuring fairness between crypto platforms and traditional exchanges.

- Limit exemptions to narrow, temporary, purpose-built cases.

- Require transparent rule-making processes including public consultation.

- Implement testing phases before permanent adoption.

From the WFE’s perspective, tokenization will succeed only if built upon regulatory principles that have proven effective for decades.

Conclusion: The Future of Tokenized Securities Hinges on Balanced Regulation

Tokenized securities are poised to redefine capital markets. But the path forward must address the regulatory friction between innovation and investor protection. The WFE’s intervention signals growing pressure from major market infrastructure operators who believe that crypto firms should not circumvent long-standing regulatory safeguards through broad exemptions.

The SEC’s ultimate stance will shape the future of tokenized equities, tokenized treasuries, and blockchain-enabled financial markets in the United States. For investors and builders, the message is clear: tokenization is entering its institutional phase, but success requires transparent, fair, and enforceable rules.