Main Points :

- 2025 was not a “lost year” for crypto, but a structural reset marked by regulatory clarity and institutional integration.

- Regulatory uncertainty declined sharply, particularly in the United States and the EU, lowering systemic risk.

- Institutional capital, driven by ETFs, custodial reforms, and tokenization of real-world assets (RWA), stabilized market infrastructure.

- 2026 is likely to represent a transition from speculative expectations to real economic demand for blockchain-based assets and services.

- For investors and builders, the opportunity shifts from short-term price action to long-term utility, cash flow, and integration with traditional finance.

1. Pantera Capital’s View: 2025 as a Year of Structural Progress

In its annual report titled “The Year of Structural Progress,” U.S.-based crypto hedge fund Pantera Capital argues that 2025 should be understood not as a period of stagnation, but as a foundational year for the next growth cycle.

While headline price performance of major assets such as Bitcoin and Ethereum fell short of market expectations, Pantera emphasizes that risk across the system materially declined. The drivers of this shift were not speculative hype, but structural developments: clearer regulations, institutional-grade market access, and improved liquidity frameworks.

According to Pantera, these changes collectively reduced uncertainty and volatility at the macro level. As a result, the crypto market entered 2026 with a fundamentally stronger base than in previous post-bull-market cycles.

2. Building the Foundation: What Changed in 2025?

2.1 Regulatory Clarity in the United States and Beyond

One of the most significant developments in 2025 was the acceleration of regulatory clarity, especially in the United States.

Following the establishment of a pro-crypto administration in early 2025, a federal working group on digital assets was formed to address market structure, stablecoins, taxation, and custody. The U.S. Securities and Exchange Commission (SEC) launched a dedicated crypto task force and reversed several previously aggressive enforcement positions.

Notably:

- The SEC clarified that many digital assets do not constitute securities.

- Enforcement actions against major crypto firms were withdrawn.

- Explicit guidance confirmed that certain stablecoins and staking activities fall outside securities regulation.

- The controversial bank custody guidance SAB 121 was effectively rolled back, allowing banks to offer crypto custody services more freely.

On the legislative front, the U.S. Congress passed the GENIUS Act, establishing the first federal framework for payment-oriented stablecoins. While the broader CLARITY Act, intended to comprehensively define crypto market structure, remained under deliberation, the direction of travel became clear.

In parallel, the European Union continued implementing MiCA (Markets in Crypto-Assets Regulation), reinforcing legal certainty across major economies.

Result: By the end of 2025, crypto regulation in leading jurisdictions shifted from ambiguity to enforceable clarity—a prerequisite for institutional-scale participation.

3. Institutional Capital and Market Stabilization

3.1 The ETF Effect

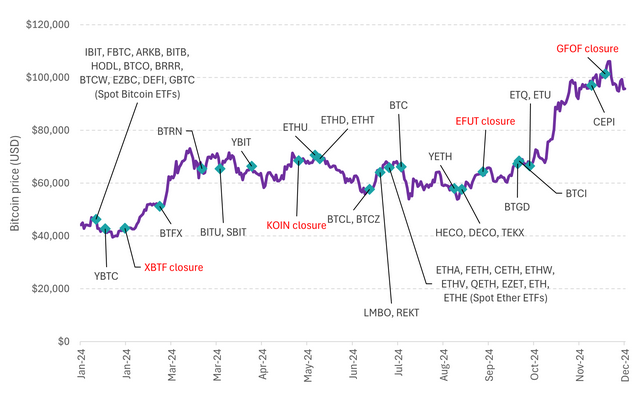

Institutional adoption accelerated most visibly through exchange-traded funds (ETFs). In the United States, spot ETFs for Bitcoin and Ethereum were joined by products tracking assets such as Solana (SOL) and XRP.

According to industry estimates, net inflows into U.S. Bitcoin spot ETFs reached approximately $22 billion in 2025.

[Annual Net Inflows into U.S. Crypto ETFs (USD)]

These ETFs transformed crypto exposure from a niche allocation into a compliance-ready institutional product, enabling pension funds, asset managers, and corporates to participate without operational complexity.

3.2 Crypto Firms Enter Traditional Finance

Another symbolic milestone was the inclusion of Coinbase in the S&P 500. This marked one of the first times a crypto-native company became embedded in the core of U.S. equity markets.

At the same time, platforms such as Robinhood expanded tokenized stock trading, while tokenization of real-world assets (RWA)—including government bonds and real estate—gained momentum.

These developments blurred the line between traditional finance and blockchain infrastructure.

4. Liquidity, Stablecoins, and Market Infrastructure

Pantera also highlights growth in stablecoin supply and improved liquidity conditions throughout 2025. Stablecoins increasingly functioned as on-chain cash equivalents, facilitating settlement, cross-border payments, and DeFi activity.

Improved custody solutions, clearer accounting treatment, and growing institutional participation collectively strengthened market plumbing. In Pantera’s assessment, 2025 was the year crypto infrastructure matured enough to support sustained real demand.

5. Looking Ahead: Why 2026 May Be the Breakout Year

5.1 Institutional Forecasts

Major financial institutions have begun articulating constructive outlooks for 2026.

- JPMorgan noted that while market capitalization temporarily contracted in 2025, regulatory easing reinforced long-term fundamentals.

- BlackRock transferred crypto assets valued at approximately $123.47 million (including BTC and ETH) to Coinbase in early 2026, signaling continued exposure rather than exit.

- 21Shares projects that total crypto ETF assets under management could exceed $400 billion by the end of 2026.

[Projected Global Crypto ETF AUM Growth (USD)]

5.2 From Expectation to Utilization

Pantera’s core thesis is that 2026 represents a psychological and economic shift:

from narratives and expectations to measurable usage and cash-flow-driven demand.

Key growth vectors include:

- Tokenized financial instruments

- Stablecoin-based payments and settlement

- Blockchain-based custody and compliance tools

- Enterprise adoption of on-chain infrastructure

For investors, this implies a move away from purely speculative trades toward assets and protocols that generate sustainable economic activity.

6. Strategic Implications for Investors and Builders

For readers seeking new digital assets or revenue opportunities, the implication is clear:

- Short-term volatility matters less than structural positioning.

- Assets aligned with regulation, institutional access, and real-world integration are better positioned.

- Wallets, custody, payments, and RWA platforms may outperform purely narrative-driven tokens.

2026 is not expected to be a simple replay of past bull markets, but rather a more mature, utility-driven expansion phase.

Conclusion: A New Phase for Crypto Markets

The apparent stagnation of 2025 masked a profound transformation. Regulatory clarity, institutional integration, and infrastructure maturity collectively reshaped the crypto market’s risk profile.

As Pantera Capital argues, these changes did not suppress growth—they prepared the conditions for it.

If expectations align with execution, 2026 may mark the beginning of crypto’s transition from an emerging asset class to a core component of global financial infrastructure.