Main Takeaways :

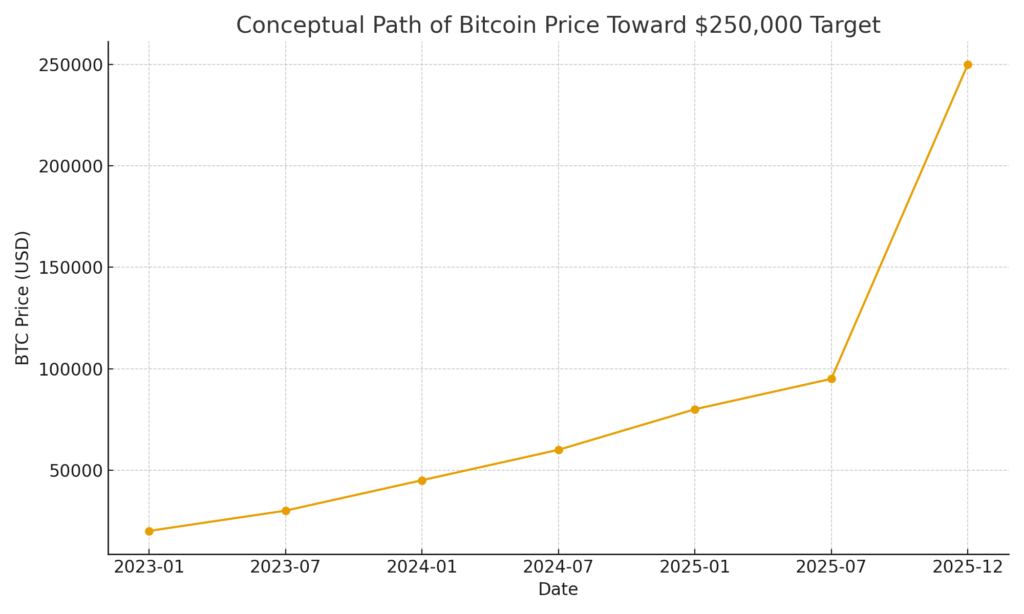

- Arthur Hayes still targets $250,000 per Bitcoin by end-2025, arguing that dollar liquidity has bottomed and that the end of quantitative tightening (QT) plus future rate cuts will push fresh capital into risk assets like BTC.

- Bitcoin recently fell toward the low-$80,000 range before rebounding above $90,000, which Hayes frames not as the start of a bear market but as a “flush” driven by ETF basis trades unwinding, not real institutional exit.

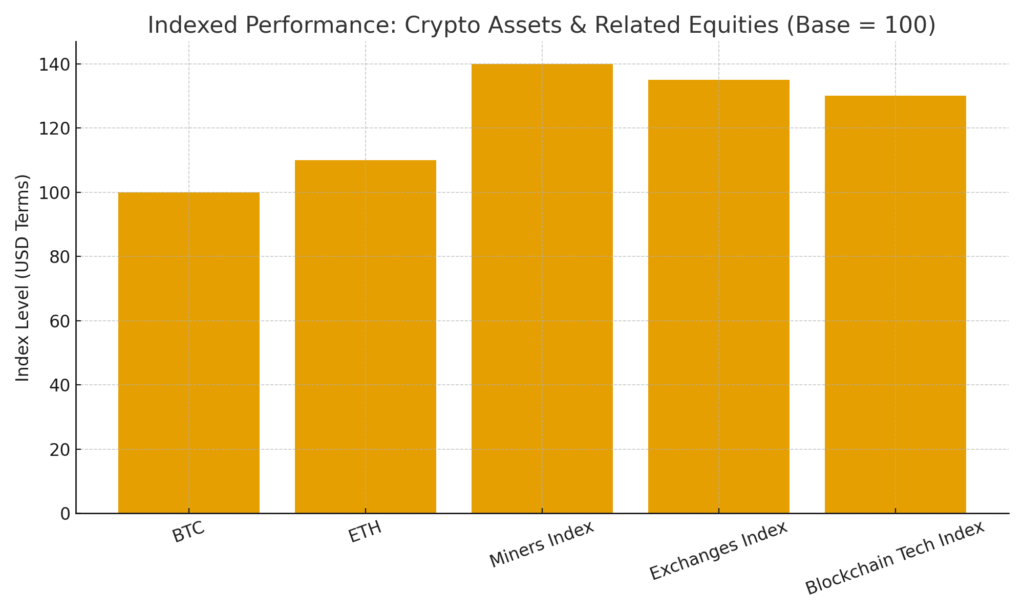

- Crypto-related stocks—especially miners, exchanges, and blockchain infrastructure plays—have rallied sharply alongside BTC and ETH, suggesting a renewed “risk-on” appetite extending beyond coins into public equity markets.

- Ethereum is entering its second major upgrade cycle of 2025 with the “Fusaka” hard fork, focused on PeerDAS data sampling, Verkle trees, and significant rollup scalability, following the Pectra upgrade earlier in the year.

- For investors hunting new revenue streams and practical blockchain use cases, this macro + tech backdrop suggests three themes:

- Directional BTC exposure anchored in the liquidity thesis.

- Equity plays on miners, exchanges, and infrastructure providers.

- Ethereum + L2 ecosystems poised to benefit from Fusaka-driven fee and scalability improvements.

1. Arthur Hayes’ $250,000 Bitcoin Target and the “Liquidity Bottom” Thesis

Arthur Hayes, co-founder and former CEO of BitMEX, has become one of the loudest voices behind the idea that Bitcoin can still reach about $250,000 by the end of 2025—even after the violent drawdown that took BTC into the low-$80,000 range this November.

1.1 From QT to Renewed Liquidity

Hayes’ core argument is not about short-term technicals but about global dollar liquidity:

- He views the recent dump to roughly $80,600 as a liquidity flush tied mainly to the unwinding of ETF basis trades—funds that went long spot ETFs (like IBIT) while shorting CME futures.

- In his view, these trades are mechanical and do not reflect genuine long-term institutional conviction exiting the market.

- More importantly, he argues that U.S. quantitative tightening is approaching its practical limits, while recession fears and political pressures make rate cuts and renewed liquidity in 2026 increasingly likely.

In that world, capital needs a home. When risk-free yields start to fall, investors rotate out of pure cash and Treasuries and back into risk assets—U.S. tech, growth equities, and increasingly Bitcoin as “macro high beta” to global liquidity.

1.2 Why Bitcoin, Not Just Tech Stocks?

Hayes’ thesis is that Bitcoin has become a direct play on monetary debasement:

- Scarce digital asset with a hard cap of 21 million coins.

- Deeply integrated into the regulated financial system via spot ETFs and large custodians.

- Liquid 24/7 global market that reacts quickly to shifts in dollar liquidity.

Recent analyses echo his view that the crash to ~$80k wiped out over $800 billion in BTC market cap, with more than $1.2 trillion erased across digital assets, but also note that structural demand (ETFs, corporate treasuries, long-only funds) has not disappeared.

Hayes therefore paints the $80k–$90k range as a cycle bottom, not a top—and sees a path to ~$250,000 by end-2025, which would be roughly a 170% rally from around $90,000 levels.

For investors, the key is whether you accept the liquidity bottom story. If you believe:

- QT is ending,

- rate cuts and/or fiscal expansion will continue, and

- BTC’s role as a “liquidity sponge” is intact,

then directional BTC exposure—spot, long-term options, or structured products—remains one of the purest macro plays.

2. Crypto-Related Stocks: Miners, Exchanges, and Infrastructure in a New “Risk-On” Phase

The article you provided highlights a broad surge across crypto-related equities—not just the coins themselves. Recent market data supports that picture:

- Bitcoin miners’ stocks have jumped as BTC recovered to the $90,000 area, improving mining margins and balance sheets.

- Exchange-linked names and brokerages exposed to crypto (including trading platforms and market-making infrastructure) are again being pitched as “buy-the-dip” candidates for 2025.

2.1 How Coin Prices Translate into Equity Performance

The relationship is straightforward but powerful:

- Higher BTC/ETH prices (in $)

→ Higher transaction volumes, derivative activity, and spreads

→ Better revenues and earnings for exchanges and brokers. - Higher BTC prices

→ Improved miner profitability and balance-sheet strength

→ More capacity to invest in new rigs, facilities, and energy contracts

→ Stronger equity stories and analyst upgrades. - Stronger ETH and L2 usage

→ More transaction fees and staking revenue for Ethereum-aligned entities

→ Better economics for infra plays (L2 operators, rollup projects, and infrastructure providers).

This is why we often see beta amplification: when BTC rises 50–100%, the strongest miners or exchanges can move several hundred percent, especially if the market is coming off depressed valuations.

(BTC and ETH as the base, with miners, exchanges, and blockchain tech indices showing higher beta.)

2.2 Where Are the Practical Opportunities?

For readers focused on new income streams and practical blockchain use, crypto equities offer:

- Leveraged exposure without self-custody risk

You can access miners, exchanges, and blockchain infrastructure via normal brokerage accounts, without managing keys or wallets. - Cash-flow visibility

Unlike pure tokens, many of these companies report revenues and earnings in $, giving investors a more familiar valuation framework (P/E, EV/EBITDA, etc.). - Strategic positioning

Some exchange/brokerage names are positioning themselves as regulated on-ramps into BTC, ETH, and tokenized real-world assets (RWA). That is where future fee income and institutional flows could concentrate.

For more advanced investors, this is also an opportunity to construct pair trades—for example, long a basket of high-quality miners or infra plays vs. short broader equity indices, or vice versa.

3. Ethereum’s 2025 “Fusaka” Upgrade: Scaling the Real Usage Layer

The third pillar of the bullish story is Ethereum’s accelerating development roadmap.

After the Pectra upgrade earlier in 2025, which improved account abstraction and validator quality-of-life, Ethereum is preparing for its second major upgrade of the year: “Fusaka”, scheduled to activate on December 3, 2025.

3.1 What Is Fusaka?

Fusaka combines two prior internal codenames—Fulu (consensus layer) and Osaka (execution layer)—into a single major hard fork.

Key expected features include:

- PeerDAS (Peer Data Availability Sampling) via EIP-7594, allowing validators to verify rollup data by sampling instead of downloading full datasets.

- Substantial expansion of “blob” capacity for rollups, with over 8–10x improvements projected versus current levels in some analyses, driving down per-transaction costs on L2s.

- Preparation for Verkle trees, which will drastically reduce state size and improve node decentralization, making it easier for individuals to validate the chain.

- Gas and block size optimizations, including EIPs aimed at capping single-transaction size and physical block size to mitigate spam and keep the network healthy.

3.2 Why Fusaka Matters for Real-World Use

For investors and builders focused on practical applications, Fusaka is not just a technical milestone; it is the economic backbone for the next wave of on-chain products:

- DeFi: Lower L2 costs and more predictable data availability make complex strategies (perps, structured products, on-chain treasuries) more feasible for smaller users.

- NFTs and gaming: Cheap, reliable rollups are critical for games that need micro-transactions and in-game asset transfers without $20 gas fees.

- Enterprise & RWA: Corporates and institutions exploring tokenized bonds, invoices, or fund shares need fee stability and security; Fusaka directly addresses that by improving throughput and decentralization.

If Hayes’ liquidity story is the demand-side engine, Fusaka is part of the supply-side infrastructure that determines where that liquidity can be deployed efficiently.

4. Strategy Ideas for Investors Seeking New Crypto Assets & Revenue Streams

Given these three pillars—BTC macro thesis, crypto equities, and Ethereum Fusaka—how can an investor actually position?

4.1 BTC as a Macro Core

For many portfolios, BTC now acts as “digital macro beta”:

- Treat a core BTC allocation in $ terms as a long-duration bet on liquidity, debasement, and the institutionalization of crypto.

- Use simple tools—spot, ETFs, or fully backed ETPs—to minimize operational risk.

- For those able to handle more complexity, overlay option strategies (selling covered calls or structured notes) to generate additional yield on top of directional exposure.

4.2 Satellites: Crypto-Linked Equities

Next, surround that core with select equities that can:

- Amplify upside when BTC and ETH trend higher.

- Provide exposure to fee-based business models (exchanges, brokerages, market makers).

- Play the infrastructure and energy story (miners, data-center operators, chipmakers).

Because these are $-denominated, they can also slot more naturally into traditional equity portfolio mandates and can be benchmarked against broader indices.

4.3 Ethereum & L2 Ecosystem Bets

On the Ethereum side, Fusaka opens a few clearly investable narratives:

- ETH itself, as the asset that secures the network and captures a portion of L2 activity through fees and burns.

- L2 tokens that stand to benefit from cheaper data availability and higher throughput (rollups focused on DeFi, gaming, and enterprise rails).

- Middle-layer infrastructure—bridges, data availability layers, sequencers—whose economics improve when rollup demand scales.

Investors searching for new altcoins with real use may want to focus on:

- L2s with clear fee models and on-chain revenue in $.

- Protocols whose business logic is deeply tied to real user activity (on-chain trading, settlements, payments), not just reflexive tokenomics.

5. Big Picture: Why This Cycle May Look Different

The combination of macro liquidity dynamics, listed equity vehicles, and mature L1/L2 infrastructure means this cycle is not simply a repeat of 2017 or 2021.

- Macro-Driven, Not Just Narrative-Driven

Hayes’ call anchors BTC in the same conversation as rate cuts, balance-sheet policy, and dollar liquidity—not just halving cycles or meme narratives. - Institutional On-Ramps Everywhere

With spot ETFs, regulated exchanges, and crypto-friendly brokers, it is easier than ever for large pools of capital to rotate into BTC, ETH, and related instruments using familiar $ rails. - Real Applications Are Finally Scaling

Ethereum’s Pectra and upcoming Fusaka upgrades are about making DeFi, NFTs, and enterprise tokenization economical at scale. Instead of asking “will anyone use this?”, we are starting to ask “how big can this become if fees and latency collapse?”

For readers specifically hunting new crypto assets and revenue lines, the message is:

- Look for projects and companies that sit at the intersection of these trends:

- Benefit from macro liquidity (BTC, ETH, large-cap L2s).

- Have clear $-denominated business models (exchanges, miners, infra).

- Are technically aligned with Ethereum’s long-term scaling path (Fusaka and beyond).

If Hayes is right and Bitcoin does trend toward $250,000, the winners will not only be BTC holders. The surrounding ecosystem—equities, infrastructure tokens, and application-layer projects—could see even greater percentage gains, especially where real usage, not just speculation, drives demand.