Main Points :

- The International Monetary Fund published a major policy paper on April 2, 2026, warning that unregulated tokenization could destabilize the global financial system.

- Tokenization is not just efficiency—it represents a structural transformation of finance.

- The IMF identifies three forms of tokenized money: bank deposits, stablecoins, and wholesale CBDCs.

- A five-pillar global policy framework is urgently needed to maintain financial stability.

- The future of finance will diverge depending on regulatory coordination, interoperability, and the role of central banks.

1. A Turning Point: IMF Sounds the Alarm on Unregulated Tokenization

The International Monetary Fund has issued one of its most consequential warnings to date: tokenization—if left unregulated—could introduce systemic risks that rival or exceed those seen during past financial crises.

In its April 2026 policy paper “Tokenized Finance,” the IMF argues that global regulators, central banks, and financial institutions are at a critical juncture. Unlike previous waves of fintech innovation, tokenization is not simply about making transactions faster or cheaper. Instead, it represents a deep restructuring of how financial systems operate.

Tobias Adrian, Director of the IMF’s Monetary and Capital Markets Department, emphasizes that tokenization reshapes the very foundations of finance: payments, liquidity management, and risk allocation. This shift, if unmanaged, could amplify vulnerabilities through:

- Ultra-fast transaction execution

- Increased concentration of liquidity

- Fragmentation across incompatible blockchain systems

This warning comes amid growing enthusiasm from institutions like BlackRock, whose CEO has described tokenization as an “internet-level transformation.” Yet, the IMF cautions that such transformative power must be accompanied by equally robust governance.

2. Beyond Efficiency: Tokenization as Structural Transformation

Traditional digital finance—online banking, payment apps, and centralized exchanges—has largely focused on improving efficiency within existing frameworks. Tokenization, however, goes much further.

2.1 The Three Core Innovations

Tokenized finance introduces three defining characteristics:

- Programmability: Financial contracts can execute automatically via smart contracts.

- Shared Ledger Systems: Transactions are recorded on synchronized, distributed ledgers rather than siloed databases.

- Near-Instant Settlement Finality: Transactions settle in real-time or near real-time, reducing counterparty risk.

These features collectively eliminate many intermediaries but also relocate risk. Instead of being concentrated in institutions, risk shifts toward:

- Code vulnerabilities

- Data oracle failures

- Infrastructure resilience

This creates a new regulatory challenge: supervision must extend beyond institutions to include algorithms, governance structures, and technical infrastructure.

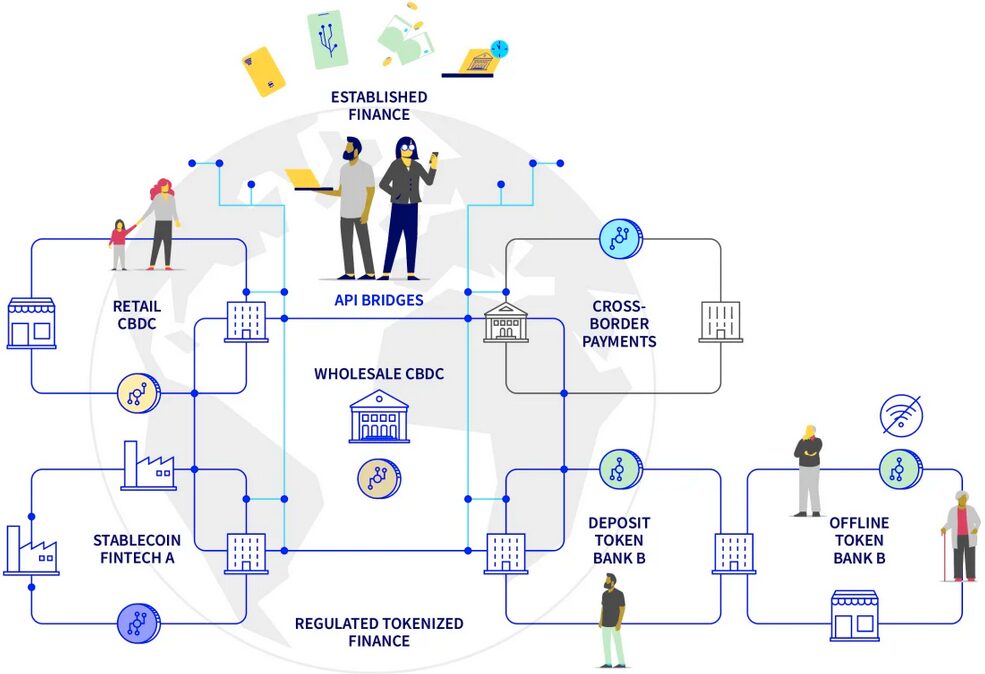

3. The Three Types of Tokenized Money and Their Risk Profiles

The IMF categorizes tokenized money into three primary forms, each with distinct implications for financial stability.

3.1 Tokenized Bank Deposits

These represent traditional bank deposits converted into digital tokens. They maintain a direct link to the banking system and are generally considered stable, provided the issuing bank remains solvent.

3.2 Regulated Stablecoins

Stablecoins—often pegged to fiat currencies like the US dollar—are widely used in crypto markets. However, the IMF highlights several vulnerabilities:

- Dependence on reserve asset quality

- Liquidity risks in government bond and repo markets

- Redemption risks tied to issuer credibility

Because most stablecoins are USD-denominated, emerging markets face currency mismatch risks, potentially destabilizing local economies.

3.3 Wholesale Central Bank Digital Currencies (wCBDCs)

wCBDCs are designed for institutional use, enabling central banks to provide settlement assets directly on tokenized infrastructures. These instruments could anchor trust in tokenized ecosystems but require careful integration.

3.4 The Rise of Synthetic CBDCs (sCBDC)

The IMF also explores a hybrid model—synthetic CBDCs—where private issuers fully back tokens with central bank reserves. This model balances innovation with public trust but introduces new supervisory requirements.

4. The IMF’s Five-Pillar Policy Framework

To address these risks, the IMF proposes a comprehensive five-pillar roadmap.

4.1 Anchor Tokenized Systems to Safe Money

Maintaining the “singleness of money” is critical. Tokenized systems must be anchored to risk-free assets such as central bank money or strictly regulated tokenized deposits.

4.2 Apply the Principle of “Same Activity, Same Risk, Same Regulation”

Regulatory frameworks must ensure that economically equivalent activities are subject to consistent oversight, regardless of technological implementation.

4.3 Establish Legal Clarity

Clear legal definitions are needed for:

- Ownership rights

- Settlement finality

- Token classification

Without legal certainty, disputes could undermine trust in tokenized systems.

4.4 Ensure Interoperability and Global Coordination

Fragmentation across blockchain systems could create inefficiencies and systemic risks. International coordination is essential to enable seamless cross-border transactions.

4.5 Build 24/7 Liquidity and Crisis Management Frameworks

Tokenized finance operates continuously. Central banks must adapt by providing:

- Real-time liquidity support

- Crisis intervention mechanisms

- Direct participation in tokenized infrastructures

5. Three Possible Futures for Tokenized Finance

The IMF outlines three potential scenarios depending on policy decisions:

5.1 Fragmented Private Dominance

If regulation lags, private stablecoins could dominate, leading to fragmented systems and increased systemic risk.

5.2 Public-Private Hybrid Model

A balanced approach where central banks and private innovators collaborate, ensuring stability while fostering innovation.

5.3 Central Bank-Centric System

A more controlled environment dominated by CBDCs, potentially limiting private sector innovation but maximizing stability.

6. Market Context: Institutional Momentum Meets Regulatory Reality

The IMF’s warning comes at a time when institutional adoption of tokenization is accelerating rapidly.

Major financial players—including BlackRock—are tokenizing funds and assets, while banks explore blockchain-based settlement systems. Meanwhile, stablecoin markets continue to expand, exceeding hundreds of billions in market capitalization.

At the same time:

- Governments are advancing CBDC pilots

- Cross-border payment initiatives are increasing

- Regulatory frameworks remain uneven across jurisdictions

This divergence underscores the IMF’s concern: innovation is outpacing regulation.

Tokenized Finance Structure

7. Strategic Implications for Crypto Investors and Builders

For readers seeking new crypto assets, revenue opportunities, and practical blockchain applications, the IMF’s framework offers critical insights.

7.1 Regulatory Arbitrage Will Shrink

Projects relying on weak regulatory environments may face increasing pressure. Compliance-ready models will gain advantage.

7.2 Infrastructure Becomes the New Alpha

Opportunities will shift toward:

- Settlement layers

- Interoperability protocols

- Compliance tooling

7.3 Stablecoins and CBDCs Will Define Liquidity

The battle between private stablecoins and public digital currencies will shape liquidity flows across the crypto ecosystem.

7.4 Tokenization of Real-World Assets (RWA)

Tokenized bonds, equities, and funds will expand rapidly, driven by institutional demand.

8. Conclusion: A Narrow Window for Coordination

The IMF’s message is clear: tokenization is inevitable, but its outcomes are not predetermined.

Without coordinated regulation, tokenized finance could amplify systemic risks. With the right frameworks, however, it could deliver:

- Greater efficiency

- Enhanced transparency

- Broader financial inclusion

The next few years will determine whether tokenized finance becomes a stabilizing force—or a source of global financial instability.