Key Points :

- Oil prices declined sharply due to renewed U.S.–Iran negotiation expectations

- Inflation concerns eased as U.S. PPI came in below expectations

- Equity markets rallied, led by tech and financial sectors

- Bitcoin surged toward recent highs, benefiting from macro stabilization

- Global policy signals from IMF, World Bank, and G7 are shaping capital flows

- Crypto markets show increasing decoupling from traditional risk assets

1. A Turning Point in Geopolitics: Oil Declines on U.S.–Iran Negotiation Hopes

The global macro landscape shifted meaningfully on April 15, 2026, as markets reacted to renewed optimism surrounding a second round of negotiations between the United States and Iran. Expectations that discussions toward a ceasefire or extended diplomatic arrangement could take place as early as the coming weekend triggered a rapid decline in oil prices, with WTI crude falling toward approximately $90.69.

This development represents more than a simple commodity price adjustment—it signals a broader recalibration of geopolitical risk. For months, elevated tensions in the Middle East had fueled energy price spikes, embedding inflationary pressures into the global economy. The mere anticipation of reduced conflict risk was enough to unwind a significant portion of those gains.

From a structural standpoint, oil remains one of the most sensitive macro indicators. It directly impacts transportation costs, manufacturing input prices, and consumer inflation expectations. As such, the drop in oil prices immediately translated into a more favorable outlook for inflation, creating ripple effects across multiple asset classes.

Interestingly, reports also indicated that Iran was considering temporary disruptions to maritime transport through the Strait of Hormuz. While this might appear contradictory, markets interpreted the broader diplomatic engagement as a dominant factor, outweighing localized risks. This underscores a key principle: markets price direction, not isolated events.

2. Inflation Relief and Bond Market Reaction

Parallel to the geopolitical developments, U.S. macroeconomic data provided additional support to the “softening inflation” narrative. The March Producer Price Index (PPI) came in below expectations, reinforcing the idea that upstream price pressures are beginning to moderate.

This data point is particularly important because PPI often acts as a leading indicator for consumer inflation. Lower wholesale prices typically translate into reduced cost pressures for businesses, which may eventually pass through to consumers.

As a result, U.S. Treasury bonds rallied, pushing yields lower. This inverse relationship between bond prices and yields reflects increased demand for fixed-income assets in a lower-inflation environment. Investors began recalibrating expectations for future Federal Reserve policy, with a reduced likelihood of aggressive tightening.

However, it is critical to note that inflation has not disappeared. Oil prices, despite their recent decline, remain historically elevated, and certain components of the Personal Consumption Expenditures (PCE) index continue to show resilience. This creates a nuanced environment where inflation is easing, but not fully resolved.

3. Equity Markets Surge: Tech and Financials Lead the Rally

With inflation fears subsiding, equity markets responded decisively. The S&P 500 climbed to approximately $6,967.38, approaching its late-January highs. This rally was not uniform across sectors.

Energy stocks, which had benefited from elevated oil prices, saw their gains eroded. In contrast, technology and financial sectors emerged as leaders. Lower interest rate expectations tend to disproportionately benefit growth-oriented companies, whose valuations are sensitive to discount rates.

Financial institutions also gained momentum, as improved macro stability reduces credit risk and supports lending activity. This sector rotation reflects a broader shift in investor sentiment—from defensive positioning toward risk-on strategies.

The Japanese equity market mirrored this trend, with the Nikkei 225 approaching ¥58,201 (approximately $387 USD), highlighting the global nature of this risk re-pricing.

4. Crypto Markets: Stability, Strength, and Structural Evolution

(Graph: Oil Price vs Bitcoin Price Correlation – showing inverse macro pressure effect)

One of the most compelling developments in this macro shift is the behavior of cryptocurrency markets—particularly Bitcoin. As oil prices declined and inflation concerns eased, Bitcoin climbed toward $74,497, marking a four-week high.

Traditionally, Bitcoin has been viewed as a hedge against inflation and monetary debasement. However, recent price action suggests a more nuanced role. Rather than purely benefiting from inflation fears, Bitcoin appears to thrive in macro stability environments where liquidity expectations improve.

This challenges the simplistic narrative of Bitcoin as “digital gold.” Instead, it increasingly behaves as a hybrid asset—part hedge, part risk asset, and part liquidity proxy.

Ethereum, priced around $2,336.51, showed slight weakness, reflecting short-term rotation rather than structural decline. Meanwhile, Solana ($83.82) and XRP ($1.36) traded within consolidation ranges, indicating that altcoins are still searching for directional momentum.

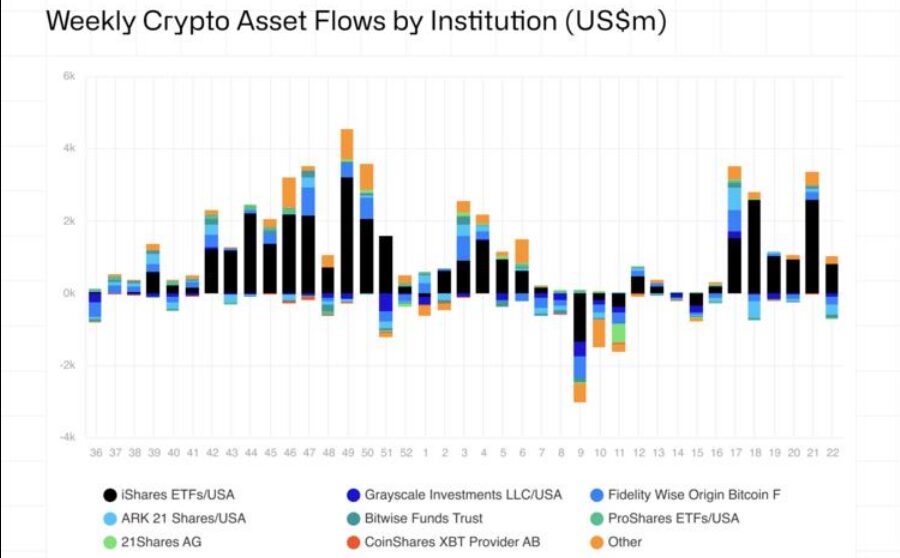

5. Institutional Flows and ETF Dynamics

(Graph: Crypto ETF Net Inflows and Price Recovery Trend)

Another critical driver of the current crypto landscape is institutional participation. Exchange-traded funds (ETFs) have become a primary gateway for traditional capital to enter digital assets.

Recent data indicates steady net inflows into crypto ETFs, even amid macro uncertainty. This suggests that institutional investors are not merely reacting to short-term price movements—they are strategically allocating capital based on long-term theses.

The interaction between ETF inflows and price recovery highlights a reinforcing cycle:

- Rising prices attract institutional inflows

- Inflows provide liquidity support

- Liquidity stabilizes volatility and encourages further participation

This dynamic represents a structural maturation of the crypto market, moving it closer to traditional asset classes in terms of capital behavior.

6. Global Policy Signals: IMF, World Bank, and G7 Influence

The ongoing IMF and World Bank Spring Meetings, alongside the G7 Finance Ministers and Central Bank Governors meeting, add another layer of complexity to the macro environment.

These gatherings are not merely symbolic—they shape expectations around:

- Monetary policy coordination

- Currency stability

- Global growth outlook

For example, speculation around a potential rate hike by the Bank of Japan remains limited (around 30%), which has constrained the appreciation of the yen. However, rising inflation forecasts in Japan—driven partly by energy prices—could shift this outlook.

Currency markets remain highly sensitive to these policy signals. The Japanese yen strengthened toward the ¥158 range per dollar (approximately $0.0063 per yen), reflecting a cautious rebalancing of global capital flows.

7. Strategic Implications for Crypto Investors and Builders

For readers seeking new crypto assets, revenue opportunities, and practical blockchain applications, the current environment offers several key insights:

A. Macro Stability Is Becoming Bullish for Crypto

Contrary to earlier cycles, crypto is no longer solely dependent on crisis-driven narratives. Stability itself can be a catalyst.

B. Institutional Adoption Is Reshaping Market Structure

ETF flows and regulated products are reducing volatility and increasing legitimacy.

C. Altcoin Differentiation Is Critical

Not all assets will benefit equally. Projects with real utility—particularly in payments, DeFi infrastructure, and cross-border settlements—are likely to outperform.

D. Integration with Traditional Finance Is Accelerating

Stablecoins, tokenized assets, and blockchain-based payment rails are increasingly embedded in global financial systems.

Conclusion

The convergence of geopolitical easing, declining oil prices, and moderating inflation has created a powerful tailwind for global markets. Equities have surged, bonds have stabilized, and cryptocurrencies—led by Bitcoin—have demonstrated resilience and adaptability.

What distinguishes this cycle from previous ones is the evolving role of crypto within the broader financial ecosystem. No longer confined to niche speculation, digital assets are becoming integral to capital allocation strategies, institutional portfolios, and real-world financial infrastructure.

For investors and builders alike, the message is clear: the next phase of crypto growth will be driven not by hype, but by integration, utility, and macro alignment.