Main Points :

- Minnesota lawmakers are considering a full ban on crypto ATMs through bill HF 3642.

- Over 70 scam cases and more than $540,000 in losses were reported in 2025 alone.

- 86% of reported losses nationwide (2024 FBI data) involved victims aged 60 or older.

- Industry operators argue that stricter regulation—not prohibition—is the solution.

- The debate reflects a broader global shift toward stronger consumer protection in crypto access points.

- Investors and blockchain builders must rethink the role of physical crypto infrastructure in the next cycle.

1. Minnesota’s Proposed Ban: A Radical Shift in Crypto Access Policy

On February 26, the Minnesota House of Representatives reviewed bill HF 3642, which proposes a complete ban on cryptocurrency ATMs (also referred to as crypto kiosks) across the state. Introduced by Representative Erin Koegel of the Democratic–Farmer–Labor Party, the bill would prohibit the installation and operation of any physical terminal that allows users to purchase cryptocurrency instantly using cash or debit cards. Online crypto transactions would remain unaffected.

This proposal represents a dramatic escalation from Minnesota’s previous regulatory approach. In 2024, the state enacted consumer protection measures that included:

- A $2,000 daily transaction cap for new users

- A 72-hour cooling-off period

- Mandatory refund mechanisms for scam victims

Despite these measures, lawmakers now argue that fraudsters have easily circumvented the rules. Criminals reportedly instruct victims to split payments into smaller deposits, effectively bypassing transaction limits and cooling-off protections.

Minnesota currently has approximately 350 licensed crypto ATMs operated by 8 to 10 companies. If HF 3642 passes, all would be removed.

2. The Data Behind the Crackdown

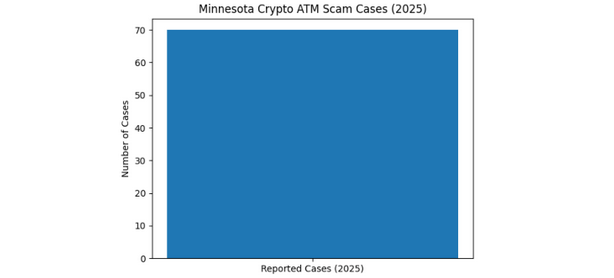

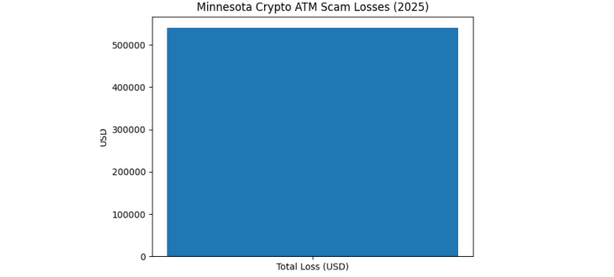

In 2025 alone, more than 70 crypto ATM-related scam incidents were reported to Minnesota’s Department of Commerce, totaling over $540,000 in losses.

[Minnesota Crypto ATM Scam Cases (2025)]

[Minnesota Crypto ATM Scam Losses (2025)]

While roughly 48% of victims received partial refunds, the total amount recovered represented only 16% of overall losses.

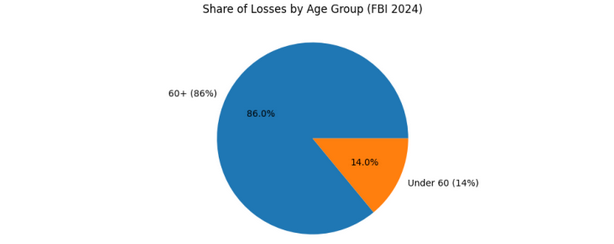

Nationally, the pattern is even more alarming. According to the FBI’s 2024 Internet Crime Report, when age was identified, individuals aged 60 and older accounted for 86% of total reported crypto fraud losses.

[Share of Losses by Age Group (FBI 2024)]

The numbers highlight a structural vulnerability: crypto ATMs serve as frictionless bridges between traditional cash economies and irreversible blockchain transfers. For scammers, this is ideal.

3. Why Elderly Victims Are Being Targeted

Testimonies presented during the committee hearing revealed devastating cases. A detective from Woodbury described a low-income elderly resident who conducted at least 10 Bitcoin transactions over six months, transferring approximately 50% of her monthly income to scammers. The situation deteriorated to the point where adult protective services had to intervene.

Another case in St. Cloud involved a 78-year-old woman who lost $80,000. The funds were transferred to overseas wallets, making recovery nearly impossible.

Fraudsters increasingly direct victims away from traditional banking channels and toward crypto ATMs. The process is fast, anonymous, and irreversible. For elderly individuals unfamiliar with blockchain mechanics, the damage can occur within minutes.

Faribault’s police chief estimated that since 2022, local residents have lost over $500,000 to crypto ATM scams—likely only 25% of actual losses due to underreporting.

The average victim age there is 68.

This data has intensified political pressure. The city of St. Paul has already enacted its own crypto kiosk ban, which took effect in December of last year.

4. Industry Pushback: Regulation Instead of Prohibition

CoinFlip, a major digital currency platform operating 50 kiosks in Minnesota, submitted testimony opposing the blanket ban.

The company argues:

- ATM operators are not the perpetrators.

- Crypto ATMs are not the only fraud vector.

- Overregulation may push users toward unregulated peer-to-peer channels.

- Less than 1% of their 12,000 annual transactions resulted in refund requests.

CoinFlip proposes alternatives:

- Mandatory refunds for all verified scam victims

- Extended cooling-off periods before transaction finality

- Enhanced KYC and monitoring standards

- Stronger warning systems and transaction flags

Their legal counsel stated that banning a legitimate product because fraud occurs sets a dangerous precedent.

5. Broader U.S. and Global Trends

Minnesota is not alone in tightening crypto access regulations.

Across the United States:

- Several states are increasing licensing requirements for kiosk operators.

- The federal government is strengthening AML enforcement under FinCEN.

- The SEC and CFTC continue expanding jurisdictional oversight.

- Consumer protection agencies are targeting misleading crypto advertising.

Internationally:

- The United Kingdom is increasing restrictions on physical crypto machines.

- The European Union’s MiCA framework strengthens compliance obligations.

- Japan maintains strict exchange registration standards.

- Singapore enforces stringent AML/KYC requirements.

The direction is clear: physical on-ramps are becoming regulatory pressure points.

6. What This Means for Investors Seeking New Opportunities

For readers seeking new crypto assets and revenue opportunities, this development signals three key structural shifts:

A. Physical Infrastructure Risk Premium

Companies operating crypto ATMs now carry significant regulatory risk. Investors must factor in potential bans or strict compliance costs.

B. Rise of Regulated On-Ramps

Expect growth in compliant digital onboarding platforms, bank-integrated crypto services, and licensed VASP infrastructures.

Stablecoin settlement layers and regulated custodial solutions may benefit from reduced reliance on anonymous kiosks.

C. Increased Demand for Fraud-Resistant Design

Projects focusing on:

- Transaction reversibility layers

- Delayed settlement smart contracts

- AI-based scam detection

- Behavioral transaction analysis

may see increased adoption.

Blockchain builders should consider integrating protective mechanisms directly into wallet UX, especially for vulnerable demographics.

7. Practical Blockchain Implications

From a practical standpoint, crypto ATMs represent a first-generation adoption model. They provided accessibility but lacked embedded safeguards.

The next phase of blockchain infrastructure will likely emphasize:

- Embedded compliance

- Real-time fraud analytics

- Identity-linked transaction scoring

- Institutional-grade custody

Developers building non-custodial systems must also address social engineering risks—not just technical security.

8. Conclusion: A Defining Moment for Physical Crypto Access

Minnesota’s proposed ban on crypto ATMs is more than a local policy debate—it is a signal of regulatory recalibration.

Lawmakers argue that consumer protection measures have failed. Industry operators argue that prohibition overreaches. Both sides acknowledge a core truth: crypto ATMs have become a high-risk access point for vulnerable populations.

For investors and blockchain entrepreneurs, this moment demands strategic clarity.

The future of crypto infrastructure will not be defined solely by decentralization or innovation. It will be defined by trust architecture, regulatory adaptability, and fraud resilience.

Those who build compliant, user-protective systems will capture the next wave of sustainable growth.

The era of frictionless anonymous cash-to-crypto machines may be closing. The era of intelligent, regulated blockchain finance is beginning.