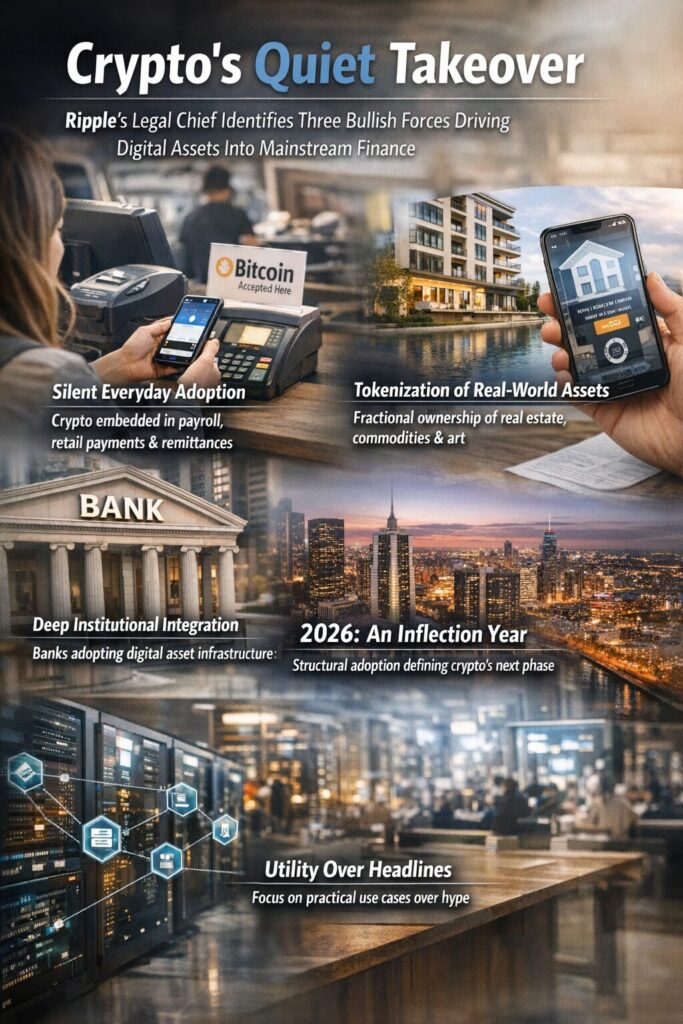

Silent Everyday Adoption: Crypto is increasingly embedded in payroll services, retail payments, creator platforms, and remittances—often without users consciously recognizing it.

Tokenization of Real-World Assets (RWA): Fractional ownership lowers barriers to entry, enabling access to real estate, commodities, and art at lower capital thresholds.

Deep Institutional Integration: Banks and traditional financial institutions are integrating digital asset infrastructure into existing systems.

2026 as an Inflection Year: Structural adoption—not speculative hype—could define the next phase of crypto expansion.

Utility Over Headlines: The shift toward practical use cases marks a transition from volatility-driven narratives to infrastructure-driven growth.

The Quiet March of Crypto Into Mainstream Finance

When crypto first emerged, it was defined by volatility, ideological debates, and headline-grabbing price swings. Today, however, a more subtle transformation is unfolding. According to Stuart Alderoty, Chief Legal Officer of Ripple and President of the National Cryptocurrency Association, the real story is not explosive growth but quiet normalization.

In a January 27 opinion piece published by Fast Company, Alderoty argues that crypto is no longer fighting for legitimacy—it is gradually embedding itself into the structural layers of finance and daily life. The turning point, he suggests, may not feel dramatic. Instead, it will feel ordinary.

“When the tipping point arrives, it may not feel dramatic. It will feel normal. And that’s the point.”

For investors seeking new revenue sources or practical blockchain applications, this framing is crucial. The next growth wave may not come from speculative mania, but from invisible infrastructure.

I. Silent Everyday Adoption: Crypto as Background Utility

From Headlines to Infrastructure

The first bullish force identified by Alderoty is what he calls “quiet adoption.” Crypto usage is expanding in ways that no longer require retail traders to check charts daily.

Instead, digital assets are being integrated into:

Payroll disbursement systems

Cross-border remittances

Retail payment gateways

Creator monetization platforms

Micropayment ecosystems

This trajectory mirrors the rise of mobile payments. Early adopters were tech enthusiasts; today, billions use mobile wallets without considering the underlying rails.

Similarly, blockchain networks such as the XRP Ledger increasingly function as settlement layers beneath user-facing platforms.

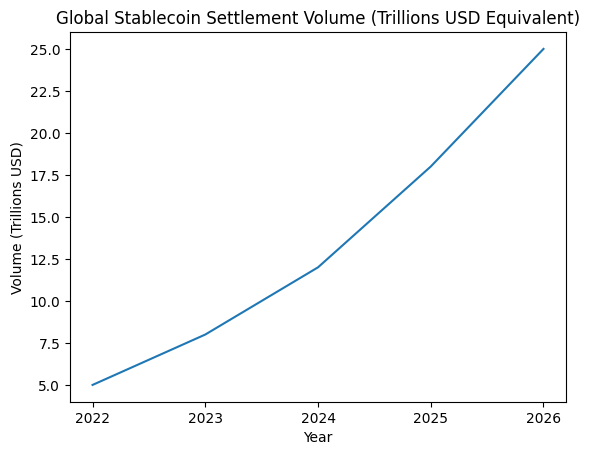

Market Context (2024–2026 Trends)

Recent global trends support this thesis:

Cross-border settlement using blockchain reduces transfer times from days to seconds.

Stablecoin transaction volumes have surpassed trillions annually.

Payroll providers are experimenting with hybrid fiat-crypto settlement models.

Remittance corridors in Asia, Latin America, and Africa increasingly utilize blockchain liquidity rails.

Importantly, these developments are often denominated in dollars. For example:

Cross-border remittance costs average 6–7% traditionally, while blockchain-based settlement can reduce effective costs significantly.

Silent adoption is structurally bullish because it reduces reliance on speculative cycles. Infrastructure usage tends to:

Increase network resilience

Improve liquidity depth

Attract regulatory clarity

Encourage institutional confidence

The absence of hype may, paradoxically, signal maturity.

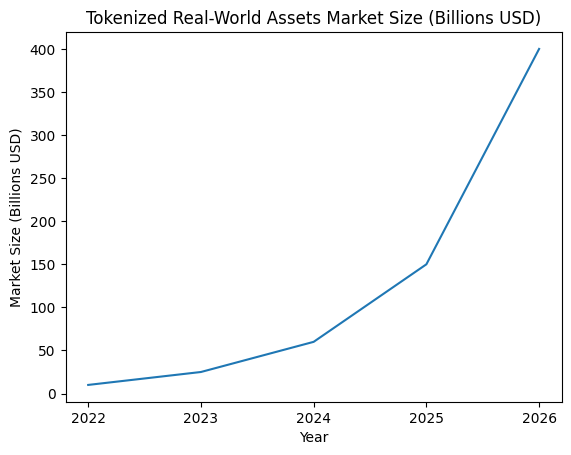

II. Tokenization: Unlocking Real-World Assets Through Fractional Ownership

Lowering Barriers to Entry

Alderoty’s second bullish driver is tokenization—the digitization of real-world assets (RWA) into blockchain-based representations.

He notes:

“Many people couldn’t own certain assets because the entry cost was too high. Tokenization breaks that barrier.”

Traditionally, access to high-value assets required significant capital:

Commercial real estate: often $500,000+ minimum exposure

Fine art: millions of dollars

Commodity storage: institutional thresholds

Tokenization allows these assets to be divided into fractions valued in dollars, sometimes as low as $10 or $100.

Structural Shifts in Capital Markets

Tokenization is not theoretical. Institutions are actively piloting:

Tokenized Treasury bills (denominated in USD)

Real estate fractionalization platforms

Commodity-backed digital tokens

Private credit digitization

By converting assets into programmable digital units, markets gain:

24/7 liquidity

Instant settlement

Transparent ownership tracking

Reduced administrative friction

Financial Implications

From an investment perspective, tokenization:

Democratizes access

Expands global capital participation

Creates new secondary markets

Introduces programmable yield mechanisms

For readers seeking practical blockchain applications, tokenization represents one of the most commercially viable growth vectors between 2024 and 2026.

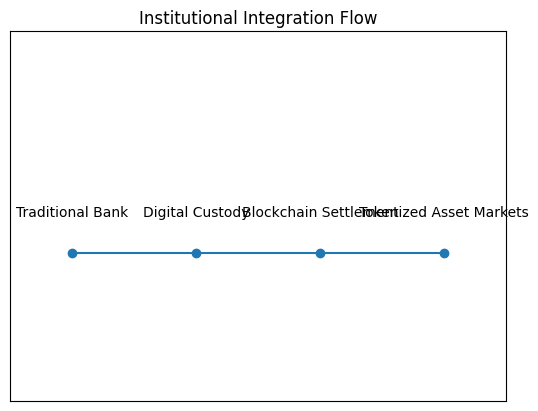

III. Institutional Integration: When Banks Embrace Digital Assets

The Institutional Layer

The third shift involves traditional financial institutions integrating crypto services into existing systems.

Alderoty states:

“Traditional financial institutions are beginning to integrate crypto services into their existing systems.”

This includes:

Digital asset custody

Stablecoin settlement

On-chain liquidity management

Tokenized deposit experiments

Central bank digital currency (CBDC) research

Regulatory Context

Institutional adoption is closely tied to legal clarity. Ripple’s long-running legal battles in the United States significantly shaped the regulatory narrative.

As clarity improves globally, banks gain confidence to:

Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.