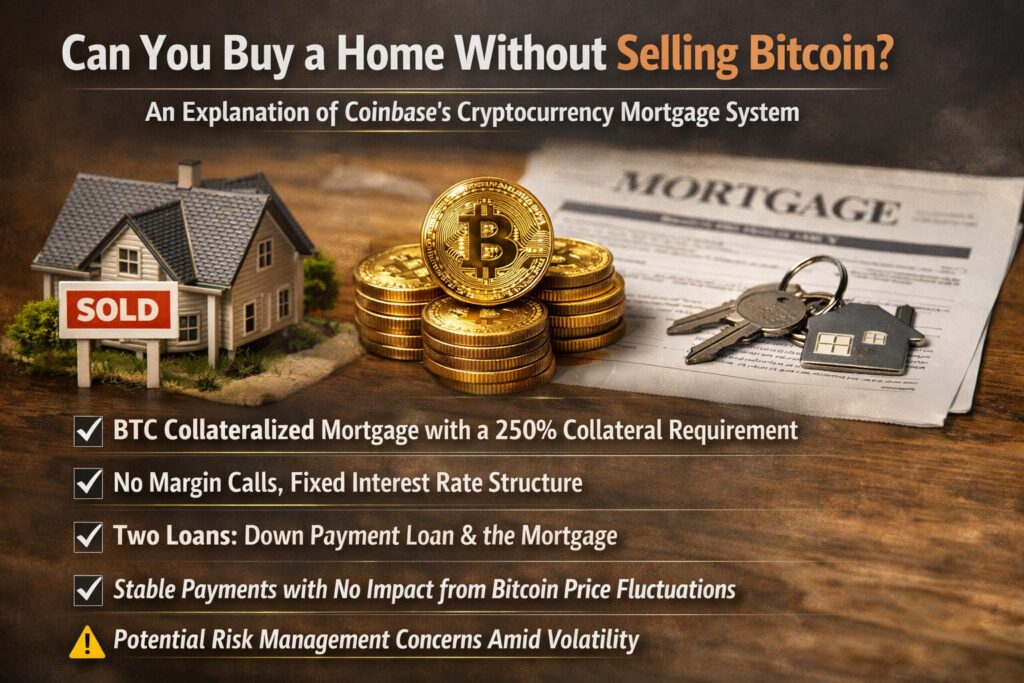

Main Points :

- BTC Collateralized Mortgage with a 250% Collateral Requirement

- No Margin Calls, Fixed Interest Rate Structure

- Combination of Two Loans: A Down Payment Loan and the Mortgage

- Stable Payments with No Impact from Bitcoin Price Fluctuations

- Potential Risk Management Concerns Amid Volatility

In late March 2026, Coinbase launched a new mortgage service that allows users to use their Bitcoin (BTC) or USDC as collateral for a home loan. This novel service, developed in partnership with Better Home & Finance, offers a solution for crypto holders to leverage their assets without needing to sell them. With backing from U.S. government-sponsored enterprise Fannie Mae, Coinbase’s product is designed to provide a stable financial option in the volatile world of cryptocurrencies. But how does this mortgage system work, and what are its potential implications for both crypto investors and the traditional housing market?

How the Cryptocurrency-Backed Mortgage Works

At its core, the new Coinbase mortgage system combines two types of loans to create a flexible and predictable financial product. Borrowers use their BTC or USDC from their Coinbase account as collateral, which allows them to access a down payment loan. The down payment loan and the primary mortgage are both set at the same interest rate and repayment period, with the borrower making a single monthly payment for both loans.

For example, consider a home purchase worth $500,000. The borrower would place $250,000 worth of BTC as collateral and receive a down payment loan of $100,000. The BTC collateral must exceed the down payment by 250%, meaning that the collateral’s initial value needs to be significantly higher than the loan amount.

No Margin Calls or Forced Liquidations

One of the most innovative aspects of this mortgage is that it does not include margin calls (also known as “margin calls”). Traditional cryptocurrency-backed loans often require continuous monitoring of collateral value, and if the value of the crypto asset declines, borrowers may face immediate liquidation or forced sales to cover the loan’s value. However, Coinbase’s system is different.

Once the loan is in place, the terms are completely fixed—there is no need for adjustments or recalculations based on Bitcoin’s price movements. The monthly payments, the interest rate, and the repayment schedule are all set, and they will not change even if Bitcoin’s value fluctuates drastically.

Stability in an Unstable Market

For a traditional mortgage, there are risks such as fluctuating interest rates, housing market downturns, or changes in the borrower’s financial situation. With Coinbase’s crypto-backed mortgage, the risk shifts from market price fluctuations to the borrower’s ability to make timely payments.

If the price of Bitcoin plummets, the loan terms remain unaffected as long as the borrower continues making payments on time. The borrower will not face a forced liquidation of their collateral unless there is a default due to missed payments for 60 days or more. In this case, the process would follow the standard legal procedure for delinquent loans, much like traditional mortgages.

Furthermore, the BTC used as collateral will be held in a Coinbase Prime account and cannot be sold or traded during the loan’s life, ensuring that the crypto assets are secure and untouched until the mortgage is paid off.

Opportunities for Homebuyers in the Crypto World

The U.S. housing market has seen significant price increases in recent years, with middle-income households spending as much as 36% of their income on mortgage repayments. For low-income families, this number can rise to 71%. This has made homeownership increasingly difficult, especially for young people with limited cash savings. Coinbase’s new service targets this demographic, offering an opportunity for cryptocurrency holders to use their digital assets as a pathway to homeownership without needing to sell their Bitcoin.

Coinbase also offers a benefit for its members, those enrolled in its “Coinbase One” membership program. These members can receive a closing cost credit of up to 1% of the loan amount (capped at $10,000) when using Better to secure the mortgage. Additionally, borrowers who use USDC as collateral will continue to earn USDC rewards during the mortgage period, helping offset some of the monthly repayment costs.

Regulatory Concerns and Market Implications

While this service represents a new frontier for cryptocurrency integration into traditional financial systems, it also raises potential concerns about systemic risks. The most significant risk is tied to the volatile nature of cryptocurrency prices. If Bitcoin’s price experiences a sharp decline, the collateral value could significantly decrease, potentially putting lenders at risk.

Moreover, as cryptocurrency adoption grows, more people may look to use digital assets for home purchases, which could disrupt the stability of the housing market. Regulators and market participants are already discussing how to address these risks, with an eye toward establishing clearer risk management frameworks for crypto-backed lending.

Conclusion: A New Path for Crypto Investors?

Coinbase’s innovative cryptocurrency mortgage system offers a new financial pathway for crypto holders who want to access real estate markets without having to sell their assets. The system’s fixed terms, lack of margin calls, and the ability to leverage digital assets in a stable manner provide a unique alternative to traditional mortgage routes.

However, as with any emerging financial product, regulatory scrutiny and long-term market effects need careful attention. As more crypto holders seek ways to turn their digital assets into tangible investments, services like Coinbase’s mortgage could pave the way for a new era of homeownership, where cryptocurrency plays a central role in bridging the gap between digital and real-world assets.