Main Points :

- The CLARITY Act is poised to redefine U.S. crypto regulation, potentially becoming law in 2026.

- The biggest controversy centers on banning passive yield on stablecoins like USDC and USDT.

- Clear classification between U.S. Securities and Exchange Commission and Commodity Futures Trading Commission oversight could unlock institutional investment.

- DeFi will be regulated based on custody and control of assets, not just technology.

- The bill could trigger a global shift in capital flows, affecting yields, exchanges, and user strategies worldwide.

1. Why the CLARITY Act Matters Now

The cryptocurrency industry is entering what can only be described as a “rule finalization phase.” After years of ambiguity, regulatory fragmentation, and enforcement-driven policy, the United States is now attempting to establish a comprehensive legal framework through the CLARITY Act.

Originally passed in the House in July 2025 with strong bipartisan support, the bill has re-emerged in April 2026 as a critical legislative priority. The Senate’s renewed discussions signal urgency: if progress is not made by May, the bill risks falling off the 2026 legislative calendar.

This is not merely a domestic issue. The U.S. remains the largest capital market in the world, and its regulatory stance directly influences global crypto liquidity, exchange operations, and institutional participation.

Recent commentary from policymakers highlights a growing concern: blockchain developers and crypto firms are increasingly relocating to jurisdictions such as Singapore and Abu Dhabi due to regulatory uncertainty. The CLARITY Act is, therefore, not just about compliance—it is about retaining innovation and capital within the United States.

2. The Yield Battle: Stablecoins at the Center of Conflict

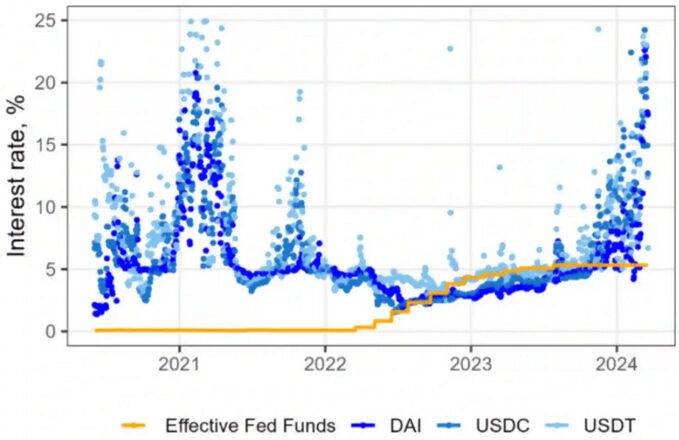

Stablecoin Yield vs Bank Deposit Yield Comparison

The most contentious issue within the CLARITY Act is whether stablecoins should be allowed to generate passive yield.

Today, many users deposit stablecoins such as USDC or USDT on exchanges or DeFi platforms to earn yields ranging from 3% to 8% annually (often quoted in USD terms, e.g., $1,000 earning $30–$80 per year). These yields have become a core gateway for crypto adoption, particularly among users seeking alternatives to low-interest bank accounts.

However, regulators—particularly banking institutions—view this as a systemic risk.

Crypto Industry Argument

Companies like Coinbase argue that:

- Users should have the right to earn yield on their assets.

- Stablecoin yield is an extension of financial freedom and efficiency.

- Restricting yield would stifle innovation and user adoption.

Banking Sector Argument

Traditional institutions, including the American Bankers Association, counter that:

- Yield-bearing stablecoins could trigger mass deposit outflows.

- This undermines the banking system’s funding model.

- It creates shadow banking risks outside regulated frameworks.

Regulatory Compromise (Current Direction)

The draft suggests:

- Passive yield (holding-based interest): likely prohibited

- Activity-based rewards (trading, liquidity provision): likely allowed

This distinction is critical. It signals a future where:

- Simply holding $10,000 in stablecoins may no longer generate $300–$800 annually.

- Active participation in DeFi or trading ecosystems may still yield returns.

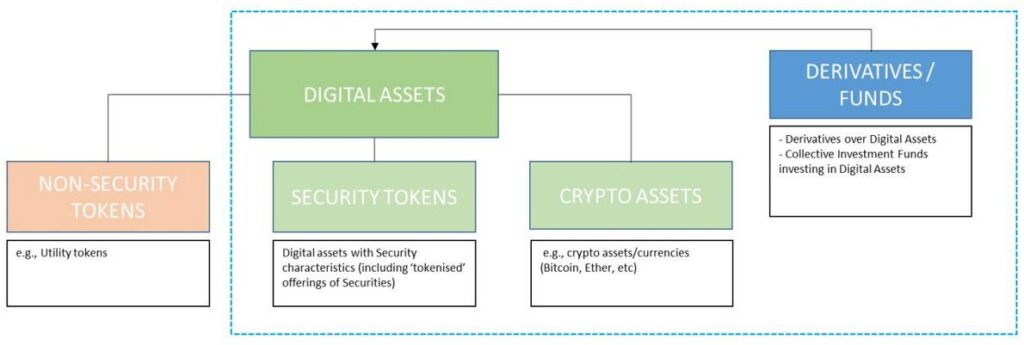

3. Classification Clarity: SEC vs CFTC vs Banking Regulators

One of the most transformative aspects of the CLARITY Act is the clear classification of digital assets.

Crypto Regulatory Classification Flow

The bill proposes:

- Digital Commodities → CFTC jurisdiction

- Securities → SEC jurisdiction

- Stablecoins → Banking regulators

This resolves one of the biggest uncertainties in crypto markets: who regulates what.

Historically, projects have faced enforcement actions without clear guidelines, creating a chilling effect on innovation. By defining jurisdiction:

- Exchanges can list assets with greater confidence.

- Developers can design tokens with regulatory clarity.

- Institutional investors gain a framework for compliance.

4. DeFi: Regulation Based on Control, Not Code

Decentralized Finance (DeFi) has long existed in a regulatory gray zone. The CLARITY Act introduces a pragmatic approach:

Regulation depends on whether an entity controls user assets.

Implications:

- Non-custodial protocols (pure smart contracts) may remain outside direct regulation.

- Custodial interfaces or platforms (where user funds are managed) will likely fall under regulatory oversight.

This creates a two-tier DeFi ecosystem:

- Pure infrastructure (low regulation)

- User-facing services (regulated)

For builders, this distinction is crucial. It shapes:

- Architecture decisions

- Business models

- Compliance strategies

5. Capital Formation: A $50M Opportunity for New Projects

The CLARITY Act introduces a streamlined fundraising pathway, allowing crypto projects to raise up to $50 million under simplified requirements.

This is significant for:

- Early-stage blockchain startups

- Token-based ecosystems

- Web3 infrastructure builders

Compared to traditional securities offerings, this lowers barriers and accelerates innovation.

In USD terms:

- A project could raise up to $50,000,000 without undergoing full SEC registration complexity.

This positions the U.S. as potentially competitive again in global crypto fundraising.

6. Market Impact: What Changes for Investors

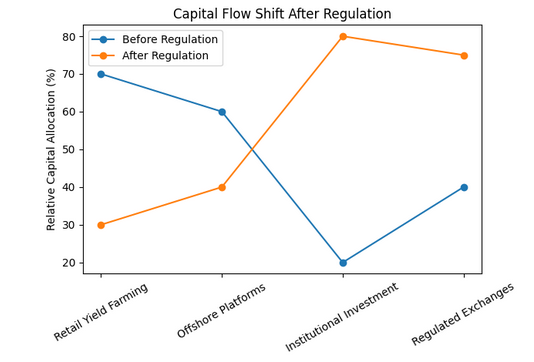

Capital Flow Shift After Regulation

1. Yield Compression

Stablecoin yields may decline significantly:

- From ~5% → potentially near 0% for passive holding

- Active strategies become more important

2. Increased Safety

Clear regulations improve:

- Custody standards

- Transparency

- Risk management

3. Institutional Inflows

With regulatory clarity:

- Pension funds

- Asset managers

- Banks

…are more likely to enter the market.

This could drive demand for major assets like Bitcoin and Ethereum, as well as compliant infrastructure projects.

7. Global Implications: Beyond the United States

The CLARITY Act will not exist in isolation. It will influence:

- Japan (already regulated under FSA oversight)

- Singapore (innovation-friendly but tightening rules)

- EU MiCA framework

We are witnessing a convergence toward:

Regulated, institution-friendly crypto markets

At the same time, regulatory arbitrage will persist:

- Users seeking yield may move to offshore platforms

- DeFi innovation may shift to less restrictive jurisdictions

8. Strategic Implications for Crypto Users

For users seeking new assets and income opportunities, the landscape is changing:

1. Passive Yield Is No Longer Reliable

Relying on stablecoin interest alone may become obsolete.

2. Active Strategies Gain Importance

Opportunities shift toward:

- Liquidity provision

- On-chain trading

- Structured products

3. Platform Selection Becomes Critical

Regulated exchanges offer:

- Higher safety

- Lower yield

Unregulated platforms offer:

- Higher yield

- Higher risk

Balancing these becomes a key strategy decision.

9. The Road Ahead: Critical Deadlines and Unresolved Issues

- Late April 2026: Senate committee markup

- May 2026: Critical legislative deadline

- Key unresolved issues:

- Final scope of yield restrictions

- DeFi regulatory boundaries

- Implementation details by regulators

Prediction markets currently estimate a ~65% probability of passage in 2026.

10. Conclusion: From Chaos to Structured Opportunity

The CLARITY Act represents a turning point in the evolution of crypto markets.

While it may reduce certain opportunities—particularly passive yield on stablecoins—it introduces something arguably more valuable:

Predictability

For investors, developers, and institutions, this means:

- Lower uncertainty

- Greater capital inflows

- More sustainable growth

The next phase of crypto will not be defined solely by speculation, but by regulated innovation and structured financial integration.

Those who adapt—by shifting strategies, understanding regulatory frameworks, and identifying new yield mechanisms—will be best positioned to benefit.