Main Points :

- Circle, issuer of USDC, is considering introducing a mechanism to make certain token transfers reversible under fraud or dispute scenarios, a sharp break from traditional blockchain immutability.

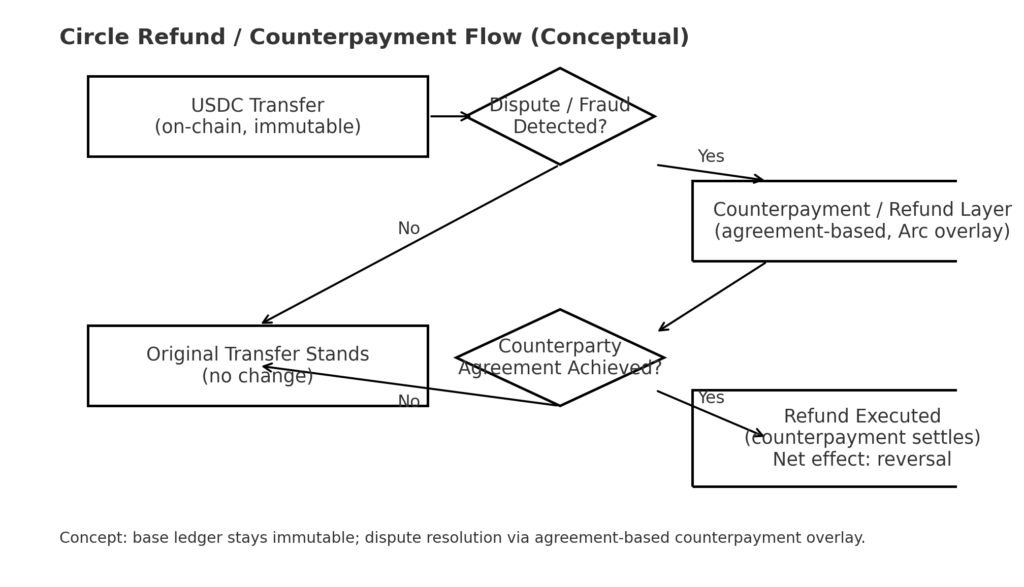

- The initiative would not change past block-level transactions per se, but add a “counterpayment / refund” layer above the base blockchain (“Arc” chain) that allows cancellation under mutual agreement.

- The move reflects Circle’s ambition to bring stablecoins closer to conventional finance, but it draws criticism for diluting decentralization and altering crypto’s ethos.

- The development comes amid a more favorable regulatory environment (e.g. U.S. stablecoin legislation), Circle’s recent IPO, and rising institutional adoption of USDC.

- However, challenges include technical design, trust among crypto purists, competitive risks, and ensuring governance for when reversibility is triggered.

- The larger stablecoin space is evolving too: European banks are planning a euro-backed stablecoin, and Circle is forging partnerships (e.g. with Ripple / OKX).

- In sum, Circle’s tentative step into reversible payments could reshape how stablecoins are perceived, bridging DeFi and TradFi—or stirring a deeper debate about what blockchain means in practice.

1. Introduction: A Radical Shift Toward Reversibility?

Traditional blockchain design rests on the principle that once a transaction is confirmed on-chain, it is final and immutable. This immutability is often championed as a core advantage over legacy finance, where chargebacks, disputes, and reversal mechanisms create friction or opacity. The recent report that Circle, the issuer behind the USDC stablecoin, is evaluating mechanisms to allow transaction reversals under fraud or dispute scenarios marks a dramatic rethinking of that principle.

In effect, Circle is proposing to introduce a secondary “refund / counterpayment” layer—somewhat analogous to credit card refunds—that overlays, rather than overwrites, the immutable ledger. In doing so, Circle aims to bridge crypto’s promise and financial institutions’ expectations for recourse. But this pivot raises deep questions—not least, about decentralization, trust, governance, and alignment of incentives.

The following sections present a synthesized and updated narrative: first summarizing the original report and its significance, then placing it in the context of recent developments in the stablecoin and blockchain space, and finally exploring implications for users, developers, and the future of programmable finance.

2. Summary of the Original Report: What Is Circle Proposing?

2.1 Background: Circle, USDC, and Arc

Circle issues the USDC stablecoin, which currently circulates in large amounts (tens of billions of dollars). The company is also developing Arc, a blockchain (or L1-style chain) tailored for financial institutions. According to the report, Arc itself would not permit direct cancellation of on-chain transactions; instead, Circle envisions adding a layer above it in which counterparties may agree on a “counterpayment” that effectively undoes or offsets a transaction in hostile or disputed cases.

Circle President Heath Tarbert (distinct from the CEO) is quoted saying that, in specific blockchains and under certain conditions with all parties’ agreement, some degree of reversal might be feasible. He frames it as learning from traditional financial mechanisms (like refunds) and argues that the ability to reverse in cases of fraud or dispute may help stablecoins gain broader adoption in legacy finance.

2.2 Key Features of the Proposed Model

- No direct protocol-level “undo”: The base ledger remains immutable. The reversal logic lives in additional layers.

- Agreement-based reversal: Any reversal would require all parties’ consent—it is not a unilateral “admin kill switch.”

- Targeted to fraud or disputes: The mechanism is explicitly framed as applicable in exceptional circumstances, not general use.

- Institutional focus: The design is oriented toward regulated entities, banks, financial flows, and foreign exchange settlement use cases.

- Controversy about centralization: Critics have already labeled the idea a dilution of blockchain philosophy; some early venture capital voices quip it “no longer a blockchain.”

2.3 Why Circle Is Considering It

From the report’s vantage point, Circle sees this move as a way to reduce friction between stablecoins and the traditional banking system:

- Financial institutions are accustomed to policies around refunds, dispute resolution, and reversibility—absent such mechanisms, stablecoins may struggle to integrate deeper.

- By offering a “refund-like” option, Circle hopes to build trust among corporates, banks, and regulators skeptical of fully irreversible systems.

- Circle may also view this as a competitive differentiator relative to other stablecoins like Tether (USDT), which typically retain stricter immutability and less institutional positioning.

2.4 Criticism and Risks

- Philosophical backlash: Many in the crypto community view immutability as sacrosanct; introducing reversibility arguably erodes one of blockchain’s core value propositions.

- Governance and abuse risk: Who decides which transfers qualify? Could the reversal mechanism be misused or exploited?

- Regulatory scrutiny: Authorities may demand clarity on when reversals are triggered, legal liabilities, and clarity of process.

- Ceding decentralization: Critics argue that this approach leans heavily toward centralization, potentially making the system more akin to a permissioned ledger.

- Technical complexity: Designing a robust, secure, auditable “refund” layer that resists fraud, chain splits, or front-running is nontrivial.

3. Recent Developments in the Stablecoin Ecosystem (2025)

To place Circle’s move in context, here are several ongoing trends and events in the stablecoin and blockchain landscape:

3.1 Regulatory Overhaul and the U.S. GENIUS / STABLE Acts

In the U.S., Congress is actively shaping legislation to regulate stablecoins—defining reserve requirements, auditing rules, and consumer safeguards. The GENIUS Act has gained attention in the Senate. Circle’s public listing and proactive regulatory alignment (e.g., reserve disclosures) are often cast as strategic moves to position itself favorably in this evolving legal environment.

Parallel to the U.S., Europe sees its own initiatives: nine major European banks (ING, UniCredit, CaixaBank, DekaBank, among others) have formed a consortium to launch a euro-pegged stablecoin, targeting a 2026 launch. This push underscores the desire of traditional institutions to reclaim a role in digital currency infrastructure rather than cede dominance to U.S.-based stablecoins.

3.2 Partnerships, Integrations, and Liquidity Expansion

Circle is actively expanding USDC’s reach through collaborations and integrations:

- OKX partnership: Circle has teamed up with exchange OKX to enhance USDC liquidity and enable 1:1 USD ⇄ USDC conversions.

- Ripple / XRPL integration: Circle and Ripple announced that USDC will be supported on the XRP Ledger (XRPL), allowing stablecoin flows on a distinct chain ecosystem.

- Fiserv collaboration: Circle and payments infrastructure firm Fiserv have formed a strategic partnership to advance stablecoin payment rails across financial ecosystems.

- Ant Group speculation: Reports suggest that Ant (Alibaba affiliate) might integrate USDC into its blockchain once regulatory compliance is assured—though Ant publicly denied some partnership rumors.

These moves indicate Circle’s ambition to spread USDC’s utility across exchanges, payment rails, and institutional corridors.

3.3 Circle’s IPO, Trust Banking Ambitions, and Market Dynamics

- IPO success: Circle went public in June 2025 on the NYSE under ticker CRCL. Its debut was met with significant investor enthusiasm and valuation jumps.

- Trust bank charter application: Circle has applied for a U.S. national trust bank license (named “First National Digital Currency Bank, N.A.” in filings) to manage USDC reserves and custody tokenized assets—though it would not accept deposits or issue loans.

- Valuation and volatility: The IPO rendered Circle a multi-billion-dollar firm. However, some analysts remain cautious. For example, Compass Point downgraded CRCL citing competition, regulatory risk, and possibly an overhyped valuation. Other firms, like Citi, still initiated coverage with a “Buy” and a $243 target.

- Stablecoin growth projections: Goldman Sachs projects USDC’s supply could grow ~40% annually through 2027, potentially fueling large expansion of Circle’s business.

3.4 Macro Insights: Stablecoins, Treasury Demand, and Hybrid Monetary Models

Two academic papers illustrate broader systemic trends:

- Stablecoin Discount & Treasury Market Impact: Tether (USDT) currently holds a notable stake in U.S. Treasury bills. The study finds that a 1% increase in Tether’s share of T-bills could reduce short-term yields by ~3.8 basis points (or more above a certain threshold). arXiv

- Hybrid Monetary Models: Another work explores integrating private stablecoins (USDC, USDT, etc.) with fiat systems in a hybrid monetary ecosystem. It argues for architectures where private issuers are backed by central bank reserves or interoperable infrastructure, strengthening stability and trust.

These studies suggest that stablecoins are not just crypto novelties but potentially systemic actors influencing traditional finance.

4. Implications for Users, Builders, and the Crypto Landscape

4.1 What Does Reversibility Mean for Users?

- Increased recourse: Users (retail or institutional) may gain more protection if they fall victim to fraud or mistaken transfers, reducing one of the common anxieties about irreversible crypto flows.

- Trust bridging: Offering a refund-like layer might make stablecoins more acceptable to institutions (e.g. banks, corporates) that demand mechanisms for dispute resolution.

- Choice matters: Some users may prefer traditional immutable tokens, while others may accept reversibility for more mainstream usability.

4.2 For Developers and Protocol Architects

- Design complexity: Architects must build a safe, foolproof “refund layer” that cannot be gamed or abused. Timing, event triggering, dispute resolution, and finality must be carefully defined.

- Governance modeling: Who decides whether a refund should be allowed? Multi-party committees? Arbitrators? DAO votes? The governance design is critical.

- Interoperability constraints: The reversibility logic will likely be localized to Arc or the extra layer—not universal across blockchains—leaving open challenges when bridging tokens or integrating with other chains.

- Tradeoffs between decentralization and control: Builders must balance the control required to handle disputes with the decentralized ethos many users expect.

4.3 Effects on the Broader Crypto and Finance Landscape

- Blurring of categories: Circle’s approach could shrink the gap between DeFi and TradFi, making stablecoins more akin to programmable bank instruments than purely decentralized tokens.

- Centralization criticism intensifies: This move may amplify criticism that stablecoin ecosystems drift toward centralized control—especially when reversibility is an option.

- Regulatory alignment: A system that resembles traditional financial controls might win favor with regulators, potentially accelerating institutional adoption.

- Competition reshuffling: Rivals like Tether or algorithmic stablecoins may respond by doubling down on immutability or by developing their own hybrid models.

- Monetary influence: As stablecoins grow, they may wield increasing influence over fiat money markets, treasury yields, and capital flows (as the academic papers above suggest).

5. What to Watch Next: Key Milestones & Risks

| Indicator | What to Watch | Why It Matters |

|---|---|---|

| Technical specs released | Circle should publish a protocol spec for its reversal layer | That will reveal whether the architecture is robust, auditable, and safe |

| Governance model and dispute framework | Who has final say, timing, appeals, criteria | Governance is the central pivot for trust and credibility |

| Regulator responses | U.S. SEC, CFTC, European regulators reactions | Regulators may challenge or endorse the architecture |

| User adoption / pilot deployment | Will financial institutions adopt reversible USDC for real flows? | It’s one thing to design it; actual use will test resilience |

| Competing responses | How Tether, other stablecoins, or banks react | Competitive counter-moves may accelerate or push back the idea |

| Market reactions to Circle stock / earnings | Investor sentiment will reflect belief in the model | A collapse in confidence could stall further innovation |

6. Conclusion: Bridging Crypto Ideals and Institutional Demands

Circle’s exploration of reversible stablecoin transactions represents a bold reimagining of what blockchain payments can do. By layering refund-like mechanisms on top of immutable ledgers, Circle is attempting to fold key elements of traditional finance—dispute resolution, recourse, conditional reversal—into the architecture of programmable money. For readers and participants in the crypto space, this is more than an incremental innovation: it is a test case in reconciling two divergent paradigms.

If successful, the model might accelerate adoption by institutions otherwise wary of irreversible flows. It could help stablecoins become more seamlessly integrated into payments, settlements, and treasury operations. But success hinges on executing governance, maintaining security, and retaining enough decentralization to preserve the unique advantages of crypto.

In the end, Circle’s move will not simply be judged by whether some transactions can be reversed—but by whether the system retains enough trust, auditability, and integrity to remain compelling in a world of competing models. The outcome may strongly influence which stablecoins attract usage, and how hybrid monetary systems evolve moving forward.