Main Points:

- Bitcoin treasury companies currently derive value mainly from accumulating BTC rather than operational businesses.

- Premiums to NAV are justified only if companies build scalable, revenue-generating services beyond “bitcoin yield.”

- Leverage via convertible debt creates asymmetric risk: full downside but capped upside.

- Without “operational alpha,” stock premiums are likely to erode over time.

- Emerging players like Metaplanet and institutional tailwinds (Crypto Week) highlight both potential and pitfalls.

- Sustainable models include broker-leverage, liquidity provision, collateralized lending, and structured products.

The Rise of Bitcoin Treasury Companies

Since 2020, a growing number of publicly listed firms have adopted Bitcoin treasury strategies, raising capital through equity or convertible debt to purchase and hold BTC on their balance sheets. High-profile names like MicroStrategy (MSTR.O) – now holding over 580,000 BTC (2.8% of the total supply, valued at approximately $60 billion) – have blazed the trail. This trend accelerated in mid-2025: as of July, some 250 companies hold BTC, up from 141 at the start of the year. Blockware Intelligence forecasts at least 36 more firms will join by year-end, a 25% increase.

The narrative is compelling: corporates signaling belief in Bitcoin as a global reserve asset, institutional-grade exposure, and the potential for share price appreciation at a premium to NAV (Net Asset Value). Yet, as crypto research firm K33’s Torbjørn Bull Jenssen observes, simply chasing “bitcoin yield”—the growth in BTC per share—is not a sustainable business plan (“Operational alpha” is missing).

Why Premiums Alone Don’t Justify Investment

The Bitcoin Yield Fallacy

Many analysts point to a metric dubbed “Bitcoin yield”—the rate at which a company’s BTC holdings per share increase—as justification for stock premiums. Conceptually, if a firm issues shares at NAV+X%, buys BTC, and holds it, the yield per share rises. However, rational investors seeking maximum BTC exposure could simply buy BTC directly on the market, avoiding fees and dilution.

In practice, treasury stocks trade at an aggregate 73% premium to underlying BTC value. But this premium fails to account for the capital efficiency and operational costs of corporate vehicles. Without value-added services, the arbitrage of direct BTC purchase versus premium-laden shares persists.

The Leverage Conundrum

Convertible Debt and Asymmetric Risk

To accelerate accumulation, many treasury firms tap convertible bonds, issuing debt that converts to equity at a discount if BTC rallies. This creates a leveraged long on BTC: firms benefit from price increases up to a cap (conversion price), while bearing full downside if BTC falls.

- Downside risk: If BTC price drops, companies may liquidate BTC to service debt.

- Upside limit: Creditors convert at a discount and sell at market, capturing gains that would otherwise accrue to shareholders.

This structure explains why debt investors eagerly finance BTC buys—it caps their risk and locks in a yield-like payoff. Yet, shareholders effectively underwrite creditors’ gains, compressing their upside.

Recent Market Momentum and Regulatory Tailwinds

Crypto Week and Institutional Adoption

In July 2025, Bitcoin surged past $122,000, marking a 10% weekly gain as Washington prepared for “Crypto Week”—deliberations on the GENIUS Act, Clarity Act, and Anti-CBDC Surveillance Act. These bills aim to clarify stablecoin rules and delineate regulatory authority, boosting institutional confidence. MicroStrategy and fellow treasury stocks rallied accordingly.

Moreover, Japanese hospitality firm Metaplanet pivoted to a BTC treasury strategy, targeting 210,000 BTC (≈$23 billion) by 2027 and planning to acquire digital financial service businesses leveraged by its holdings. Their avoidance of convertible debt in favor of preferred shares hints at a desire for a more balanced capital structure, though skeptics question the lack of an immediate operational roadmap.

Sustainable Business Models Beyond “Bitcoin Yield”

To justify and sustain premiums, treasury companies must develop scalable, fee-generating services anchored in BTC. Viable pathways include:

- Broker-Leverage Services

Offering clients leveraged BTC exposure via margin or structured notes, generating fees on both sides of the trade. - Liquidity Provision

Acting as market makers on crypto exchanges, capturing bid-ask spreads while using on-balance-sheet BTC as inventory. - Collateralized Lending

Lending BTC or using BTC as collateral to underwrite loans, earning interest margin (e.g., BTC-backed corporate debt). - Structured Products

Designing derivatives or yield-bearing products (e.g., BTC-linked notes), charging structuring and management fees.

These lines of business rely on an active balance sheet—not merely holding BTC, but deploying it in financial transactions. They are scalable, capable of generating consistent revenue streams and justifying ongoing stock premiums.

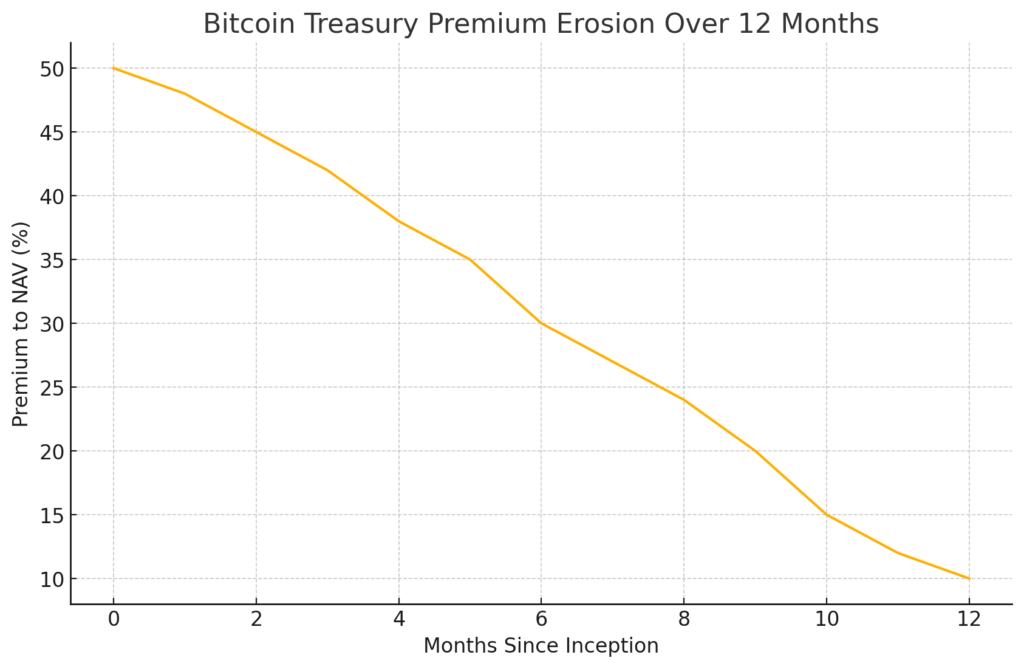

The Risk of Premium Erosion

Our hypothetical chart illustrates how premiums can decay over a 12-month period lacking operational alpha:

See “Bitcoin Treasury Premium Erosion Over 12 Months” above.

Absent business execution, market arbitrageurs will exploit the premium, driving it toward NAV. Once premiums compress, share prices could collapse, triggering margin calls or debt covenants—and a possible fire sale of BTC.

Conclusion

While Bitcoin treasury companies have captured headlines—and capital—through aggressive BTC accumulation, “buy and hold” strategies alone do not constitute a sustainable business plan. Without operational alpha—value-added services such as brokerage, liquidity provision, lending, or structured products—stock premiums are vulnerable to erosion. As regulatory clarity (e.g., Crypto Week legislation) and institutional adoption boost Bitcoin’s narrative, only companies that deploy their BTC in scalable, fee-generating activities will justify premium valuations and emerge as the sector’s long-term winners.