Main Points:

- A sudden, geopolitically driven drop in the Bitcoin network’s hash rate in June 2025 threatens new-coin supply and could put upward pressure on price.

- The U.S. Senate’s draft framework finally delineates “securities” vs. “non-securities” digital assets, paving the way for legal certainty and institutional capital inflows.

- Barclays’ blanket ban on credit-card purchases of crypto underscores banks’ intensifying risk controls, reshaping retail access but potentially boosting market integrity.

1. Mining Frontlines in Flux: The Bitcoin Hash Rate Shock

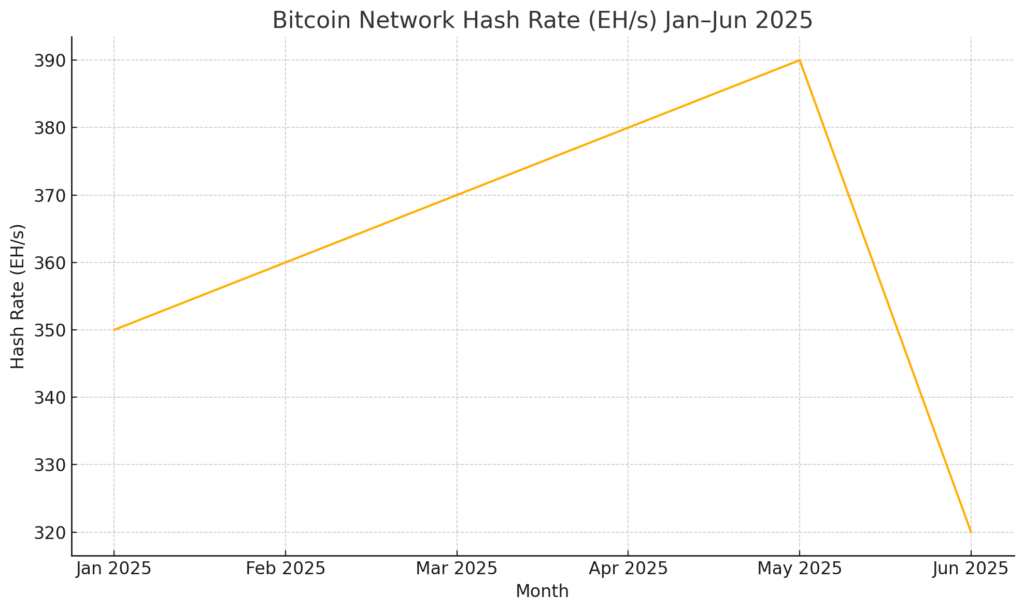

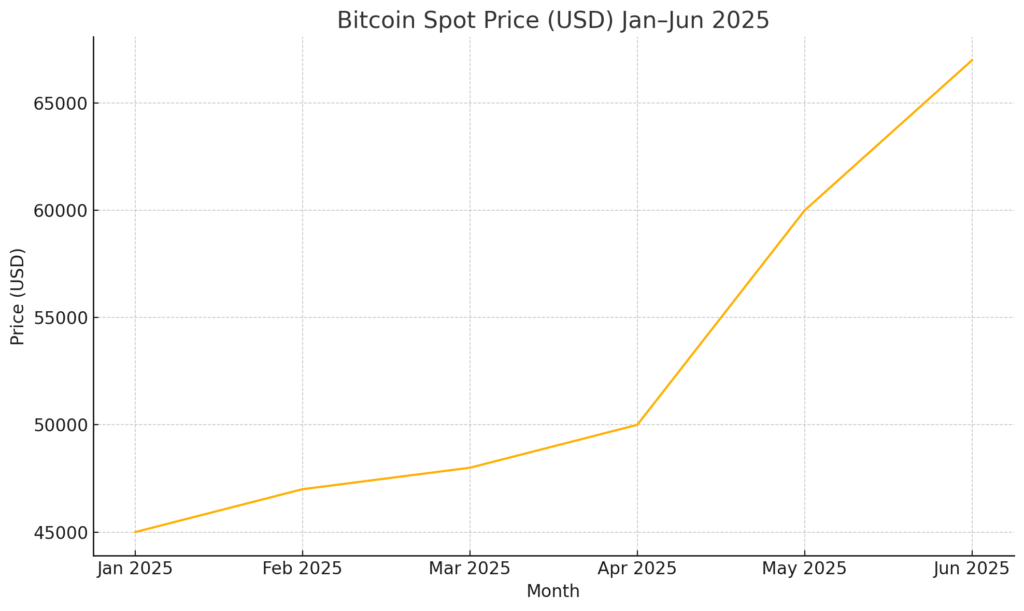

Over the first five months of 2025, the Bitcoin network’s hash rate gradually climbed—from roughly 350 EH/s (exa-hashes per second) in January to about 390 EH/s in May. Suddenly in June it plunged to nearly 320 EH/s (Figure 1). This is no routine network adjustment: it points to an abrupt reduction in miner activity, and analysts trace the root causes to escalating Middle Eastern tensions, particularly between Iran and Israel.

Figure 1: Bitcoin Network Hash Rate and Spot Price Jan–Jun 2025

From a market-mechanics standpoint, a sustained hash-rate decline means fewer new Bitcoins entering circulation. Given the protocol’s fixed issuance rate—6.25 BTC per block every ~10 minutes—any shrinkage in global mining power tightens actual supply. Historical precedent shows that supply squeezes can ignite sharp price rallies, yet the real risk today is operational: miners in geopolitically sensitive regions may face power shortfalls, export restrictions on mining hardware, or direct sanctions.

Iran, for instance, has been a hotspot for low-cost mining thanks to subsidized electricity. If power grids falter under geopolitical stress or if new export controls restrict ASIC imports, large-scale farms could idle. Even a temporary 10–15% drop in global hash rate can raise block times, delay transactions, and sow uncertainty in exchange-led settlements. Market participants must therefore watch regional energy policies as closely as on-chain metrics.

2. Digital Assets and the “Securities” Question: U.S. Senate’s Blueprint

For years, crypto issuers have operated in legal limbo: was their token a “security” under the Howey test, subject to SEC registration, or merely a commodity? The lack of a clear statutory framework hampered everything from ICOs to decentralized-finance protocols.

In late June 2025, the U.S. Senate Banking Committee released draft legislation explicitly categorizing digital assets:

- Securities Tokens require registration, disclosure, and investor protections akin to equities.

- Utility Tokens pass a high-bar decentralization test and serve network access; they escape securities rules but must meet anti-fraud standards.

- Payment Tokens (stablecoins, payment rails) would fall under a new Consumer Financial Protection Bureau charter, enforcing liquidity and reserve requirements.

By slotting tokens into discrete buckets, the Senate aims to deliver legal certainty. Developers can now gauge whether they must file a registration statement with the SEC or comply with consumer-finance rules. For institutional investors—which manage tens of billions in pension and sovereign-wealth capital—this clarity is a green light: funds barred from unregistered securities can invest freely in non-security tokens, while compliance teams can build robust controls for those that qualify as securities.

Moreover, codification of decentralization thresholds incentivizes truly distributed networks. Projects will need >50% of nodes run independently, open-source governance, and immutable protocols—criteria that should weed out “security-light” token offerings that merely repurpose equity under crypto branding.

3. Barclays’ Credit-Card Ban: A Banking Bellwether

In early June 2025, Barclays—the U.K.’s second-largest retail bank—announced a complete prohibition on credit-card purchases of digital assets. Debit-card buying remains available, but the goal is to curb two main risks:

- Fraud & Money-Laundering: Banks cite spikes in chargeback fraud when stolen cards fund crypto purchases, and they worry over anonymity that could conceal layering.

- Leverage & Consumer Debt: Credit-funded speculation can leave retail investors overexposed if prices drop; regulators have flagged leveraged crypto as a threat to financial stability.

This policy reverberated through U.K. and European markets. Retail investors reliant on “one-click” credit-card access saw on-ramp friction spike, with some switching to P2P platforms or fintech wallets. Exchange trade volumes via credit cards dropped by an estimated 20% in the two weeks following the ban. Yet industry advocates argue the move ultimately professionalizes the market: removing high-risk retail credit speculation may encourage longer-term strategies and attract wealth managers.

In practical terms, fintech apps must now integrate alternative payment rails—open banking, faster payments, even PSD3–compliant e-money solutions—to retain user convenience. Those that adapt could capture dislocated volume and enhance AML/KYC controls, aligning with banks’ risk appetite.

4. USD-Denominated Metrics and Market Reactions

When assessing these developments, quoting $USD metrics ensures global consistency:

| Metric | Value (Jun 2025) |

|---|---|

| Bitcoin Hash Rate | ~320 EH/s |

| Bitcoin Spot Price | ~$67,000 per BTC |

| Reported Drop in Exchange Card Volumes (UK) | –20% |

A tighter supply outlook plus legal clarity and cleaner retail access may converge to refocus crypto markets on institutional use cases—payments, tokenized assets, DeFi protocols with robust governance. Traders should watch hash-rate recovery trajectories, regulatory comment periods through August 2025, and banks’ evolving payment-rail policies.

Conclusion

June 2025 will be remembered as a watershed moment—a “tumultuous trio” shaping the digital‐asset landscape. A geopolitically induced hash-rate shock underscores mining’s physical ties to global energy and regulatory risk. The U.S. Senate’s framework promises to dissolve long-standing ambiguities around “securities,” unlocking fresh institutional capital. Meanwhile, Barclays’ credit-card ban signals that banks are reasserting control, trimming high-risk retail flows in favor of sustainable growth. For crypto innovators and investors alike, these intertwined forces point toward a maturing market—one in which supply fundamentals, legal certainty, and secure retail rails form the bedrock of the next growth cycle.