Main Points:

- Corporate “bitcoin-treasury” strategies—i.e., publicly traded firms holding large amounts of Bitcoin on their balance sheets—are now under renewed pressure amid recent crypto market pull-backs.

- The largest player, Strategy (formerly MicroStrategy), despite a sharp drop in its share price, is still viewed by some analysts as a candidate for inclusion in the S&P 500 index.

- Smaller digital-asset-treasury (DAT) companies are facing much tougher conditions: their market net asset value multiples (mNAVs) have fallen below key thresholds, making fresh capital raises and bitcoin accumulation difficult.

- The business model of DATs—issue equity or debt to buy crypto, rely on crypto price appreciation, and often dilute existing shareholders—carries inherent structural risks, especially in down-markets.

- Recent research suggests that while corporate bitcoin accumulation has been a driver of bitcoin demand and price, the leverage and opacity of the model may turn into a source of systemic risk if conditions reverse.

- For crypto-assets investors—particularly those seeking new asset opportunities, income sources, or practical blockchain applications—the evolving DAT landscape presents both potential and risk. The model’s durability in adverse market conditions is questionable.

1. The Rise of Corporate Bitcoin Treasuries

In recent years, a new paradigm emerged in the crypto-finance world: publicly listed firms converting part of their corporate treasuries into bitcoin. The leading example of this playbook is Strategy, which under the leadership of Michael Saylor shifted from primarily software/analytics into a bitcoin-treasury business. The model is relatively simple: raise capital (via equity or debt), deploy it to accumulate bitcoin, and hope for price appreciation and capital market upside. As one guide notes, “the crypto treasury strategy generally follows a standard sequence of events: raising capital … then acquiring crypto.”

The attraction is clear: bitcoin’s strong historical gains, scarcity (21 million coins), and increasing institutional recognition provide an appealing treasury hedge or value-store alternative. Meanwhile, such companies offer equity investors indirect exposure to bitcoin via regulated stock markets rather than direct token custody.

For new crypto-asset hunters and those seeking next-generation income or blockchain applications, this trend appeared to extend the digital-asset opportunity set beyond tokens into corporates.

2. Recent Pull-back and the Pressure on the Model

However, the model is now under renewed scrutiny. With crypto markets entering adjustment phases and macro conditions tightening, several stress points have emerged.

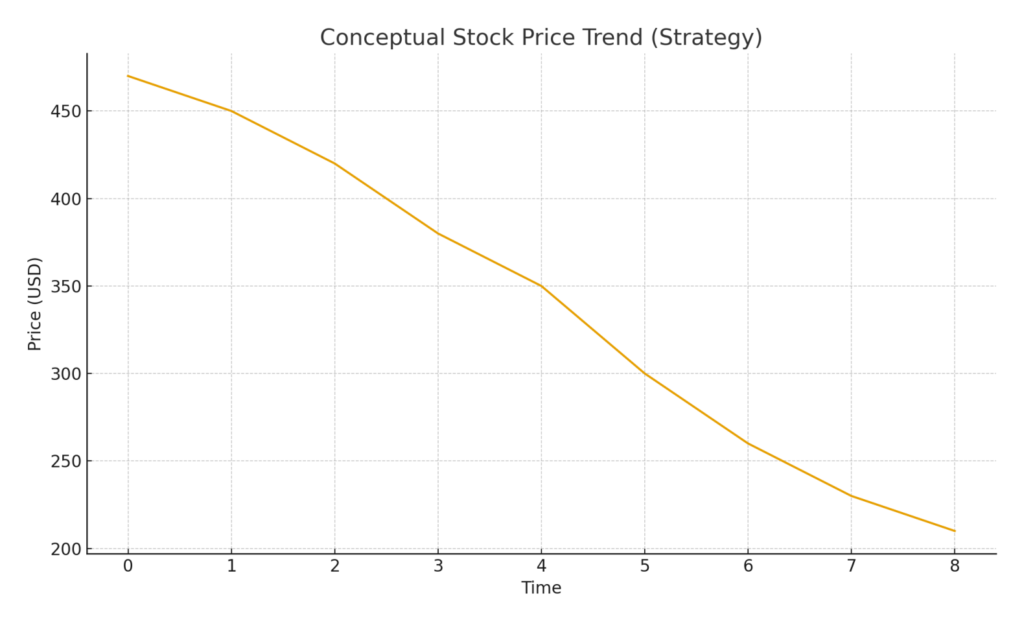

According to a recent report, the share price of Strategy fell from a peak around $474 down to roughly $207. (The referenced source indicates sizeable draw-down) — yet analysts still view it as a potential December inclusion in the S&P 500 index.

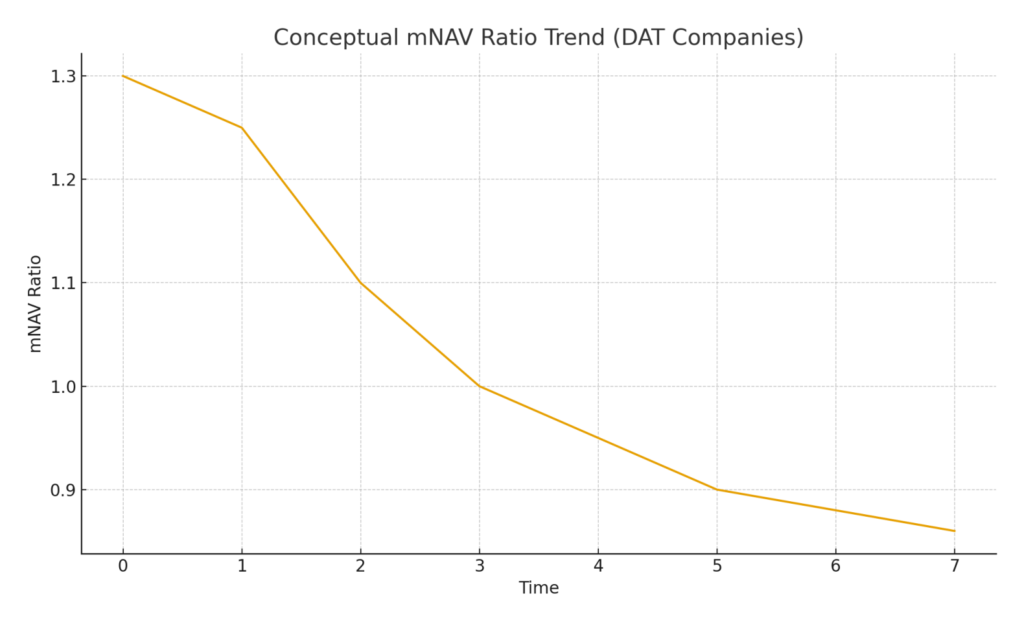

Moreover, a broader data point: a recent article found that amongst the top 20 “pure-play” bitcoin-treasury companies, many are now trading at an mNAV (market cap divided by crypto holdings value) of below 1.0×, meaning the market values less than the value of their crypto on the balance sheet.

What this means is: when the underlying asset (bitcoin) is volatile or stagnant, the equity wrapper suffers. The corporate must still finance operations, service any debt, and may be forced into dilution or even liquidation if things go bad. One research piece warns that as their holdings grow, treasury companies could become a “systemic risk” for bitcoin if forced to sell.

The original article you cited notes that the major risk right now is not forced liquidation of the largest player but NAV compression – the high valuation premium at which shares were issued is now under pressure, and investors who bought earlier at elevated valuations are bearing the brunt.

3. Smaller DATs: The Weak Link

While Strategy may (at least for now) retain some resilience, the smaller DAT players are in a more precarious position. Their mNAVs have breached the critical threshold of 1×, meaning they cannot raise fresh capital easily to buy more bitcoin. The article highlights that many such firms saw their market NAV (mNAV) fall below that level, restricting additional bitcoin purchasing via new equity issuance.

For example, the concept of mNAV ratio is defined as the firm’s market value divided by the value of digital assets held (in this case bitcoin). If mNAV > 1, the company can issue new equity at a premium and use the proceeds to buy more assets; if mNAV < 1, the model breaks down because any issuance dilutes asset per-share value.

These firms also often suffer from negative operating cash flows, and rely heavily on capital markets rather than internal cash-flow generation. The risk of dilution, leverage, and forced sales looms.

Therefore, for new opportunities in the crypto-asset space, the smaller DATs may present higher upside (if they recover) but also higher risk (structural model risk).

4. Implications for Bitcoin, Token Investors and Blockchain Practitioners

Impact on Bitcoin supply and demand

One dynamic to highlight: the corporate accumulation of bitcoin has materially altered the supply-side dynamics of the bitcoin market. A research piece shows that the number of corporations buying bitcoin on average reached 26 per day in June 2025.

As more supply is locked up in corporate treasuries, fewer coins are available for other users, which can provide upward pressure on the price, especially in a tight market. However, if the sentiment turns and corporates become net sellers or stop buying, the same mechanism could amplify downside.

For token investors, this means that corporate behaviours are increasingly a factor in crypto asset flows, not just retail or institutional fund behaviour.

Indirect exposure: equity wrappers vs direct tokens

Investors tempted by DAT firms must recognize the difference between owning tokens directly (e.g., buying bitcoin or altcoins) versus owning an equity wrapper whose value depends on token holdings plus corporate financing decisions, dilution risk, debt, and governance. A recent Business Insider report shows that retail investors have already lost approximately $17 billion by buying into DAT stocks at inflated premiums over NAV.

Thus, if your focus is on discovering the next-gen crypto asset or building a blockchain application, exposure via DAT stocks is a distinct vector: better regulation, tradability, but added corporate risk and often no direct exposure to stake yields, token utility, or DeFi flows.

For blockchain application developers and practitioners

If you are building or operating a blockchain product (wallet, DeFi, token issuance, etc.), the rise (and possible contraction) of corporate treasury strategies signals a few things:

- The narrative of “bitcoin as corporate treasury reserve asset” may bleed over into new protocols or projects that offer treasury-play opportunities (e.g., alt-coin treasuries, staking treasuries). Such models may attract investor interest but also expose you to corporate-finance risk rather than pure blockchain-utility risk (see for example ETH-treasury companies which stake ETH for yield).

- The risk of correlation between token price and corporate treasury stocks is rising: one academic study found the average beta of firms holding bitcoin to be ~0.62, and for some above 1.0.

- If you are designing infrastructure (wallets, token issuance platforms, etc.), the prospect of corporate treasuries could add demand for custody, transparency, and compliance features. Conversely, a rollback or credibility hit in the treasury model could reduce demand for such services or shift emphasis back to utility-token models.

5. What to Watch Going Forward

S&P 500 inclusion and index effects

One key question: will Strategy (and by extension similar firms) be included in the S&P 500 index? The original article reports that one research house (10X Research) estimated a ~70% chance of inclusion by end of year. The implication of inclusion would be broad passive index fund buying, which could support the share price irrespective of token price movement. However, the inclusion depends on free-float market cap, profitability, corporate governance, and other index criteria.

Execution risk: financing, dilution, and NAV leverage

The durability of the model depends on the companies’ ability to keep acquiring assets without eroding per-share value. Key metrics to monitor include: mNAV multiples, dilution rate (shares issued), debt burdens, and treasury policy (do they sell assets under pressure?). If mNAV falls persistently below 1×, the model’s dynamic breaks and investor confidence may collapse.

Macro environment and crypto market regime

Because the DAT model leverages bitcoin price appreciation and cheap capital, a shift in macro regime (rising interest rates, dollar strength, risk-off sentiment) could lead to a sharp reversal. As one research note argues, the very leverage that amplifies upside can amplify downside and turn DATs into systemic risk.

Token and blockchain opportunities

For those seeking new crypto assets or practical blockchain applications, the contraction of DAT models could open windows of opportunity. If the treasury-play hype fades, capital may shift toward tokens backed by real utility, staking yield, DeFi revenue, and blockchain infrastructure. Projects that emphasize cash-flow generation, tokenomics rooted in usage (not just accumulation), and transparent governance may gain favor.

Conclusion

The corporate bitcoin treasury strategy carved out by Strategy and its peers introduced a novel bridge between traditional equity markets and the crypto universe. Initially, the model delivered outsized returns and captured investor imaginations. But as we see in the current market correction, structural risks—dilution, financing dependencies, leverage, and valuation multiples—are coming to the forefront.

For investors hunting new crypto assets, the message is nuance. While DAT firms may still have upside, they are no longer simply “bitcoin on offer” — they are corporates with token-wrapper risk baked in. Meanwhile, for blockchain practitioners and token issuers, the evolving landscape signals a shift: the treasury-accumulation thesis may be fatigued, and utility, yield, governance and real-world adoption may again take center stage.

If you’re looking for the next revenue-source or novel blockchain use-case, now may be the time to look past treasury-plays and focus on tokens or platforms where usage, staking yield or application-layer network effects drive value—not just accumulation of a scarce asset.