Key Takeaways :

- The proposed Digital Asset PARITY Act aims to fundamentally reshape crypto taxation in the United States.

- Bitcoin and other digital assets may soon fall under wash sale rules, eliminating a major tax optimization strategy.

- At the same time, regulated stablecoin payments could become effectively tax-free under certain conditions.

- Policymakers are signaling a shift from crypto as a speculative asset to crypto as a payment infrastructure.

- The bill could accelerate adoption of stablecoins while reducing short-term trading incentives.

Introduction: A Turning Point in Crypto Taxation

The cryptocurrency market has long existed in a gray area of tax policy, benefiting from regulatory gaps that traditional financial assets could not exploit. One of the most prominent examples is the absence of wash sale rules for digital assets such as Bitcoin.

Now, that era may be coming to an end.

A new bipartisan proposal in the United States Congress—the Digital Asset PARITY Act—seeks to close these loopholes while simultaneously promoting the use of stablecoins for payments. This dual approach marks a critical inflection point in how governments view digital assets: not merely as speculative instruments, but as infrastructure for real-world financial systems.

This shift has profound implications for investors, developers, exchanges, and financial institutions worldwide.

Section 1: What Is the Digital Asset PARITY Act?

The proposed legislation, introduced by Steven Horsford and Max Miller, aims to align the tax treatment of digital assets with traditional financial instruments.

At its core, the bill proposes to amend Section 1091 of the Internal Revenue Code, which governs wash sale rules.

Historically, wash sale rules prevent investors from claiming a tax loss if they sell a security at a loss and repurchase it within a short timeframe. However, cryptocurrencies have not been classified as “securities,” allowing traders to exploit this loophole.

The PARITY Act would redefine digital assets as “specified assets,” thereby subjecting them to these same restrictions.

This means that strategies commonly used by crypto traders—such as selling Bitcoin at a loss and immediately buying it back to reduce taxable income—would no longer be allowed.

Section 2: The End of Wash Sales in Crypto Markets

Wash Sale Mechanism (Before vs After Regulation)

The elimination of wash sale loopholes represents one of the most significant structural changes to crypto trading behavior.

Previously, investors could:

- Sell Bitcoin at a loss

- Immediately repurchase it

- Claim the loss to offset gains elsewhere

This strategy, known as tax-loss harvesting, has been widely used in both retail and institutional portfolios.

Under the new framework, such actions would be disallowed if repurchase occurs within a restricted period. Furthermore, the regulation is expected to extend beyond spot trading to include:

- Options

- Futures

- Forward contracts

- Short positions

This comprehensive coverage ensures that traders cannot bypass the rules through derivatives.

The immediate consequence is a reduction in short-term speculative strategies and increased friction in portfolio rebalancing.

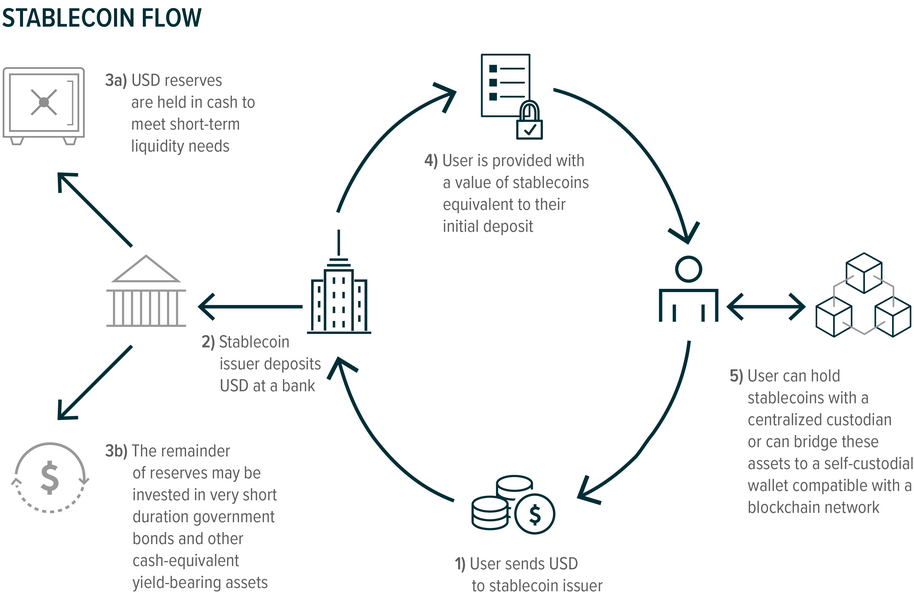

Section 3: Stablecoins as Tax-Free Payment Instruments

Stablecoin Payment Flow

While the bill tightens rules on speculative trading, it introduces a powerful incentive on the utility side.

Under the proposed framework, certain regulated payment stablecoins—pegged 1:1 to the US dollar—would be exempt from capital gains taxation when used for transactions within a narrow price band (approximately $0.99–$1.01).

This effectively removes the tax burden associated with everyday crypto payments, a long-standing barrier to adoption.

For example:

- Paying $50 using a stablecoin would not trigger a taxable event

- Minor fluctuations in price would be ignored for tax purposes

Additionally, lawmakers are considering a de minimis exemption for transactions under $200, further simplifying small payments.

This approach signals a clear policy direction: encourage digital dollars for commerce while discouraging speculative tax manipulation.

Section 4: Market Implications — From Speculation to Utility

The broader implication of this legislation is a paradigm shift in the crypto economy.

Currently, the stablecoin market exceeds approximately $316 billion, yet nearly 99% of its activity remains tied to trading rather than real-world payments.

By removing tax friction for payments, the bill could catalyze:

- Merchant adoption of blockchain-based payments

- Growth in on-chain commerce

- Integration with fintech and remittance systems

This aligns with trends seen in companies like Visa and PayPal, both of which have expanded their stablecoin and blockchain payment capabilities.

For emerging markets and remittance corridors, the implications are even more significant. Stablecoins could become a core settlement layer, reducing costs and increasing transaction speed.

Section 5: Risks and Concerns for Investors

Despite its potential benefits, the legislation has sparked concern among market participants.

One major issue is the loss of tax efficiency tools for investors. Without wash sale strategies, portfolio management becomes less flexible, particularly during volatile markets.

At the same time, the transition to a payment-focused ecosystem is not yet fully developed.

This creates a potential “worst-case scenario”:

- Investors lose tax advantages

- Payment infrastructure remains immature

- Market liquidity declines in the short term

Additionally, there are concerns about regulatory overreach and the complexity of implementation, particularly for decentralized finance (DeFi) platforms.

Section 6: Global Context and Emerging Trends

The United States is not alone in rethinking crypto taxation.

Countries such as the UK, Japan, and members of the EU are also tightening reporting requirements and closing tax loopholes. At the same time, many jurisdictions are exploring central bank digital currencies (CBDCs) and regulated stablecoins.

This convergence suggests a global trend:

- Increased compliance requirements

- Reduced tolerance for speculative arbitrage

- Greater emphasis on real-world utility

From an investment perspective, this means the next wave of opportunities may lie not in short-term trading, but in infrastructure:

- Payment rails

- Stablecoin ecosystems

- Compliance and analytics tools

- Cross-border settlement platforms

Section 7: Strategic Outlook for Crypto Investors and Builders

For readers seeking new revenue opportunities and practical blockchain applications, the implications are clear.

The market is evolving toward a dual structure:

- Regulated utility layer (stablecoins, payments, enterprise use)

- Constrained speculative layer (Bitcoin, altcoins under stricter tax rules)

This aligns with your previously defined framework of:

- Asset-backed representation

- Autonomous trust systems

Investors should consider:

- Exposure to stablecoin infrastructure projects

- Companies enabling compliance and tax reporting

- Payment-focused blockchain applications

Meanwhile, developers and entrepreneurs should focus on:

- UX for seamless stablecoin payments

- Integration with traditional financial systems

- Regulatory-first product design

Conclusion: A Structural Shift, Not Just a Tax Change

The Digital Asset PARITY Act is more than a tax reform proposal—it is a strategic blueprint for the future of digital finance.

By closing loopholes like wash sales and incentivizing stablecoin payments, regulators are attempting to reshape the crypto market into a more sustainable and utility-driven ecosystem.

For investors, this means adapting strategies away from short-term arbitrage and toward long-term value creation.

For builders, it signals a clear direction: the future of crypto lies not just in price speculation, but in real-world financial integration.