Main takeaways :

- MSCI is contemplating removing from its indexes companies whose balance sheets are dominated by crypto assets (50%+), which may push institutional capital from corporate-held Bitcoin to spot Bitcoin ETFs.

- The likely exclusion affects major “crypto-treasury” firms such as MicroStrategy (also referred to as “Strategy” or “MSTR”), potentially triggering billions of dollars in passive–fund outflows.

- This structural shift could rewire how Bitcoin exposure is obtained — favoring ETFs over equity exposures — changing the ecosystem of institutional Bitcoin investment and reducing “leverage-through-equity” risk.

- For investors, the change underscores the growing dominance of spot-Bitcoin ETFs as transparent, fungible, and regulation-friendly vehicles — and may open room for new altcoins or crypto-native funds.

- The debate raises broader questions about classification: when a company holds mostly crypto, is it a “business company” or effectively an “investment fund”? The classification could redefine which kinds of firms are eligible for mainstream equity indices.

Background — Why MSCI Is Pushing This Change

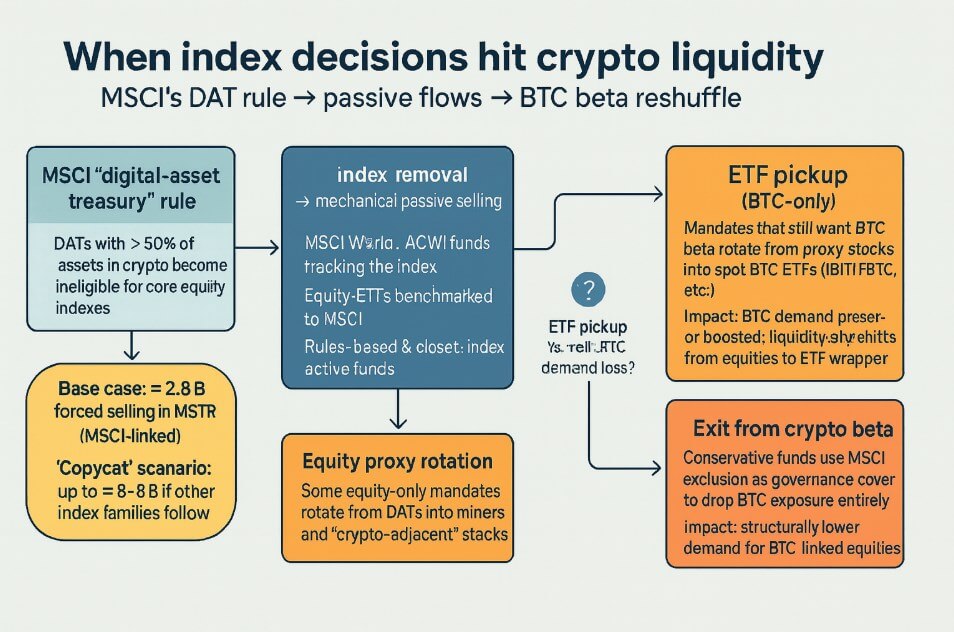

The global index provider MSCI has recently opened a consultation on whether to exclude companies whose portfolios are dominated by digital assets — especially firms holding crypto as treasury rather than operating an active business. Under the proposed rule, any company whose digital-asset holdings exceed 50% of total assets would be deemed ineligible for the firm’s “Global Investable Market” indices.

The rationale is simple: traditional indices are meant to reflect operational, business-driven companies — firms that run real operations, not just hold assets. If a publicly listed company’s value depends primarily on crypto holdings, it arguably behaves like a fund or holding company rather than an operating business.

That’s why companies like MicroStrategy — which hold massive amounts of Bitcoin (BTC) on their balance sheet — are now under scrutiny. Under the new criteria, they may be excluded as “digital-asset treasuries.”

What This Means for Crypto-Holding Firms: The Risk of Forced Outflows

If the rule goes through, firms like MicroStrategy risk being removed from major equity benchmarks in the next rebalancing cycle (targeted for February 2026, with decision expected by mid-January) following the ongoing consultation.

Institutional investors and passive funds that track MSCI indices would likely be forced to sell their holdings in such firms — resulting in potentially massive outflows. One estimate by JPMorgan Chase & Co. (JPMorgan) puts the outflows from MicroStrategy alone at around US$2.8 billion.

Other analyses suggest that if multiple index providers follow MSCI’s lead, total passive outflows could reach as high as US$8–9 billion, or even more depending on the number of affected firms.

The market is already reacting: MicroStrategy’s share price has reportedly dropped more than 60% from its 2024 peak — eliminating the “mNAV premium” (the premium paid for its shares relative to the net value of Bitcoin held).

For newer funding vehicles issued by these firms (e.g., preferred shares, notes), the risk is even clearer: yields have risen (indicating higher perceived risk), and some offerings have already underperformed after issuance.

In sum: for firms whose primary business is holding crypto, being stripped from an index can trigger a self-fulfilling collapse in share price via forced passive outflows, depressed valuations, and impaired access to capital.

What This Means for Bitcoin and ETFs — A Structural Shift in Institutional Flow

This potential exclusion by MSCI marks more than just a shake-up for a few firms — it could reshape how institutions access Bitcoin.

- From leverage-through-equity to direct exposure via ETFs

- For years, some institutions gained Bitcoin exposure indirectly by buying shares in companies like MicroStrategy — effectively a leveraged play on BTC.

- With the risk of index exclusion, that pathway weakens. Instead, institutions may gravitate toward spot-Bitcoin ETFs offered by major asset managers. These funds offer direct exposure to BTC, are transparent, and generally have fewer regulatory or classification issues.

- Indeed, several recent reports suggest demand for spot-Bitcoin ETFs has surged — and that funds offering them (e.g., by major asset managers) are being increasingly perceived as the “purest” form of institutional BTC exposure.

- Reduced equity-linked risk and volatility

- Stocks like MicroStrategy carry additional risks beyond BTC volatility — equity-market risk, index-tracking risk, funding risk, corporate risk.

- ETFs, in contrast, may offer a cleaner risk profile: exposure to BTC price, but without corporate or equity-funding variables. For institutional funds seeking “crypto exposure without corporate risk,” this is appealing.

- Potential reallocation toward altcoins or new crypto-native funds

- As equity-linked BTC vehicles come under pressure, institutional capital freed from passive funds may flow into alternative crypto investments — altcoin funds, decentralized-finance (DeFi) strategies, or future ETFs for other assets (like ETH).

- This might broaden the base of interest beyond BTC, benefiting diverse blockchain ecosystems and spurring innovation.

- Regulatory clarity and classification standardization

- By challenging the classification of “crypto-treasury companies,” MSCI forces the market to confront a fundamental question: what counts as a “real business”?

- A clearer standard benefits the broader crypto industry — investors know what kind of firms are index-eligible, and companies focused on actual business operations (not just crypto holding) may attract more support.

Recent Market Developments: Signs of the Shift Already Underway

The theoretical debate is already manifesting in real-world actions:

- According to multiple crypto-news sources, institutions reportedly sold off roughly US$5–6 billion in equity holdings tied to firms like MicroStrategy over the past quarter. The selling pressure is attributed to both ETF demand and index-exclusion risk.

- Simultaneously, spot- and altcoin-ETF demand appears to be rising. One report notes that after the exclusion risk surfaced, inflows into spot-Bitcoin ETFs resumed and even accelerated, with ETF providers being viewed as safer “pure crypto” vehicles.

- Further, the broader regulatory environment seems to be tightening: in Asia, some exchanges have begun scrutinizing companies that promote themselves as “digital asset treasuries,” limiting their ability to list or expand — which may disincentivize future corporate-treasury style Bitcoin holdings.

These moves indicate that the market is already pricing in MSCI’s potential rule — institutional investors are reallocating, and the industry may be entering a new phase where crypto exposure is standardised around ETFs rather than equity-based plays.

Implications for Crypto Investors & Blockchain-Oriented Projects

For readers like you — interested in new crypto assets, blockchain applications, and potential revenue streams — this structural shift offers several important takeaways:

- Increased legitimacy and liquidity for spot-crypto ETFs. As institutional capital shifts away from equity-based crypto exposure, spot-Bitcoin ETFs will likely attract more inflows, improving liquidity and reducing volatility.

- Opportunity for altcoins and DeFi projects. With capital freed from equity-linked BTC holders, some of that may flow into altcoins, DeFi, and blockchain infrastructure projects — presenting opportunities for early investors and developers alike.

- Clearer differentiation between “treasury-holding firms” vs. “operational blockchain businesses.” Companies that build real products — DeFi platforms, blockchain-native services, token projects — may receive more favorable treatment compared to pure-holding firms.

- Potential downward pressure on “company-stock as BTC proxy” valuations. Investors should be cautious about companies whose value depends heavily on their crypto treasuries — these may see restricted access to passive capital, depressed valuations, and increased volatility.

- A turning point for institutional adoption. The shift may mark the beginning of a new era where Bitcoin and crypto become standard components of institutional portfolios — but via regulated, transparent instruments like ETFs, rather than high-beta equity plays.

What Could Go Wrong — Risks & Unintended Consequences

Of course, the proposed change by MSCI — and the subsequent market adjustments — are not without risks:

- Forced selling could destabilize markets. If many passive funds dump their shares in crypto-treasury firms simultaneously, the resulting downward pressure could ripple across equity and crypto markets.

- Concentration risks in ETFs. As capital flows into a few major ETFs, the crypto exposure of institutional investors becomes concentrated — which could reduce diversification and create systemic dependencies.

- Reduced incentives for firms building real crypto businesses. While the reform favors operational blockchain firms, it could discourage the creation or listing of new “crypto treasury” companies — perhaps disincentivizing firms from building long-term crypto balance sheets.

- Regulatory and classification uncertainty remains. The debate around what constitutes a “business company” vs. “investment company” may continue to evolve; depending on jurisdictions, different criteria may apply, leaving some regulatory gray zones.

Conclusion — A Structural Inflection Point for Institutional Crypto

The deliberations by MSCI reflect a deeper reexamination of how crypto belongs in global financial markets. By potentially excluding companies whose assets are largely crypto holdings, MSCI isn’t just targeting a handful of firms — it’s redefining how institutional capital can access Bitcoin.

The likely result is a shift away from equity-based crypto exposure (e.g., via companies like MicroStrategy) toward direct, transparent, and regulated instruments such as spot-Bitcoin ETFs. For crypto investors, developers, and blockchain-native entrepreneurs, this shift carries both risk and opportunity.

On one hand, it could usher in a new wave of institutional acceptance, liquidity, and mainstream integration for crypto — creating fertile ground for altcoins, DeFi protocols, and other blockchain-based innovations. On the other, firms that treated crypto as a treasury asset may struggle, causing revaluation and volatility.

In short: we are potentially witnessing a pivotal moment — not just for Bitcoin, but for how crypto is structurally embedded into global finance. For those looking for the next frontier, this evolving landscape may offer more clarity, better tools, and new opportunities.