Main Points:

- FHFA Directive: On June 25, 2025, the Federal Housing Finance Agency (FHFA) ordered Fannie Mae and Freddie Mac to prepare proposals to include unconverted cryptocurrency holdings in single-family mortgage risk assessments.

- Eligibility Criteria: Only crypto held on U.S.-regulated centralized exchanges, compliant with all relevant laws, may be considered.

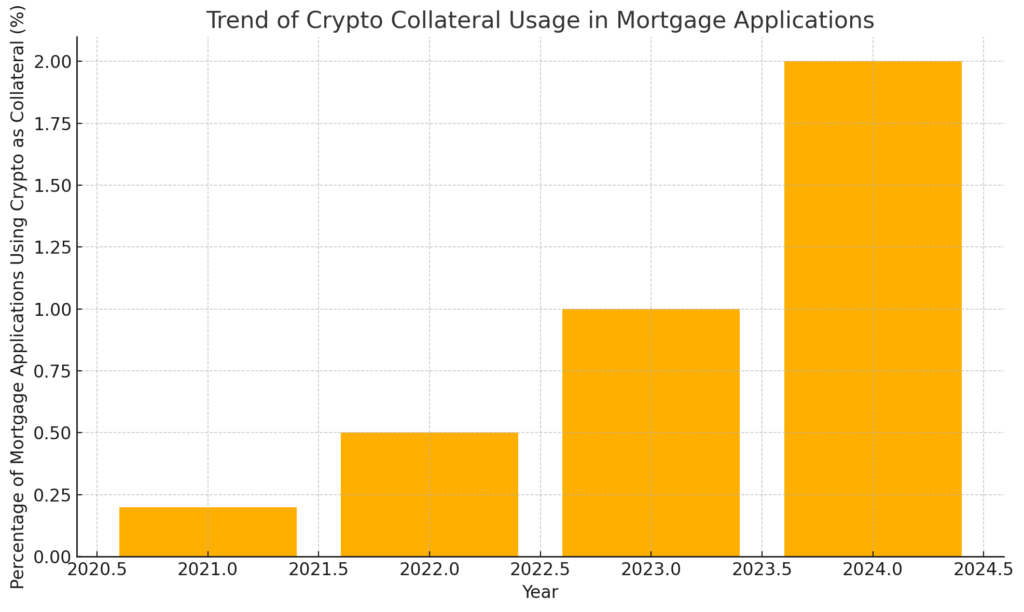

- Current Adoption: Crypto-backed mortgages remain rare—roughly 1 % of homebuyers used crypto proceeds in 2023–2024.

- Industry Moves: JPMorgan plans to accept Bitcoin ETF shares as collateral; Circle’s USDC stablecoin will be eligible as futures collateral via Coinbase Derivatives and Nodal Clear next year.

- Market Impact: The shift could broaden homeownership access, encourage banks to diversify asset recognition, and accelerate crypto’s mainstream financial integration.

Background

Since its creation to stabilize the housing market after the 2008 financial crisis, FHFA has overseen Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation). These government-sponsored enterprises purchase home loans from lenders, freeing up liquidity for further mortgage originations and underpinning the U.S. housing market’s stability. Despite widespread volatility—Bitcoin dropped 16 % earlier this year before rebounding—FHFA’s announcement marks the first time digital assets may be acknowledged directly in mortgage underwriting without prior conversion to U.S. dollars.

Details of the FHFA Directive

FHFA Director William J. Pulte issued a letter instructing both GSEs to:

- Draft a Proposal: Outline how crypto can be treated as a reserve asset in single-family mortgage risk assessments without USD conversion.

- Define Eligible Assets: Limit consideration to assets stored on U.S.-regulated centralized exchanges, verifiable under applicable laws.

- Assess Risk Mitigants: Include volatility buffers and reserve requirements to manage digital asset risks.

- Board Approval: Obtain each enterprise’s board sign-off before submission to FHFA for review .

Pulte emphasized the directive followed “significant studying” and aligns with President Trump’s stated ambition to make the U.S. the “crypto capital of the world”.

Industry Implications

- Broadening Credit: By recognizing crypto holdings directly, lenders can more accurately capture a borrower’s full financial profile, potentially approving mortgages for otherwise creditworthy applicants whose wealth resides partially in digital assets.

- Volatility Management: Risk frameworks must address crypto’s price swings. Proposed buffers could discount on-chain balances by a conservative percentage to mitigate downside risk.

- Regulatory Coordination: The approach may set a precedent for other regulators—banking, securities, and consumer finance—to update guidelines around unconverted crypto assets.

- Tech Integration: Mortgage platforms and loan origination systems will need API integrations with centralized exchanges for real-time balance and compliance verification.

Case Studies and Use Cases

- High-Net-Worth Borrowers

Wealthy individuals often hold significant crypto portfolios. Under the new regime, they could leverage Bitcoin or Ethereum holdings as collateral without liquidating positions, preserving upside exposure while accessing home equity. - Stablecoin Collateral for Futures

Circle’s USDC, valued at $1 per token, will become accepted collateral for derivatives trading on Coinbase Derivatives and Nodal Clear in 2026, illustrating institutional acceptance of stablecoins as reliable reserves. - Bank-Sponsored Crypto Loans

JPMorgan has indicated plans to permit Bitcoin ETF shares (e.g., BTC ETF) as collateral in its bespoke lending products for select clients, foreshadowing broader bank adoption.

Recent Developments

- FHFA Public Feedback

FHFA opened a public comment period through August 2025, soliciting input on proposed risk parameters and asset eligibility. - Pilot Programs

Smaller depository institutions have begun pilot programs allowing crypto pledges against home equity lines of credit, using 50 % collateral haircuts to account for volatility. - Technology Partnerships

Fintechs such as Figure Technologies and Anchorage Digital are collaborating with lenders to provide custody, asset verification, and real-time valuation oracles.

Graphical Illustration

Below is a chart showing the trend of mortgage applications using cryptocurrency as collateral, illustrating growing—but still niche—adoption:

Conclusion

FHFA’s directive represents a landmark in financial innovation and regulatory evolution, potentially transforming mortgage underwriting by formally integrating cryptocurrency holdings into borrower assessments. By mandating board-approved proposals and focusing on assets held at U.S.-regulated exchanges, FHFA aims to balance innovation with risk management. As other major financial institutions like JPMorgan and Circle follow suit, expect broader frameworks for digital asset collateral across banking and capital markets. For crypto investors, this shift unlocks new pathways to liquidity—turning dormant digital portfolios into tangible purchasing power without forfeiting market exposure—while signaling crypto’s continued march toward mainstream legitimacy.