Main Points :

- Japan’s MoneyX 2026 conference positioned stablecoins, CBDCs, and tokenized deposits as complementary layers of a new “Currency OS.”

- JPYC reported rapid growth, aiming for AI-native programmable money interoperable with global standards such as USDC.

- DCP (DeCurret DCP) emphasized corporate treasury automation and on-chain settlement integration, including cross-border rails.

- Japan’s Ministry of Finance framed CBDCs as a public backstop for “payment gap zones.”

- Progmat stressed interoperability standards akin to TCP/IP for digital money networks.

- Global trends show increasing convergence between regulated stablecoins, central bank initiatives, and tokenized bank liabilities.

- The next wave of opportunity lies in AI agents, automated FX, programmable B2B finance, and infrastructure-layer protocols.

1. A “Connected Money Paradigm”: Reimagining the Currency Stack

On February 27, 2026, at The Prince Park Tower Tokyo, the next-generation finance conference “MoneyX 2026” convened regulators, stablecoin issuers, tokenization platforms, and financial infrastructure developers to debate what many described as a “New OS of Money.”

The session titled “Connected Money Paradigm” addressed a fundamental question: Can three forms of digital money—stablecoins, tokenized bank deposits, and central bank digital currencies (CBDCs)—coexist within a unified economic framework?

Rather than positioning these as rivals, speakers described them as complementary modules in a layered financial architecture.

This reframing is crucial. For years, debate around digital currency has been binary—private versus public, decentralized versus centralized. But MoneyX 2026 suggested something more pragmatic: interoperability over ideological purity.

For investors and builders searching for new revenue streams and practical blockchain use cases, this shift signals opportunity not in competition, but in integration.

2. JPYC’s Growth: Toward AI-Native Programmable Money

Noritaka Okabe, CEO of JPYC, reported that the cumulative issuance of the company’s Japanese yen stablecoin has reached approximately ¥1.3–1.4 billion (approximately $9–10 million at current exchange rates). Monthly growth has averaged 69%, with approximately 81,000 holders and an average purchase size of about ¥110,000 (approximately $750).

Beyond growth metrics, Okabe highlighted JPYC’s Series B first close, bringing total capital raised to approximately ¥1.78 billion (approximately $12 million). Investors include institutional players such as Central Bank Capital and Meiji Yasuda Life.

But the most compelling vision is strategic rather than financial:

“Money usable not only by humans, but also by AI agents and robots.”

JPYC aims to issue programmable money on public blockchains, compatible with USDC standards, enabling foreign tourists without Japanese bank accounts—and even autonomous AI systems—to transact seamlessly.

In the medium to long term, JPYC intends to expand into on-chain foreign exchange (FX), working with Circle to enable AI-driven automated FX trading.

Strategic Implication

The convergence of stablecoins and AI agents introduces a new category of demand:

- Machine-to-machine (M2M) payments

- Autonomous treasury management

- AI-native cross-border arbitrage

This is not merely fintech innovation—it is financial infrastructure for non-human economic actors.

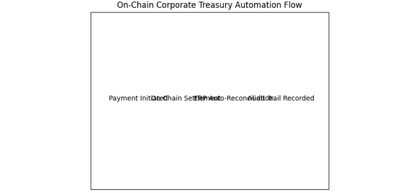

3. Corporate Treasury Automation: DCP’s On-Chain Vision

Keisei Hirako of DCP (DeCurret DCP) pointed to inefficiencies in corporate payment management. Current systems rely heavily on:

- Transaction passwords

- Dual manual approvals

- Manual data entry into ERP/accounting systems

DCP’s proposal: automate the entire flow on-chain—from transfer initiation to accounting reconciliation.

In this architecture:

- A payment is executed on-chain.

- Metadata is embedded.

- ERP entries reconcile automatically.

- Audit trails become cryptographically verifiable.

This vision moves blockchain beyond speculative trading into enterprise-grade financial plumbing.

DCP has also partnered with Singapore-based Palpeo to explore on-chain conversion of SWIFT-based international transfers.

Revenue Implications

For investors and builders:

- B2B programmable payment rails

- API-based treasury automation services

- Compliance-as-a-service modules

- Real-time liquidity optimization engines

The real value may not be in retail speculation—but in enterprise middleware.

4. CBDCs as a Public Safety Net: The Ministry’s Position

Junichiro Hatogai from Japan’s Ministry of Finance articulated a public-sector perspective on CBDCs.

He framed CBDCs not as competitors to private stablecoins, but as safety nets for “payment gap zones”—areas or demographics underserved by private actors.

Importantly, he noted that even in urban areas, digital literacy divides can exclude individuals from financial participation.

“People are connected to society through the act of payment.”

From this viewpoint, CBDCs ensure universal access.

He described the government’s role metaphorically as “preparing the soil and nutrients” so that private ecosystems can flourish.

Macro Insight

Globally:

- The European Central Bank is advancing the digital euro.

- China’s e-CNY continues pilot expansion.

- The Federal Reserve remains cautious but active in research.

CBDCs may not dominate retail use—but they anchor monetary sovereignty and systemic resilience.

For market participants, this suggests a dual system:

- Public money as base layer trust anchor

- Private programmable layers as innovation engines

5. Interoperability: The TCP/IP Moment of Digital Money

Tatsuya Saito of Progmat emphasized interoperability across networks.

His analogy was powerful: digital money needs a trustless protocol equivalent to TCP/IP.

Without standardization, ecosystems fragment. With it, capital flows seamlessly across:

- Stablecoins

- Tokenized deposits

- CBDCs

- Cross-chain infrastructures

This is arguably the most critical infrastructure opportunity.

Builders who define interoperability standards may shape the monetary internet.

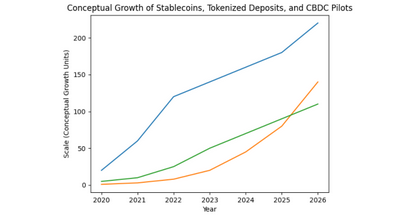

Graph Title: Comparative Growth Trajectories: Stablecoins vs Tokenized Deposits vs CBDC Pilots

- X-axis: Year (2020–2026)

- Y-axis: Market Value ($)

- Three curves representing global stablecoin market cap, tokenized bank deposits issuance, and number of CBDC pilot jurisdictions

(Provide visual line graph with clear legend and $-denominated scales.)

6. Global Context: Convergence Is Accelerating

Recent trends worldwide reinforce the MoneyX thesis:

- U.S. regulators are clarifying stablecoin reserve frameworks.

- Banks are experimenting with tokenized deposits for settlement efficiency.

- Cross-border corridors are increasingly blockchain-enabled.

The debate is shifting from “Should blockchain replace banking?” to:

“How do we integrate programmable money into regulated finance?”

For yield-seeking investors, attention should turn toward:

- Regulated yield-bearing stablecoins

- Tokenized treasury instruments

- On-chain repo markets

- AI-powered FX liquidity routing

The alpha may be infrastructure-layer positioning, not just token price appreciation.

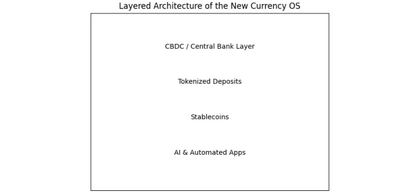

Graph Title: The Layered Architecture of the New Currency OS

Visual stack diagram:

Layer 1: Central Bank Money (CBDC / Reserves)

Layer 2: Tokenized Bank Deposits

Layer 3: Regulated Stablecoins

Layer 4: AI Agents & Automated Financial Applications

Use clear labeling and arrows showing interoperability between layers.

7. Investment and Builder Opportunities

The MoneyX 2026 discussion signals several practical opportunities:

1. AI-Payable Stablecoins

Design tokens optimized for machine-initiated microtransactions.

2. On-Chain FX Markets

Automated liquidity routing across regulated stablecoins.

3. Compliance Infrastructure

Programmable KYC/AML modules embedded into token logic.

4. Enterprise Treasury Middleware

APIs bridging ERP systems and on-chain rails.

5. Interoperability Protocols

Cross-chain messaging standards and settlement layers.

The next cycle’s winners may not be meme coins—but monetary middleware.

Conclusion: Coexistence as Competitive Advantage

MoneyX 2026 reframed digital currency discourse.

Stablecoins, tokenized deposits, and CBDCs are not mutually exclusive. They are components of a modular monetary operating system.

Public institutions provide stability.

Private actors deliver innovation.

Infrastructure developers enable interoperability.

For investors, the opportunity lies not in choosing one side—but in positioning at the intersection.

The “New OS of Money” is not a replacement of finance—it is its upgrade.