Main Points:

- China’s share of global semiconductor foundry capacity to climb from 21% in 2024 to 30% by 2030, overtaking Taiwan.

- Massive “Big Fund” state investments underpin domestic giants SMIC and Hua Hong.

- U.S. and Taiwan export curbs on Huawei and SMIC intensify China’s push for chip self-reliance.

- Stable, lower-cost domestic chip supply could reshape AI development and crypto mining economics.

- Despite the 2021 mining ban, China still accounts for a significant share of Bitcoin hashrate, with estimates from 21% to over 55% via underground operations.

- Leading Chinese ASIC makers—Bitmain, Canaan, MicroBT—are establishing U.S. production facilities to bypass tariffs and secure North American customers.

- The global crypto-mining market is projected to grow from $2.2 billion in 2024 to $3.3 billion by 2030, at a 6.9% CAGR.

1. A New Semiconductor Powerhouse

Subheading: China’s Foundry Capacity Trajectory

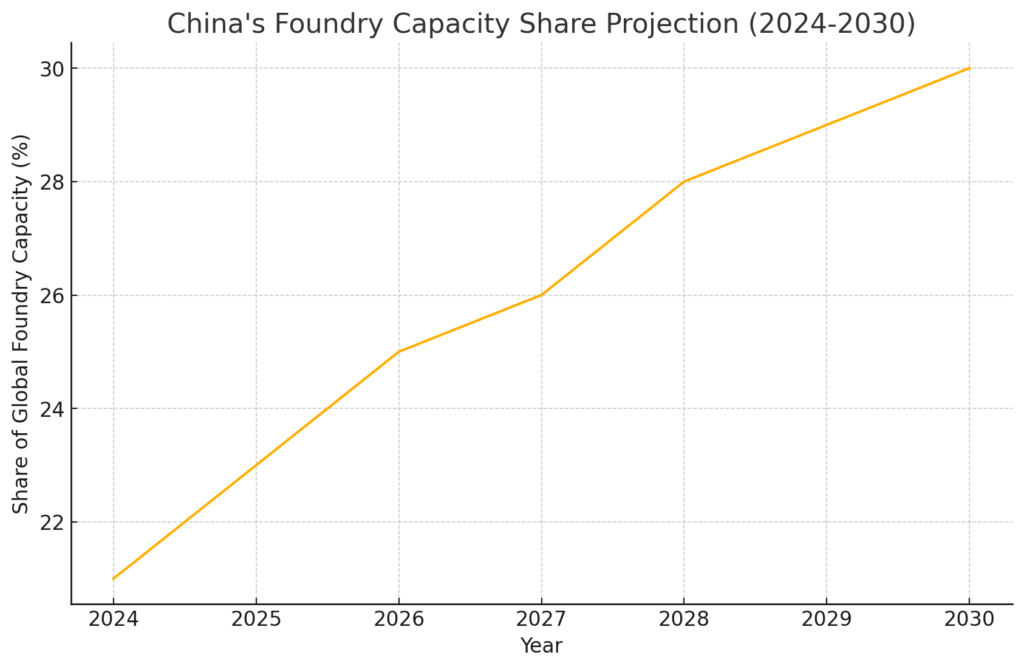

China’s foundry capacity has been on a meteoric rise. According to Yole Group, China’s share of global foundry production capacity will surge from 21% in 2024 to 30% by 2030, eclipsing Taiwan’s 23% share and positioning China as the world’s largest hub for chip manufacturing.

Figure 1 visualizes this projected growth in capacity share:

Refer to the chart above illustrating China’s foundry share (2024–2030).

2. Fueling the Surge: The “Big Fund” Strategy

Subheading: State-Backed Investment Driving Domestic Champions

China’s rapid expansion is bankrolled by the National Integrated Circuit Industry Investment Fund (the “Big Fund”), which has injected multibillion-dollar equity into domestic pure-play foundries such as SMIC and Hua Hong Semiconductor. These investments accelerate advanced-node fabs and wafer capacity—vital for both AI accelerators and crypto mining ASICs.

3. Geopolitics of Chip Supply

Subheading: Export Controls and Self-Reliance

In alignment with U.S. policy, Taiwan has enacted stringent export restrictions on Huawei and SMIC. These measures curtail Chinese access to cutting-edge lithography and packaging technologies, prompting Beijing to double down on domestic innovation and alternative supply lines. The result: an accelerated push toward achieving technological self-sufficiency and supply-chain resilience. 4. Ripple Effects for AI and Crypto Mining

Subheading: Cost Dynamics and Competitive Shifts

Semiconductors underpin AI training and inference workloads as well as cryptocurrency mining. As domestic chip costs stabilize and potentially fall, China-based AI startups and cryptocurrency miners could enjoy lower operating expenses. This dynamic may force global competitors to reassess their cost structures and could shift data-center and mining-farm deployments toward regions with cheaper, reliable chip supply.

5. China’s Underground Mining Resurgence

Subheading: Mining Ban vs. Hidden Hashrate

Officially banned since mid-2021, crypto mining persists clandestinely in China’s provinces with surplus hydropower (e.g., Sichuan). While early post-ban estimates pegged China’s share of Bitcoin network hashrate at 21% by mid-2022, more recent analyses suggest it may exceed 55%, underscoring the tenacity of underground operations and cheap energy arbitrage.

6. ASIC Makers Going West

Subheading: Bitmain, Canaan, and MicroBT in the U.S.

To circumvent U.S. tariffs and geopolitical headwinds, major Chinese ASIC vendors have begun localizing production in North America. Bitmain opened assembly lines stateside to hasten deliveries; Canaan and MicroBT are exploring U.S. facilities to avoid punitive duties. This onshoring not only secures their access to large mining markets but also hedges supply-chain risk.

7. Crypto Mining Market on an Upward Curve

Subheading: From $2.2 B to $3.3 B by 2030

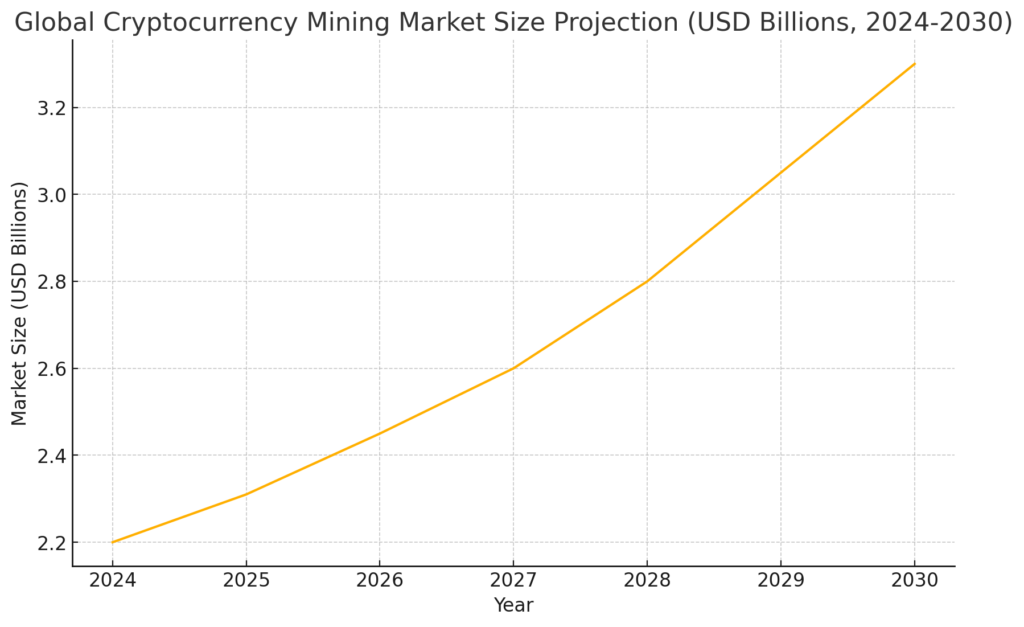

The global cryptocurrency mining market—encompassing hardware sales, hosting, and ancillary services—is forecast to expand from $2.2 billion in 2024 to $3.3 billion by 2030, at a compound annual growth rate (CAGR) of 6.9%.

Figure 2 depicts this growth trajectory:

Refer to the chart above illustrating mining market size (2024–2030).

Conclusion

China’s emergence as the largest foundry hub by 2030 signals a dramatic rebalancing of the semiconductor and crypto-mining landscapes. Massive state investments and strategic self-reliance initiatives promise stable, cost-effective chip supplies that could empower domestic AI and mining operations. Meanwhile, underground Bitcoin mining and the globalization of ASIC production underscore the resilience and adaptability of China’s crypto ecosystem. For investors and blockchain practitioners, these trends highlight new opportunities in mining hardware, hosting services, and decentralized infrastructure powered by next-generation Chinese chipmaking prowess.