Key Points :

- Crypto VC is shifting from early-stage speculation to late-stage consolidation

- The market has structurally matured—not just reacting to a bear cycle

- Early-stage ROI has collapsed, with most new tokens underperforming

- M&A activity surged to $8.6B, signaling industry consolidation

- Capital is flowing from Web3 into AI-focused investments

- Emerging themes: AI agents, prediction markets, and RWA tokenization

- The next cycle may be defined by AI-driven finance and real-world assets (RWA)

1. From Gold Rush to Structural Maturity

The cryptocurrency venture capital (VC) market is undergoing a profound transformation—one that signals not merely a cyclical downturn but a deeper structural evolution of the industry itself. According to insights shared by Alex Thorn of Galaxy Digital, the decline in early-stage investments is not simply a byproduct of bearish sentiment but rather a reflection of the industry reaching a new phase of maturity.

In the early days of crypto—particularly during the 2016–2018 ICO boom and the subsequent DeFi and NFT surges of 2020–2022—capital flowed aggressively into nascent projects. The logic was simple: the infrastructure was still being built, and almost any new idea had the potential to capture value. Exchanges, wallets, and token issuance platforms were greenfield opportunities.

That era, however, appears to be over.

Today, core infrastructure—centralized exchanges, custodial services, L2 scaling solutions, and even cross-chain bridges—has largely been established. The low-hanging fruit has been picked. As a result, the barrier to creating meaningful innovation has increased dramatically. Investors are no longer funding ideas—they are funding execution, traction, and defensibility.

This transition marks the end of the “anything can work” phase and the beginning of a more disciplined capital environment.

2. The Collapse of Early-Stage Returns

Recent data underscores the severity of this shift. In Q1 2026, only 8 newly listed tokens achieved returns greater than 1x, meaning that the overwhelming majority failed to outperform even their listing price.

This is a stark contrast to previous cycles, where early investors often saw exponential returns within weeks or months of token launches. Today, liquidity fragmentation, tighter market conditions, and increased scrutiny have made such outcomes rare.

Moreover, the industry has witnessed a wave of project shutdowns. Platforms like Magic Eden (in certain segments), Nifty Gateway, and Dmail have either scaled back operations or faced existential challenges. In Q1 alone, 86 crypto projects entered liquidation.

This is not merely creative destruction—it is a cleansing process that reflects a maturing market where only sustainable business models can survive.

3. From Buyer’s Market to Seller’s Market

Venture capitalist Tom Dunleavy described the current environment as a transition from a “buyer’s market” to a “seller’s market.” Historically, investors had the upper hand, cherry-picking among countless early-stage opportunities.

Now, however, the dynamic has flipped. High-quality, proven projects command premium valuations, and competition among investors to secure allocations has intensified.

At the same time, fewer funds are willing to take risks on seed-stage ventures. This has led to a paradox: while capital still exists, it is increasingly concentrated in later-stage deals.

For the few VC firms still willing to invest early, this environment presents a unique opportunity. With reduced competition, they can access promising projects at favorable terms—provided they can identify true innovation amid the noise.

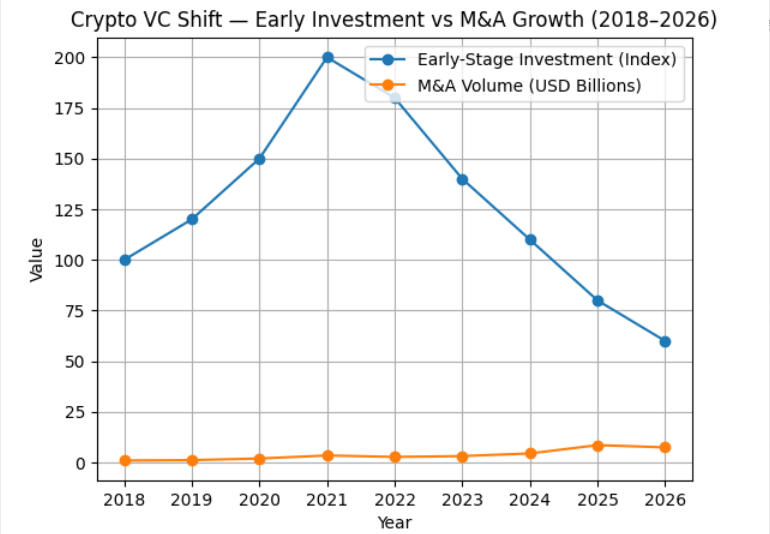

4. The Rise of Consolidation: $8.6 Billion in M&A

Perhaps the clearest indicator of market maturity is the surge in mergers and acquisitions (M&A). In 2025, crypto-related M&A activity reached 267 deals totaling $8.6 billion, a fourfold increase year-over-year.

This trend signals a shift in how value is created in the industry. Instead of funding new startups, capital is increasingly being deployed to acquire and integrate existing businesses.

Well-capitalized players are absorbing weaker competitors, consolidating market share, and building vertically integrated ecosystems. This mirrors patterns seen in traditional industries, where consolidation follows periods of rapid expansion.

For investors, this represents a different kind of opportunity—one focused on strategic positioning rather than speculative upside.

Crypto VC Shift — Early Investment vs M&A Growth (2018–2026)

(Description: A line graph showing declining early-stage funding vs rising M&A volume, with M&A reaching $8.6B in 2025.)

5. The Disappearance of “Web3” as an निवेश Category

Another critical factor is the effective disappearance of “Web3” as a standalone investment category. During the 2021 cycle, Web3 served as a catch-all narrative that attracted massive inflows of capital into early-stage projects.

Today, that narrative has fragmented.

Investors are no longer satisfied with broad thematic labels. Instead, they demand specificity: What problem is being solved? What is the revenue model? Where is the user adoption?

Without a unifying narrative, early-stage funding has become more selective—and more scarce.

6. Capital Flight to AI: A Competing Frontier

One of the most significant developments reshaping crypto VC is the migration of capital into artificial intelligence (AI). Many crypto-focused funds have effectively become hybrid AI funds, reallocating resources toward machine learning, agent-based systems, and infrastructure for autonomous computation.

This shift is not accidental. AI represents a parallel frontier with equally transformative potential—and, in the current environment, arguably clearer monetization pathways.

Within crypto itself, AI is emerging as a dominant theme. Projects focused on AI agents, autonomous trading systems, and decentralized compute networks are attracting disproportionate attention.

For example, prediction platforms like Polymarket are generating daily fees of approximately $1.9 million, demonstrating real demand for certain niches.

Meanwhile, AI-related crypto sectors have shown relative resilience, declining only about 30% from peak, compared to 80% drawdowns in segments like DeSci and SocialFi.

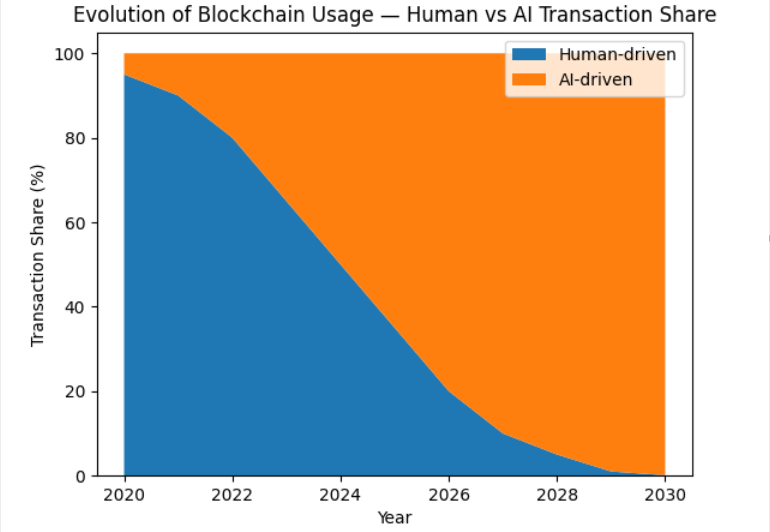

7. Toward an AI-Driven Financial System

Looking ahead, the integration of AI and blockchain could redefine the very nature of financial systems. Galaxy Digital has suggested that up to 99.9% of on-chain transactions could eventually be executed by AI agents.

This implies a radical shift:

- From human-driven transactions to machine-driven economies

- From user interfaces designed for people to protocols optimized for algorithms

- From Web3 as a user-centric paradigm to infrastructure for autonomous agents

In this context, blockchain becomes less about decentralization for individuals and more about trustless coordination between machines.

Evolution of Blockchain Usage — Human vs AI Transaction Share

(Description: A stacked area chart showing human-driven transactions declining while AI-driven transactions approach 99.9% over time.)

8. The Next Meta: Real-World Assets (RWA)

Despite the challenges facing early-stage investment, new narratives are beginning to emerge. Among them, tokenization of real-world assets (RWA) stands out as a leading candidate for the next major wave.

RWA involves bringing traditional assets—such as equities, bonds, and commodities—onto blockchain networks. This creates opportunities for:

- Fractional ownership

- Increased liquidity

- Global accessibility

- Programmable financial instruments

Major asset managers are increasingly viewing RWA as the bridge between traditional finance and crypto. Unlike previous speculative cycles, RWA is grounded in tangible value, making it more attractive to institutional investors.

9. Market Psychology: Fatigue or Transition?

The current pessimism in the crypto market may also reflect psychological fatigue. After multiple boom-and-bust cycles, participants are less willing to embrace hype without substance.

Researcher Zack Pokorny notes that the absence of bold experimentation contributes to a sense of stagnation. However, this may be a temporary phase—a necessary reset before the next wave of innovation.

Indeed, as Lucas Tcheyan suggests, these discussions are typical of bear markets. The key question is not whether early-stage investing will return, but what form it will take in the next cycle.

10. Conclusion: End of an Era—or Prelude to the Next?

The evidence is clear: the crypto VC market has entered a new phase. The era of indiscriminate early-stage investment is fading, replaced by a more mature, disciplined, and competitive environment.

Yet this should not be mistaken for decline.

Rather, it represents a transition—from speculation to sustainability, from narrative-driven funding to fundamentals-driven investment. The next wave of innovation is already taking shape, driven by AI integration and the tokenization of real-world assets.

For investors and builders alike, the challenge is no longer to chase hype but to anticipate structural shifts. The opportunities remain—but they are now concentrated in fewer, more sophisticated domains.

The gold rush may be over. But the foundations of a new financial system are being laid—quietly, methodically, and with far greater consequence.