Key Takeaways :

- Global debt has reached a historic $348 trillion, exposing inefficiencies in traditional credit systems

- Digital lending platforms remain under 0.2% of total market share, signaling massive upside potential

- Legacy systems like FICO-based credit scoring are outdated and costly

- AI-driven underwriting and blockchain-based settlement rails are emerging as critical control layers

- By 2030, lending may resemble cloud infrastructure, with modular, API-driven financial services

Introduction: A Massive Market Ready for Disruption

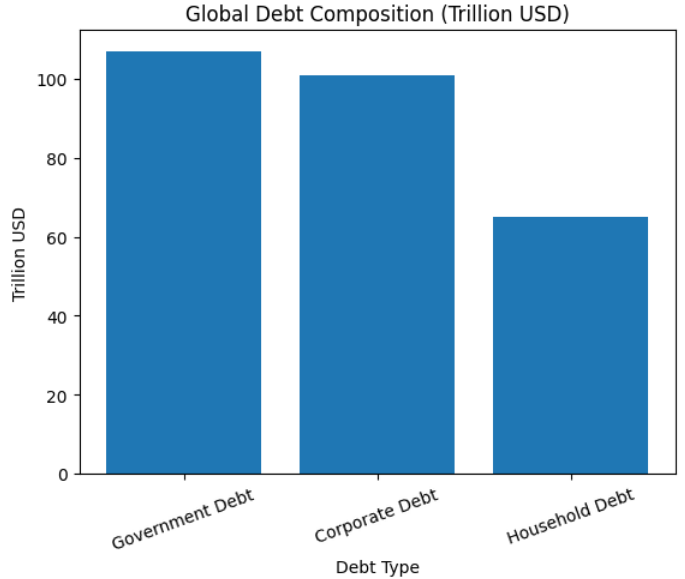

The global financial system stands at a critical inflection point. According to data analyzed by Artemis and based on figures from the Institute of International Finance (IIF), total global debt reached an unprecedented $348 trillion by the end of 2025. This includes $107 trillion in government debt, $101 trillion in corporate debt, and $65 trillion in household debt.

Despite the scale of this market, the infrastructure supporting lending remains surprisingly outdated. While fintech innovation has transformed payments, trading, and even asset custody, lending—the backbone of global finance—still relies heavily on legacy systems designed decades ago.

This mismatch between scale and innovation is creating a historic opportunity. The convergence of artificial intelligence (AI) and blockchain technology is now poised to fundamentally reshape how credit is assessed, distributed, and settled.

Global Debt Composition

The Inefficiency Problem: A System Frozen in Time

One of the most striking observations from Artemis is how little the core infrastructure of lending has evolved. Credit scoring systems such as FICO, introduced in 1989, still dominate underwriting decisions in major markets like the United States.

This reliance on outdated models leads to several inefficiencies:

- High origination costs: Mortgage origination in the U.S. costs approximately $11,000 per loan, nearly double early 2010s levels

- Slow processing times: Manual verification and siloed data systems delay approvals

- Limited inclusion: Millions of individuals and SMEs remain underserved due to rigid scoring frameworks

These inefficiencies are not just operational—they represent a structural drag on global economic growth.

A Tiny Digital Footprint in a Giant Market

Despite years of fintech hype, digital lending platforms account for only $590 billion to $680 billion in total volume—less than 0.2% of the global debt market.

This disparity highlights two critical insights:

- The opportunity is enormous

- Adoption barriers remain significant

Traditional banking institutions still dominate due to regulatory trust, capital access, and entrenched customer relationships. However, their vertically integrated models are increasingly being challenged by more flexible, technology-driven alternatives.

From Vertical Banks to Horizontal Financial Stacks

Historically, banks operated as vertically integrated entities—handling everything from customer onboarding to underwriting, funding, and servicing.

Today, this model is fragmenting.

A new horizontal stack is emerging, where specialized providers handle distinct layers of the lending process:

- Data layer: Alternative credit data, behavioral analytics

- Intelligence layer: AI-driven underwriting and risk modeling

- Execution layer: Loan origination and servicing platforms

- Settlement layer: Blockchain-based payment rails

This modularization mirrors the evolution of cloud computing, where monolithic systems gave way to distributed, API-driven architectures.

The Two Critical Control Points: AI and Blockchain

Artemis identifies two “choke points” that will define the winners in this transformation:

1. The Intelligence Layer (AI Underwriting)

AI is rapidly transforming credit assessment by enabling:

- Real-time risk analysis using alternative data

- Dynamic pricing of loans based on behavioral signals

- Automated decision-making at scale

Unlike traditional credit scoring, AI models can incorporate:

- Transaction histories

- Mobile usage patterns

- On-chain activity

- Social and economic signals

This allows for a far more nuanced and inclusive understanding of creditworthiness.

2. The Settlement Layer (Blockchain Rails)

Blockchain introduces a new paradigm for financial settlement:

- Instant or near-instant transactions

- Reduced counterparty risk

- Programmable money via smart contracts

- Global interoperability without intermediaries

Stablecoins and tokenized assets are already demonstrating how blockchain can reduce friction in cross-border lending and payments.

Recent Trends: Institutional Momentum and Tokenization

Beyond Artemis’ analysis, broader market trends reinforce this shift:

Rise of Tokenized Credit Markets

Tokenization is enabling:

- Fractional ownership of debt instruments

- Increased liquidity in traditionally illiquid markets

- Transparent, on-chain tracking of loan performance

Projects in decentralized finance (DeFi) are already experimenting with on-chain credit protocols, bridging traditional finance (TradFi) and crypto-native ecosystems.

Institutional Adoption Accelerates

Major financial institutions are increasingly exploring:

- Private credit tokenization

- Blockchain-based settlement networks

- AI-enhanced risk modeling

This convergence signals that crypto is no longer a parallel system—it is becoming embedded within the core of global finance.

Toward 2030: Lending as Infrastructure

Artemis predicts that by 2030, lending will resemble cloud computing:

- A few dominant full-stack platforms will control multiple layers

- Smaller players will integrate via APIs and blockchain rails

- Financial services will become programmable and composable

This transformation has profound implications:

- Lower costs: Automation reduces operational overhead

- Greater access: Underserved populations gain credit access

- Faster innovation: Modular systems enable rapid experimentation

Strategic Implications for Crypto Investors and Builders

For readers seeking new crypto opportunities and revenue streams, this shift presents several actionable insights:

1. Focus on Infrastructure, Not Just Tokens

The biggest value may lie in:

- AI underwriting platforms

- On-chain settlement protocols

- Data aggregation layers

2. Watch the Convergence of TradFi and DeFi

Hybrid models combining:

- Regulatory compliance

- Blockchain efficiency

- Institutional capital

will likely dominate the next phase.

3. Identify Emerging “Choke Point” Players

Companies controlling:

- Credit intelligence

- Settlement rails

could capture disproportionate value, similar to how AWS dominates cloud infrastructure.

Conclusion: A Once-in-a-Generation Transformation

The $348 trillion global debt market is undergoing a fundamental transformation. While fintech has already reshaped payments and trading, lending—the largest and most complex segment—has remained largely untouched.

That is now changing.

AI is redefining how credit risk is understood, while blockchain is reinventing how value moves across borders. Together, they are creating a new financial architecture—one that is more efficient, inclusive, and programmable.

For investors, builders, and institutions alike, the message is clear:

The future of finance will not be built on legacy systems—it will be engineered through intelligence and decentralized infrastructure.