Main Points :

- Bitcoin fell back below the psychological $70,000 level amid renewed U.S. policy uncertainty.

- The U.S. Supreme Court’s ruling against tariff overreach reignited fears of an escalating trade conflict.

- The stalled U.S. crypto market structure “Clarity Bill” has heightened regulatory ambiguity.

- Options markets show a sharp rise in short-term put demand, signaling near-term event risk hedging.

- AI-related systemic risk narratives are spreading across macro markets, pressuring risk assets broadly.

- Despite the drop, futures-spot spreads remain orderly, suggesting a healthy deleveraging rather than a liquidity crisis.

- Key upcoming events (housing data, legislative deadlines, fintech conferences) may define the next phase.

1. A Return Below $70,000: What Happened?

Bitcoin has once again slipped below the psychological $70,000 threshold, a level it had managed to reclaim earlier in the month. The decline unfolded between February 23 and 24, driven not by internal crypto-specific stress, but by a confluence of macro and policy uncertainties emerging from the United States.

In USD terms, the move represents a break below a key psychological and technical support zone. While the exact low fluctuated intraday, market participants broadly observed that Bitcoin traded back into the mid-to-high $60,000 range during peak selling pressure.

Importantly, this was not an isolated crypto event. U.S. equities, particularly technology-heavy indices, also experienced broad-based declines. The move reflects a classic “risk-off” episode, where investors rotate away from volatile assets amid heightened uncertainty.

For readers seeking new crypto opportunities or yield strategies, it is crucial to distinguish between structural breakdowns and cyclical corrections. Current data suggests the latter.

2. Tariff Shockwaves: Supreme Court Ruling and Political Retaliation

A major catalyst behind the renewed volatility was a U.S. Supreme Court decision that deemed certain executive tariff measures to be an overreach of authority. While the ruling was legally technical, the political reaction was not.

Former President Donald Trump and allied political figures signaled strong opposition via public statements and social media, raising concerns that tariff policies could return aggressively if political control shifts. Markets interpreted this as a revival of trade war risk.

Historically, tariff escalations have led to:

- Increased global supply chain uncertainty

- Stronger USD volatility

- Equity drawdowns in export-sensitive sectors

- Capital flight into defensive positioning

Bitcoin’s response to tariff risk has been complex over time. In some historical instances, BTC benefited from geopolitical uncertainty as a “non-sovereign hedge.” However, in the current macro regime, Bitcoin is behaving more like a high-beta tech asset rather than a digital gold proxy.

This suggests that institutional flows are currently driving price behavior more than ideological narratives.

3. The Clarity Bill Stalemate: Regulatory Ambiguity Persists

Another major pressure point is the ongoing uncertainty surrounding the U.S. crypto market structure legislation, commonly referred to as the “Clarity Bill.” The White House has set March 1 as a negotiation deadline, yet consensus remains elusive.

The bill aims to define:

- Jurisdictional boundaries between the SEC and CFTC

- Stablecoin issuance frameworks

- Token classification standards

- Custody and exchange compliance structures

For institutional capital allocators, regulatory clarity is not optional—it is foundational. The absence of clear legal frameworks creates valuation discounts.

Until there is a definitive resolution, Bitcoin and broader crypto markets may remain sensitive to headline risk.

4. Market Microstructure: A Healthy Correction?

Despite the sharp price decline, derivatives data suggests that this is not a systemic crisis.

Spot-Led Selling

Order flow analysis indicates that the decline was primarily driven by spot market selling rather than cascading futures liquidations.

Futures Basis Stable

The spread between futures and spot prices remains within normal ranges. There is no significant backwardation or abnormal funding stress.

This implies:

- No liquidity crunch

- No funding freeze

- No major leverage wipeout

Such characteristics point to a controlled deleveraging phase rather than a structural breakdown.

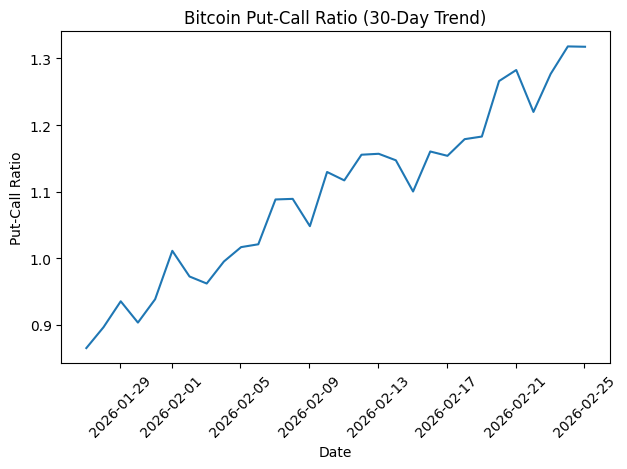

5. Options Market Signals: Short-Term Fear Spikes

Where sentiment deterioration is most visible is in the options market.

The Put-Call Ratio (PCR) has risen noticeably, particularly in near-dated expiries. Traders are aggressively purchasing short-term puts.

This behavior signals:

- Event-driven hedging

- Fear of sudden downside shocks

- Heightened awareness of policy deadlines

[Bitcoin Put-Call Ratio (Last 30 Days)]

Short-dated put accumulation typically reflects short-term uncertainty rather than long-term structural bearishness. It often precedes volatility compression once events pass.

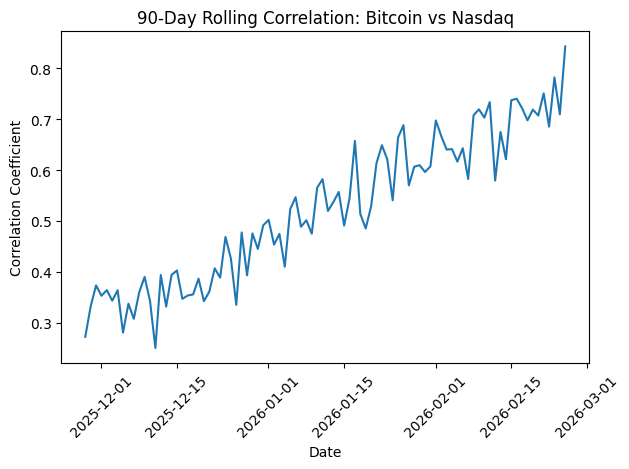

6. AI Tail Risk Narrative: The “2028 Global Intelligence Crisis”

Beyond tariffs and crypto regulation, a more abstract but powerful narrative is emerging: AI-driven systemic disruption.

A recent analytical report discussing a potential “2028 Global Intelligence Crisis” has gained traction. The report outlines scenarios where rapid AI deployment could:

- Displace significant labor segments

- Compress corporate profit margins

- Trigger credit stress in leveraged industries

- Force abrupt macroeconomic realignments

Arthur Hayes has similarly warned that AI-driven liquidity shocks could create financial instability, framing Bitcoin as a “liquidity fire alarm.”

Yet paradoxically, in the short term, AI fear has led to risk-off behavior across equities and crypto alike.

[Correlation Between Nasdaq and Bitcoin (90-Day Rolling)]

The correlation underscores that Bitcoin is currently embedded in the broader risk asset complex.

7. Key Upcoming Catalysts

The market now turns its attention to several critical dates:

- February 24: S&P Case-Shiller Home Price Index (20-city)

- March 1: Clarity Bill negotiation deadline

- March 3–6: FIN/SUM fintech conference in Japan

The housing data will provide insight into U.S. consumer strength. If housing softens materially, recession probabilities may rise, intensifying risk-off flows.

The Clarity Bill deadline could produce a relief rally if compromise emerges.

The FIN/SUM event may influence Asian fintech sentiment and cross-border crypto adoption narratives.

8. Strategic Implications for Crypto Investors

For those searching for new crypto assets or yield opportunities, this environment demands strategic nuance.

Short-Term

- Expect elevated volatility.

- Hedging via options may remain expensive but justified.

- Spot accumulation strategies should consider macro event timing.

Medium-Term

If regulatory clarity improves and tariff tensions subside, Bitcoin could reassert its structural uptrend, especially if ETF inflows resume.

Long-Term

AI-driven economic restructuring could ultimately strengthen the Bitcoin thesis as a neutral settlement layer—particularly if trust in traditional financial intermediaries erodes.

However, the transition may be turbulent.

9. Conclusion: Risk Asset for Now, Structural Hedge Later?

At present, Bitcoin is being treated as a risk asset, not a safe haven. Policy ambiguity, revived tariff tensions, and AI tail-risk narratives are converging to create macro uncertainty.

Yet the correction appears orderly. There is no liquidity crisis, no derivatives meltdown, and no systemic leverage implosion.

For disciplined investors, such phases often represent recalibration rather than collapse.

The coming weeks—especially the regulatory deadline—will likely determine whether Bitcoin stabilizes and rebounds or extends its correction.

In volatile markets, clarity is capital.