Main Points:

- Qatar National Bank (QNB) has integrated J.P. Morgan’s Kinexys blockchain platform to accelerate USD corporate payments.

- The adoption enables 24/7 settlement, reducing processing times to as little as 2 minutes.

- Kinexys (formerly Onyx) is a permissioned financial-grade blockchain network offering deposit ledgers, tokenization, and programmable payments.

- Recent innovations include the pilot of a USD deposit token (JPMD) on a public L2 blockchain (Base).

- Broader industry trends (tokenized deposits, real-time rails, programmable payments) support adoption momentum across banks worldwide.

- Risks and challenges remain—governance, regulation, security, interoperability—but the move signals a tipping point in institutional finance.

Introduction

In late September 2025, Qatar National Bank (QNB) announced a major upgrade to its corporate payments infrastructure: it has adopted J.P. Morgan’s blockchain platform Kinexys for U.S. dollar payments, enabling near-instant, 24/7 settlement. This marks a concrete example of how “real world” banking is increasingly embracing blockchain rails. In this article, we will (1) summarize the key features of QNB’s deployment and Kinexys’ architecture, (2) examine recent innovations and pilots, (3) contextualize the move within global payments trends, and (4) assess opportunities and risks for institutions and crypto/native entrants alike.

QNB Deploys Kinexys for Faster USD Corporate Payments

QNB’s Upgrade: What Changed

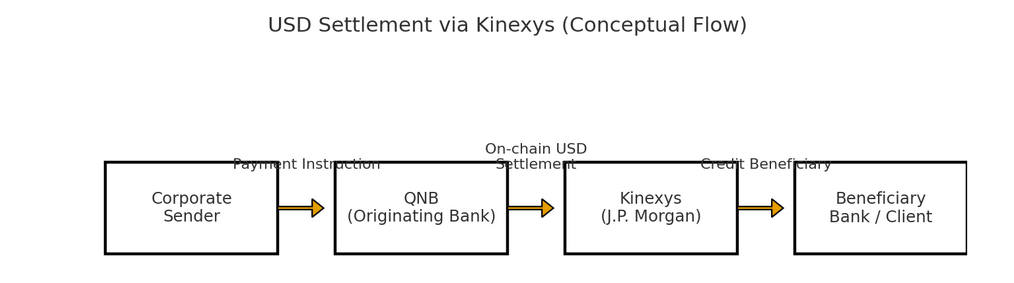

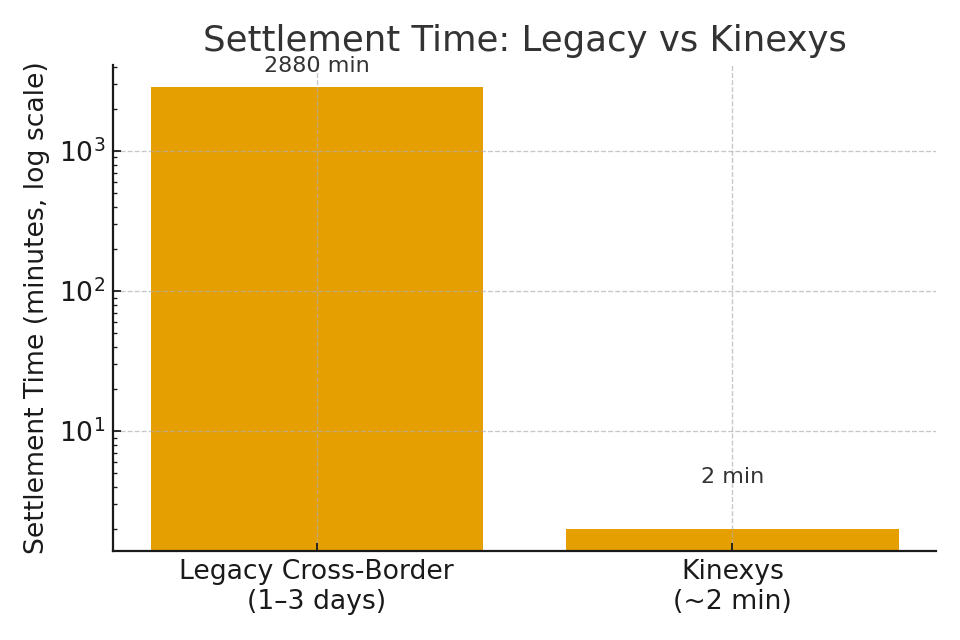

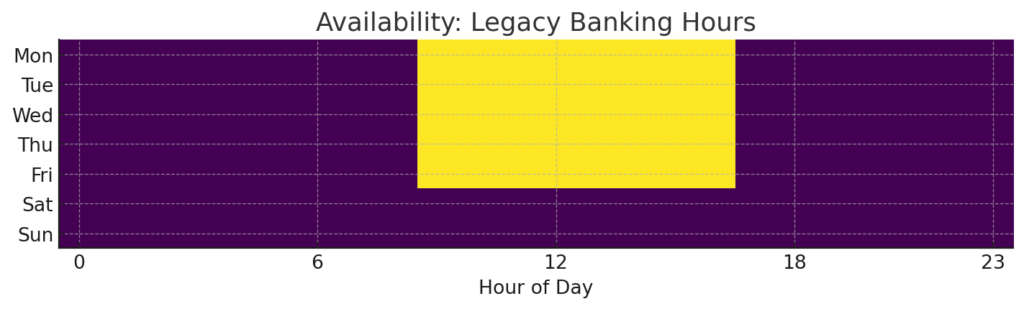

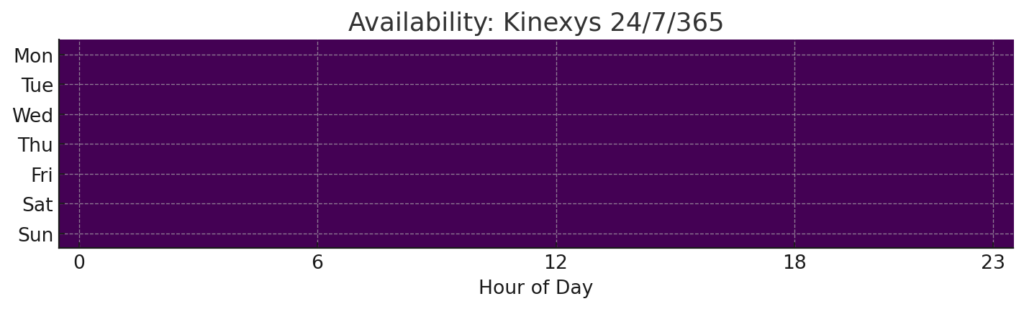

QNB, the largest bank in the Gulf region, has begun processing U.S. dollar–denominated corporate payments through J.P. Morgan’s Kinexys blockchain. Previously, such cross-border or USD payouts had to navigate legacy correspondent banking networks, which often introduce delays (especially across weekends or non-business days). QNB claims it can now guarantee settlement in as little as 2 minutes, and offer 24/7 availability — features that its treasurers call “a dream.”

This is reportedly the first deployment of Kinexys in Qatar. QNB also intends to automate multiple-currency cross-border flows and provide seamless on-demand settlement.

Why It Matters

- Liquidity flexibility: Corporates no longer have to “float” funds across multiple banks or compensate for delays.

- Cost reduction: Fewer manual steps or intermediary swaps can reduce friction and fees.

- Competitive advantage: Regions with slower legacy rails can fall behind if counterparties demand faster settlement.

- Signaling effect: A major regional bank choosing blockchain for real use (beyond pilot) invites peer banks to follow.

Inside Kinexys: Architecture, Capabilities & Recent Innovations

What Is Kinexys?

Kinexys (formerly named “Onyx by J.P. Morgan”) is J.P. Morgan’s institutional blockchain infrastructure suite, built for payments, tokenization, data exchange, and programmable assets. It is a permissioned (i.e. permissioned nodes) network combining a payments rail and ledger for deposit accounts.

Its major components include:

- Kinexys Digital Payments: Enables real-time, 24/7 processing and multi-currency settlement.

- Kinexys Digital Assets / Labs: For tokenization of assets and more programmable financial products.

- Liink: A peer data-sharing / payments information network for authorized institutions and fintechs.

Operationally, Kinexys acts like a bank ledger + payment rail—participants maintain deposit accounts on the ledger, and transactions (i.e. movement of those deposit balances) are settled on-chain.

Transaction Scale & Growth

- To date, Kinexys has processed over $1.5 trillion in notional volume across its services.

- It handles an average of over $2 billion daily in payments and settlement flows.

- Payment transaction volume has been growing roughly 10× year-over-year.

Multi-Currency and FX: GBP Addition

Originally focused on USD and EUR, in 2025 Kinexys expanded to support GBP-denominated deposit accounts in London, enabling 24/7 cross-border payments in the British pound. Clients such as LSEG’s SwapAgent and commodities trader Trafigura are among the early adopters. This move underscores J.P. Morgan’s ambition to cover major currencies on-chain.

On the horizon also is FX capability directly in the chain, making foreign exchange settlement an on-chain function rather than an off-chain reconciliation.

Deposit Tokens on Public Chains: JPMD Pilot

One of the most noteworthy developments is J.P. Morgan’s proof-of-concept for JPMD, a USD-denominated deposit token issued on Base (a public Ethereum Layer 2 blockchain). This represents a hybrid bridging of traditional banking deposits into public blockchain rails (under permissioned issuance). Through JPMD, institutional clients could send and receive on-chain fiat-equivalent tokens, without depending on third-party stablecoins.

Cross-Chain & Tokenized Asset Settlement

Kinexys has also conducted experiments in cross-chain tokenized asset settlement, enabling assets on one chain to settle against payments on another via Oracles etc. This is an important step in achieving composability across different blockchains and financial infrastructures.

Novel Use Cases: Blockchain in Space

In a more experimental direction, J.P. Morgan tested blockchain-based value transfers between satellites, leveraging smart contracts to transact value off-planet. Though not directly relevant for QNB’s USD rails, it signals the ambition to integrate blockchain with IoT and distributed systems at scale.

Why This Move Aligns with Broader Payments Trends in 2025

Shift from Pilots to Production

Business-to-business blockchain adoption is no longer confined to proof-of-concept. At Sibos 2025, analysts noted that the conversation among banks moved from “should we do it?” to “how quickly can we adopt it?” Infrastructure like Kinexys is increasingly viewed not as experimental, but as foundational plumbing.

Tokenized Deposits as a Complement to Stablecoins

While stablecoins have attracted regulatory scrutiny, many central banks and institutions are now exploring tokenized deposits—digital representations of bank deposits on-chain—as safer, regulated alternatives. In the UK, for instance, several major banks are piloting tokenized deposit systems. J.P. Morgan’s JPMD pilot is directly in this line of thinking.

Real-Time, 24/7 Payment Rails

One of the persistent constraints in finance has been the “cutoff times” of financial systems. The ability to send U.S. dollars (or other currencies) at any hour, any day, without human intervention, is a powerful differentiator. For instance, India’s Axis Bank recently launched 24/7 USD payments with J.P. Morgan.

Programmability & Smart Payment Logic

Emerging research shows how digital payment programming (via “streams” and composable smart contract templates) can reduce complexity, improve flexibility, and offer automated conditional transactions. Institutions that embed such programmability can offer richer treasury services, automatic sweeps, contingent disbursements, etc.

Security, Governance & Compliance Are Front and Center

With greater adoption comes greater scrutiny. The risk of cyberattack, regulatory challenge, and governance complexity increases when you expose settlement layers to more participants. According to academic reviews, digital banking platforms must manage phishing, data breaches, third-party integration risks, and compliance with global frameworks in real time.

Convergence of TradFi and DeFi Thought

The divide between traditional finance and decentralized finance is increasingly blurred. Large banks are tokenizing deposits (like JPMD), enabling cross-chain workflows, and embedding “DeFi-like” composability into regulated rails. This convergence is sometimes called “Banking 2.0.”

Opportunities & Challenges for New Entrants

For New Tokens / Cryptos

- Integration opportunities: If banks adopt rails like Kinexys, new tokens (whether utility, payment, or stablecoins) will need to interoperate or position themselves as complementary rather than adversarial.

- On-chain bridge demand: Projects that help bridge permissioned blockchains to public chains (securely and compliantly) may have strategic importance.

- Regulated “on-chain money” demand: The JPMD pilot suggests institutions want on-chain assets with the backing and trust of commercial bank deposits—less volatile than pure stablecoins.

For Blockchain Infrastructure Providers

- Interoperability layer providers (cross-chain, oracles, messaging) will be in demand as banks want tokenized assets that can settle across different chains.

- Compliance & audit tooling: Monitoring, attestation, KYC/AML, reporting—all these will be necessary in real-world banking deployments.

- Security & vaulting services: As more value is stored on-chain, the risks of hacks or compromises grow; secure custody, disaster recovery, and multi-sig schemes are critical.

For Banks and Enterprises

- First-mover advantage: Entities that re-platform now can capture efficiencies and better meet client expectations.

- Migration challenge: Legacy systems, internal inertia, regulatory risk, and counterparties’ unwillingness may slow adoption.

- Governance models: How to govern who participates in the network? What consensus rules? How to upgrade protocols?

QNB + Kinexys: Implications & Outlook

QNB’s deployment of Kinexys for USD corporate payments is more than a “proof of concept” — it’s a bold step into production blockchain rails for real-world banking. The move shortens settlement windows, provides liquidity advantages, and signals to global institutions that Middle East / Gulf banking is moving quickly into the next generation of payment infrastructure.

The global environment supports this trajectory: real-time rails, tokenized deposits, programmable payments, and tighter TradFi–DeFi integration all point toward institutional adoption. However, success hinges on robust governance, security models, regulatory alignment, and interoperability across systems and jurisdictions.

For builders, this moment opens windows: bridging tools, deposit token innovations, compliance modules, and infrastructure for institutions will be increasingly needed. For token projects, alignment (or compatibility) with permissioned rails could become a strategic necessity rather than an optional choice.

In sum: QNB’s leap is emblematic of a new era in which blockchain payment rails stop being speculative and start being operational. The next question: who will build the interfaces, utilities, and adjacent tools that run on these rails—and which currencies will bond to them?