Key Points :

- Pakistan has officially lifted its 2018 ban on banking access for crypto firms.

- Licensed Virtual Asset Service Providers (VASPs) can now open bank accounts under strict regulation.

- Banks are prohibited from directly trading or holding crypto assets.

- Strong AML/CFT/CPF compliance and continuous monitoring are mandatory.

- The move signals institutional alignment and opens pathways for large-scale crypto adoption.

1. A Policy Reversal That Signals a New Era

In April 2026, Pakistan made a decisive move that could reshape its financial landscape: the central bank officially allowed licensed crypto companies to open bank accounts, effectively reversing a blanket prohibition imposed in 2018. This is not merely a regulatory adjustment—it represents a strategic pivot from exclusion to controlled integration.

For years, Pakistan existed in a paradox. Despite having an estimated 40 million crypto users—one of the largest adoption bases globally—the country maintained a restrictive banking stance that forced crypto activity into informal or offshore channels. This disconnect between user demand and institutional policy created inefficiencies, risks, and missed economic opportunities.

The latest decision resolves that contradiction. By enabling regulated access to banking infrastructure, Pakistan is effectively bringing crypto activity into the formal financial system—where it can be monitored, taxed, and scaled.

This shift mirrors a broader global trend. Governments are increasingly recognizing that banning crypto does not eliminate its use; instead, it pushes activity into opaque environments. Regulation, rather than prohibition, is emerging as the preferred approach.

2. The Role of PVARA: Building a Regulatory Backbone

Central to this transition is the establishment of the Pakistan Virtual Asset Regulatory Authority (PVARA), formalized under the 2026 Crypto Act. PVARA serves as the licensing, supervisory, and enforcement body for all crypto-related activities in the country.

This institutional framework is critical. Without a dedicated regulator, integration between banks and crypto firms would remain fragmented and risky. PVARA creates a standardized gateway: only licensed entities can access banking services.

This model is comparable to regulatory structures in jurisdictions such as Dubai (VARA) and Singapore (MAS), where licensing acts as a filter for legitimacy. The implication is clear: Pakistan is not merely opening the door—it is installing a checkpoint.

For crypto entrepreneurs, this creates both an opportunity and a barrier. Entry into the regulated ecosystem requires compliance, transparency, and operational maturity. But for those who meet the criteria, the reward is access to fiat rails—a prerequisite for scaling any serious financial service.

3. Strict Separation: Protecting the Financial System

One of the most notable aspects of Pakistan’s framework is the strict separation between banks and crypto exposure.

Banks are explicitly prohibited from:

- Trading cryptocurrencies using their own capital

- Holding crypto assets on behalf of customers (outside permitted frameworks)

- Using customer deposits for crypto-related activities

At first glance, this may appear restrictive. However, it reflects a deliberate risk containment strategy.

By isolating crypto risk within licensed VASPs, regulators ensure that volatility in digital asset markets does not directly impact the traditional banking system. This approach is similar to ring-fencing mechanisms used in other financial sectors.

From a systemic perspective, this is a pragmatic compromise. It allows innovation to proceed while safeguarding financial stability—a key concern for emerging markets.

4. Operational Requirements: Segregation and Transparency

The new rules impose detailed operational requirements on VASPs and their banking partners. These include:

- Verification of regulatory licenses before account opening

- Strict segregation of company funds and customer funds

- Creation of dedicated accounts for transaction settlement

- Prohibition of using customer funds as collateral or for lending

These measures are not merely bureaucratic—they are foundational to trust.

In the absence of such safeguards, crypto platforms can easily become opaque, increasing the risk of misuse, insolvency, or fraud. By enforcing segregation and transparency, Pakistan is aligning with global best practices seen in regulated exchanges and custodial platforms.

For developers and system architects, this has direct implications. Backend systems must support:

- Multi-ledger accounting structures

- Real-time fund segregation

- Audit-ready transaction histories

- Regulatory reporting interfaces

In other words, compliance is not an add-on—it is a core system requirement.

5. AML/CFT/CPF: From Compliance to Continuous Surveillance

Pakistan’s framework goes beyond standard compliance checks. It introduces a model of continuous monitoring.

Banks are required to:

- Conduct thorough due diligence on VASPs

- Understand their business models, user onboarding processes, and geographic exposure

- Monitor transactions on an ongoing basis

- Report suspicious activity in accordance with AML laws

This aligns with FATF (Financial Action Task Force) recommendations and reflects a shift from static compliance to dynamic risk management.

For the crypto industry, this has significant implications. Platforms must implement:

- Transaction monitoring systems

- Risk scoring engines

- Travel Rule compliance mechanisms

- Integration with reporting frameworks

This is particularly relevant for companies like yours operating as EMI/VASP entities. The expectation is no longer just to comply—but to demonstrate proactive risk detection and response.

6. Global Context: Why This Move Matters Now

Pakistan’s decision does not exist in isolation. It is part of a broader global realignment in crypto regulation.

Several key trends are converging:

- The rise of stablecoins as cross-border payment tools

- Increasing institutional interest in digital assets

- Regulatory clarity emerging in major markets (US, EU, UAE, Asia)

- The integration of crypto into traditional financial infrastructure

For example, partnerships involving stablecoins for cross-border settlements—such as the reported collaboration with World Liberty Financial—highlight the practical use cases driving policy change.

In this context, Pakistan’s move can be seen as strategic positioning. By enabling regulated crypto activity, the country is preparing to participate in the next phase of global financial innovation.

7. Market Implications: New Opportunities for Builders and Investors

For readers seeking new crypto assets, revenue streams, or practical blockchain applications, this development opens several avenues:

1. Regulated Exchange and Custody Services

Licensed VASPs can now operate with direct banking support, enabling fiat on/off ramps—a critical component for user adoption.

2. Cross-Border Payment Solutions

With a large diaspora and remittance flows, Pakistan is well-positioned to leverage crypto for cheaper and faster international transfers.

3. Stablecoin Infrastructure

The regulatory framework supports the integration of stablecoins into payment systems, particularly for settlement and liquidity management.

4. Compliance Technology (RegTech)

As regulatory requirements increase, demand for AML, KYC, and monitoring solutions will grow—creating opportunities for specialized platforms.

5. Tokenization and Asset Representation

With regulatory oversight in place, tokenized assets—ranging from real estate to commodities—become more feasible.

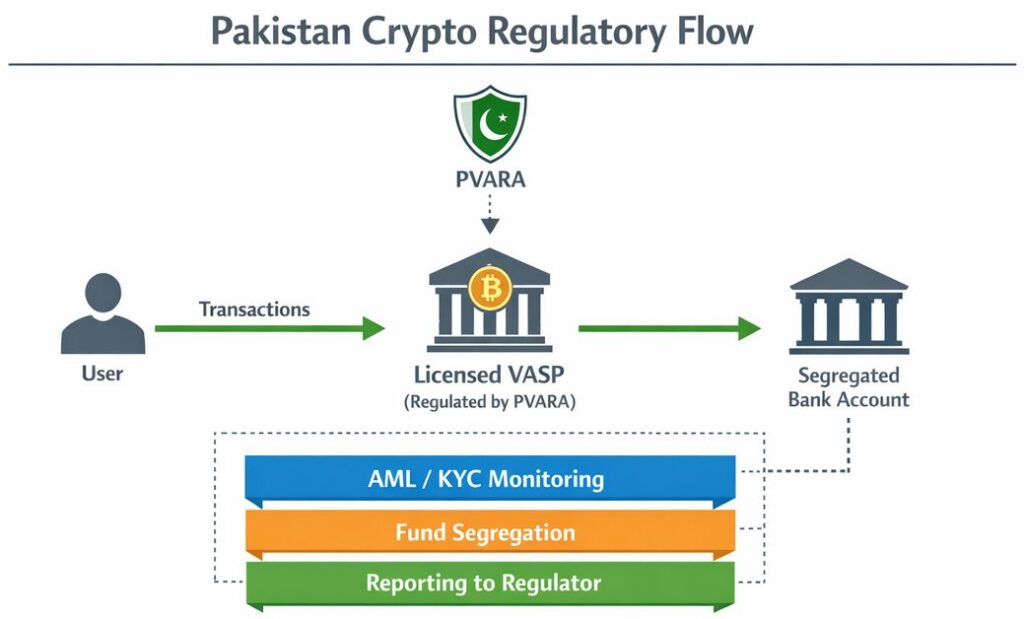

Pakistan Crypto Regulatory Flow (Bank ↔ VASP ↔ User)

Image description: A flow diagram showing:

User → VASP (licensed by PVARA) → Bank Account (segregated)

With compliance layers: AML/KYC monitoring, fund segregation, reporting lines to regulator.

8. Risks and Limitations: Not a Free Market

Despite the positive outlook, it is important to recognize the limitations.

- Banks remain insulated from direct crypto exposure

- Regulatory approval processes may be stringent and slow

- Compliance costs could be high for smaller players

- Enforcement capacity will determine real-world effectiveness

Moreover, geopolitical and macroeconomic factors could influence how aggressively Pakistan pursues crypto integration.

This is not a deregulated environment—it is a controlled ecosystem. Success will depend on the balance between innovation and oversight.

9. Strategic Insight: From Informal to Institutional

The most important takeaway is the transition from an informal crypto economy to an institutional one.

This shift has profound implications:

- Capital flows become traceable and scalable

- Institutional investors gain confidence to enter the market

- Infrastructure becomes standardized and interoperable

- Regulatory arbitrage opportunities diminish

For builders, this means designing systems that are compliant by default.

For investors, it means evaluating projects based on regulatory readiness—not just technical innovation.

Conclusion: A Blueprint for Emerging Markets

Pakistan’s decision to allow bank accounts for licensed crypto firms marks a turning point—not only for the country but for emerging markets globally.

It demonstrates that:

- Crypto adoption cannot be suppressed by prohibition

- Regulation is the key to unlocking institutional participation

- Integration with banking systems is essential for scalability

For those exploring new crypto assets, revenue opportunities, and blockchain applications, this development is more than news—it is a signal.

The next wave of growth will not come from unregulated experimentation, but from compliant, scalable, and interoperable systems that bridge traditional finance and decentralized technology.

Pakistan has taken a step in that direction. The question now is which players will move fast enough to capitalize on it.