Main Points :

- Europe is undergoing a structural fiscal shift driven by massive defense spending increases

- Rising debt levels are putting pressure on sovereign bonds, interest rates, and currency stability

- IMF projections suggest long-term fiscal deterioration tied to defense expansion

- Institutional investors are increasingly positioning Bitcoin as a macro hedge

- Bitcoin is evolving from a speculative asset into a strategic reserve alternative

1. A Structural Break in Europe’s Fiscal Discipline

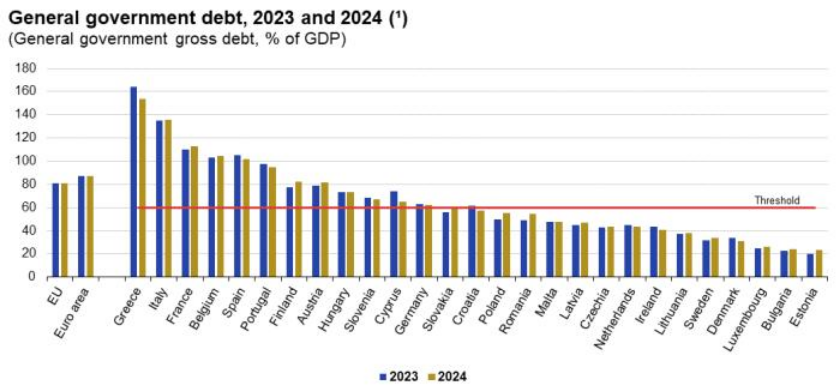

In 2026, Europe entered a new fiscal era—one that may redefine the global monetary landscape for years to come. For decades, countries like Germany symbolized fiscal restraint, anchored by strict constitutional rules such as the “debt brake,” which limited deficits to 0.35% of GDP. However, this paradigm has now shifted dramatically.

Germany has effectively suspended this rule, launching a €500 billion ($540 billion) special fund dedicated to defense and infrastructure. This move is not isolated. At the NATO summit in June 2025, member states formally committed to raising defense spending from 2% to 5% of GDP by 2035. Collectively, this signals a nearly €800 billion ($864 billion) rearmament initiative across Europe within just a few years.

This is not merely a geopolitical adjustment—it is a structural economic transformation. Fiscal expansion of this magnitude inevitably reshapes inflation dynamics, interest rate trajectories, and currency confidence.

2. IMF Warning: Defense Spending Comes at a Cost

According to the IMF’s April 2026 World Economic Outlook, defense-driven fiscal expansion has predictable macroeconomic consequences.

In a typical scenario:

- Fiscal deficits worsen by approximately 2.6 percentage points of GDP within 2.5 years

- Public debt increases by roughly 7 percentage points within 3 years

- In wartime conditions, debt expansion can surge to 14 percentage points

While defense spending can stimulate short-term economic activity, it often crowds out private investment. Governments may divert resources from productive sectors such as education, healthcare, and innovation, thereby weakening long-term growth potential.

This creates a paradox: short-term economic stimulation at the expense of long-term fiscal sustainability.

3. France: The Eurozone’s Emerging Weak Link

Among European economies, France stands out as a potential fiscal flashpoint.

Already subject to the EU’s Excessive Deficit Procedure (EDP), France has yet to fully align its fiscal strategy with the new defense mandates. Its sovereign credit rating has come under pressure, and the yield spread between French and German bonds continues to widen.

At the same time, the spread between French and Italian bonds—historically a measure of fiscal divergence—has nearly disappeared. This suggests that markets are reassessing relative risk within the Eurozone.

The implication is profound: the euro, as a unified currency, may increasingly reflect internal imbalances among member states. This undermines confidence in the currency itself.

4. Rising Interest Rates and the Risk of Stagflation

The expansion of defense spending is largely funded through sovereign debt issuance. This increases bond supply, pushing yields higher.

In Europe and the UK, expectations are building for multiple rate hikes through 2026. UK long-term yields are already among the highest in the G7, with ultra-long bonds (30+ years) facing significant upward pressure.

This dynamic introduces a dangerous feedback loop:

- Increased spending → higher inflation

- Higher inflation → tighter monetary policy

- Higher rates → increased debt servicing costs

- Increased costs → further fiscal strain

This cycle raises the risk of stagflation—a combination of slow economic growth and persistent inflation.Insert European Debt vs Interest Rate Spiral

5. Currency Confidence Under Pressure

At its core, this fiscal transformation raises a fundamental question: what underpins the value of fiat currencies?

As governments expand balance sheets and issue more debt, the real value of currency may erode. Investors begin to question whether traditional sovereign-backed assets can preserve wealth in real terms.

This is not a new concern—but the scale and coordination of current fiscal expansion amplify the issue significantly.

6. Bitcoin: A Neutral Monetary Alternative

Against this backdrop, Bitcoin’s value proposition becomes clearer.

Unlike fiat currencies, Bitcoin is:

- Not controlled by any central authority

- Not subject to discretionary monetary policy

- Programmatically scarce (21 million supply cap)

In an environment of expanding sovereign debt and potential currency debasement, Bitcoin offers an alternative: a non-sovereign store of value.

7. Institutional Accumulation Signals a Shift

Recent market data reveals a critical shift in Bitcoin ownership dynamics.

In Q1 2026:

- Retail investors sold approximately 62,000 BTC

- Institutions and corporations accumulated around 69,000 BTC

Additionally, BlackRock’s spot Bitcoin ETF (IBIT) recorded $269 million in inflows on April 9 alone. Total inflows into U.S. spot Bitcoin ETFs have exceeded $53 billion.

This divergence suggests that sophisticated investors are positioning ahead of a macroeconomic transition.

Institutional vs Retail BTC Flows

8. Bitcoin as Strategic Reserve Asset

Bitcoin is increasingly viewed not just as a speculative instrument, but as a strategic reserve asset.

For institutions, the rationale includes:

- Hedging against currency debasement

- Diversifying away from sovereign risk

- Gaining exposure to a non-correlated asset

This mirrors historical shifts where gold played a similar role. However, Bitcoin introduces portability, transparency, and programmability—features aligned with a digital financial system.

9. Implications for Investors and Builders

For crypto investors and builders, this macro shift creates multiple opportunities:

Investment Opportunities

- Long-term accumulation of BTC as a macro hedge

- Exposure to Bitcoin-related financial products (ETFs, derivatives)

- Strategic allocation alongside traditional assets

Business Opportunities

- Development of BTC-based financial infrastructure

- Cross-border settlement solutions using blockchain

- Hybrid models integrating fiat and decentralized systems

Strategic Consideration

The key question is no longer “Should crypto be part of a portfolio?”

It is now:

“What percentage of assets should be outside the fiat system?”

Conclusion: A Monetary Regime in Transition

Europe’s defense-driven fiscal expansion is more than a policy shift—it is a signal of a broader transformation in the global financial system.

As sovereign debt rises and currency confidence is tested, the role of alternative assets becomes increasingly important. Bitcoin, with its decentralized architecture and fixed supply, stands at the intersection of this transition.

Institutional investors appear to recognize this early. Their accumulation patterns suggest a long-term thesis: that the future of value storage may not be tied to any single nation, but to globally neutral systems.

For those seeking new crypto assets, revenue opportunities, and practical blockchain applications, this moment represents not just risk—but structural opportunity.