Main Points :

- The United States is increasingly reframing cryptocurrencies not as adversaries to banks, but as part of the same financial infrastructure.

- Public remarks by David Sacks, reported to be involved in White House AI and crypto policy discussions, signal a shift in regulatory mindset rather than a short-term market catalyst.

- The critical issue is not immediate price impact, but who will be allowed to participate in crypto markets and under what regulatory assumptions.

- Ongoing market structure legislation suggests a future where banks, stablecoins, and crypto firms operate under harmonized rules.

- This transition may fundamentally change the quality, risk profile, and institutional makeup of the digital asset market.

Introduction: A Turning Point for U.S. Crypto Policy

For much of the past decade, the relationship between banks and cryptocurrencies in the United States has been framed as a zero-sum conflict. Banks viewed crypto as a regulatory and reputational risk, while crypto firms criticized banking regulations as barriers designed for a pre-digital era.

That framing is now beginning to change.

Recent comments attributed to David Sacks, who has been reported as playing a role in White House-level AI and digital asset policy discussions, reflect a deeper rethinking underway in Washington. Rather than positioning crypto as a parallel or antagonistic system, policymakers are increasingly exploring how digital assets can be formally integrated into the same institutional and regulatory framework as traditional banking.

This is not a headline designed to move Bitcoin prices tomorrow. Instead, it is a signal about the future architecture of financial markets.

1. Banks and Crypto as One Industry, Not Two

The most striking element of the recent policy discourse is the suggestion that banks and crypto firms may eventually be treated as participants in a single “digital asset industry.”

This does not mean that all banks will suddenly become crypto exchanges, nor that decentralized finance will lose its distinct identity. Rather, it implies that the regulatory system may stop treating crypto as an exceptional or temporary anomaly.

Under this emerging view:

- Crypto custody, settlement, and stablecoin issuance could be considered extensions of existing financial services.

- The legal distinction between “bank activity” and “crypto activity” may become more functional than categorical.

- Risk management, capital requirements, and compliance expectations could converge across both sectors.

This shift in framing is critical because regulatory philosophy often determines market outcomes more decisively than individual enforcement actions.

2. Market Structure Rules and the CLARITY Moment

Behind this change in tone lies a broader effort in the U.S. to clarify market structure rules for digital assets.

For years, regulatory ambiguity has dominated the crypto landscape. Agencies disagreed over jurisdiction, market participants operated under enforcement-driven guidance, and institutional players largely stayed on the sidelines.

That environment is now giving way to structured debate over questions such as:

- Which digital assets are securities, commodities, or payment instruments?

- How should stablecoins be regulated when they function simultaneously as money, settlement tools, and financial infrastructure?

- What compliance standards should apply when banks interact directly with blockchain-based systems?

Legislative initiatives often described collectively as “market structure reform” aim to answer these questions. While no single bill resolves everything, the direction is clear: integration, not exclusion.

3. Not a Price Catalyst, but a Participant Catalyst

For traders focused on short-term price movements, this policy shift may seem underwhelming. There is no immediate supply shock, no halving event, and no sudden surge in retail demand.

Its importance lies elsewhere.

If banks and large financial institutions are given clearer pathways to participate in digital asset markets, the composition of market participants will change. That, in turn, affects liquidity quality, volatility patterns, and project selection.

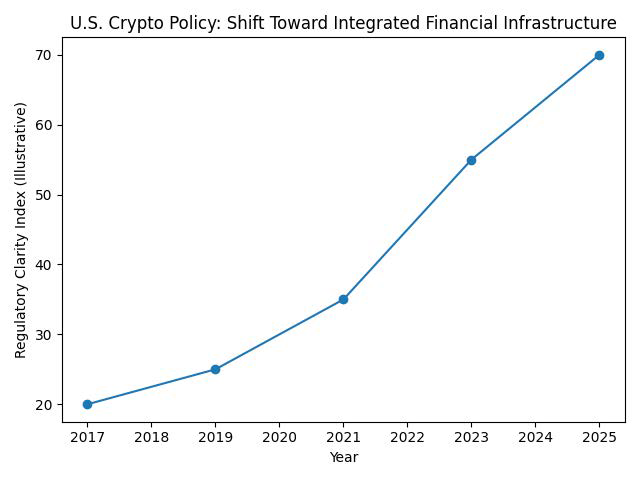

Below is an illustrative chart showing how U.S. crypto policy has gradually shifted from enforcement-heavy ambiguity toward regulatory integration.

[U.S. Crypto Policy Shift Timeline]

This transition suggests that future growth may be driven less by speculative cycles and more by institutional adoption and infrastructure build-out.

4. Why This Shift Is Happening Now

The timing of this policy evolution is not accidental.

Several forces are converging:

- Stablecoin Reality

Dollar-pegged stablecoins now settle trillions of dollars annually on public blockchains, functioning as de facto payment rails. Ignoring them is no longer practical. - Global Competition

Jurisdictions such as the EU, Singapore, and Japan have moved ahead with clear crypto frameworks. The U.S. risks losing financial leadership if it remains stuck in ambiguity. - Institutional Demand

Asset managers, custodians, and payment providers increasingly demand regulatory certainty before deploying capital and infrastructure. - Technological Maturity

Blockchain systems are no longer experimental novelties. They are production-grade networks supporting real economic activity.

Together, these factors push policymakers from a defensive stance toward a design-oriented approach.

5. Implications for Banks

If crypto becomes part of the same financial industry as banking, banks may find new opportunities rather than new threats.

Potential areas of involvement include:

- Digital Asset Custody: Secure storage for crypto assets under regulated frameworks.

- Stablecoin Issuance and Settlement: Bank-backed or bank-integrated dollar tokens.

- Blockchain-Based Payments: Faster cross-border settlement using public or permissioned ledgers.

- Tokenized Deposits and Securities: Representing traditional financial instruments on-chain.

Banks that adapt early may gain a competitive advantage, while those that resist may find themselves disintermediated.

6. Implications for Crypto Firms and Builders

For crypto-native companies, integration cuts both ways.

On the positive side:

- Regulatory clarity lowers legal risk.

- Access to banking services improves.

- Institutional clients become reachable.

On the challenging side:

- Compliance costs increase.

- “Move fast and break things” becomes less viable.

- Governance, transparency, and risk controls become mandatory rather than optional.

The projects most likely to benefit are those already designed with regulatory compatibility in mind.

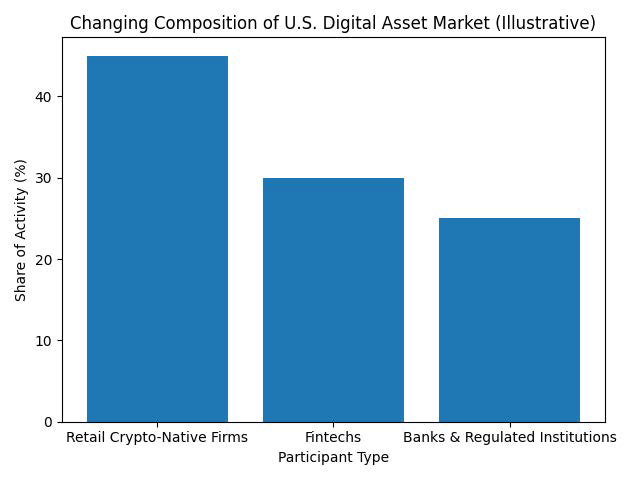

7. A Changing Market Composition

As participation broadens, the makeup of the digital asset market itself may evolve.

The following illustrative chart shows a possible shift in market activity share as regulated institutions enter more deeply.

[Changing Composition of Digital Asset Market]

This does not imply the disappearance of retail or decentralized actors, but it does suggest a more balanced and institutionally anchored ecosystem.

8. What Investors Should Watch

Rather than watching price charts alone, investors interested in long-term opportunity should monitor:

- Regulatory milestones in U.S. market structure legislation

- Bank announcements related to custody, stablecoins, or tokenization

- Growth in compliant infrastructure providers

- Shifts in liquidity sources from offshore to onshore venues

These indicators reveal structural change before it becomes visible in asset prices.

Conclusion: From Exception to Infrastructure

The core message of the recent U.S. policy discourse is subtle but profound.

Cryptocurrencies are no longer being treated as an external challenge to the banking system. They are increasingly viewed as a component of the same financial infrastructure—one that requires updated rules, shared standards, and institutional participation.

For builders, this means designing for compliance as well as innovation.

For investors, it means focusing less on hype cycles and more on structural adoption.

For the market as a whole, it signals a transition from adolescence to maturity.

The real impact of this shift will not be measured in tomorrow’s price candles, but in who is allowed to build, operate, and scale the financial systems of the next decade.