Main Points :

- Strategy (formerly MicroStrategy) signals its 12th consecutive week of Bitcoin purchases despite a severe market downturn.

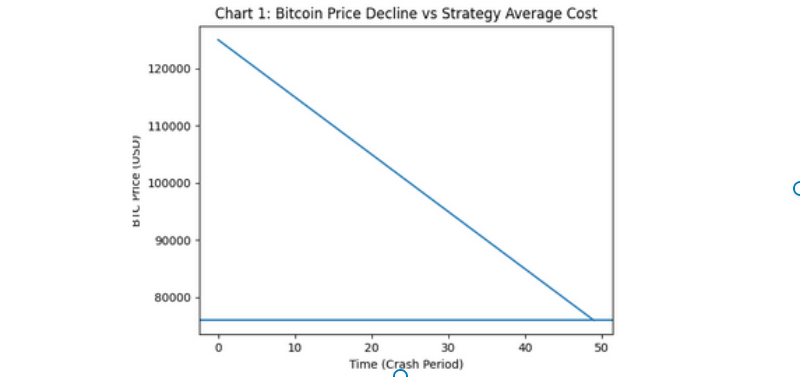

- Bitcoin has fallen more than 50% from its all-time high of over $125,000 to below $76,000.

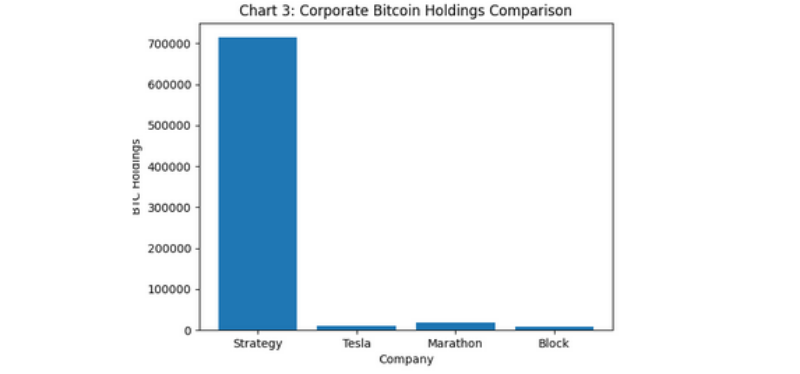

- Strategy currently holds 714,644 BTC worth approximately $49.3 billion at current market prices.

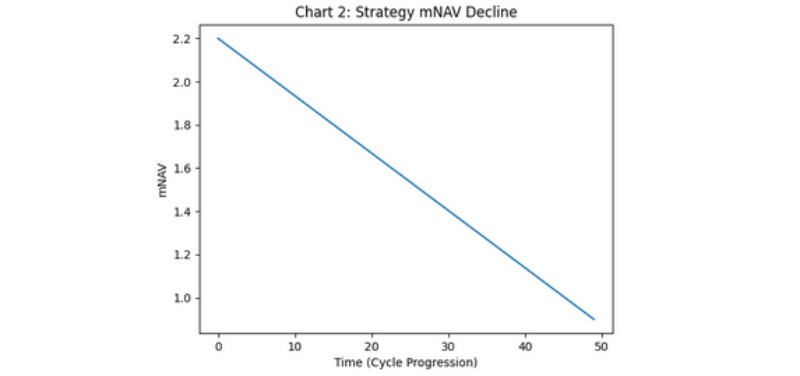

- The company’s mNAV (multiple of Net Asset Value) has fallen below 1, signaling potential structural stress.

- Several crypto treasury firms are under pressure as equity premiums collapse.

- Institutional conviction contrasts with retail caution.

- The downturn may present long-term accumulation opportunities for capitalized players.

1. Saylor’s Persistent Accumulation Strategy

Amid one of the sharpest crypto downturns since the 2022 bear market, Michael Saylor, co-founder and executive chairman of Strategy (formerly MicroStrategy), has once again signaled that the company is preparing to acquire additional Bitcoin. His latest post on X featured the now-iconic Bitcoin accumulation chart that investors have come to interpret as a precursor to another purchase announcement.

If completed, the upcoming transaction will mark Strategy’s 99th Bitcoin acquisition and its 12th consecutive week of purchases. This consistency is remarkable given the backdrop: Bitcoin has dropped more than 50% from its all-time high above $125,000 during the October flash crash, sliding below the company’s reported average acquisition cost of approximately $76,000.

The most recent confirmed purchase occurred on February 9, when Strategy invested over $90 million to acquire 1,142 BTC. This brought total holdings to 714,644 BTC, valued at roughly $49.3 billion at current prices.

Rather than retreating during market panic, Strategy appears to be doubling down.

2. The October Flash Crash and Market Context

The broader crypto market experienced a violent correction following October’s flash crash. Bitcoin’s decline from $125,000 to levels below $76,000 erased hundreds of billions in market capitalization. Altcoins suffered even steeper drawdowns, with many large-cap assets losing 60–70% of their value in dollar terms.

Institutional ETF flows, however, tell a more nuanced story. Spot Bitcoin ETFs in the United States have shown intermittent accumulation, suggesting that while speculative retail activity has cooled, long-term institutional capital has not fully retreated.

At the macro level, tighter global liquidity, elevated interest rates, and renewed risk-off sentiment across equities contributed to capital rotation away from high-volatility assets, including cryptocurrencies.

Yet for long-term treasury allocators like Strategy, volatility appears to be an entry mechanism rather than a deterrent.

3. The mNAV Warning Signal

One of the most critical indicators in the crypto treasury space is mNAV, or multiple of Net Asset Value. This metric measures how much premium (or discount) a company’s stock trades at relative to the value of its underlying crypto holdings.

Strategy’s mNAV has reportedly fallen to approximately 0.90, meaning the market values the company at a 10% discount to the value of its Bitcoin holdings.

Historically, companies trading above an mNAV of 1 can raise capital more easily by issuing equity at a premium, then deploying that capital to acquire more Bitcoin. This mechanism fueled Strategy’s aggressive accumulation over the past several years.

When mNAV falls below 1, however, it implies that equity issuance becomes dilutive rather than accretive. Investors are effectively saying that the company’s operational risks, leverage structure, and execution uncertainty outweigh the premium once assigned to its Bitcoin exposure.

Standard Chartered had previously warned that several crypto treasury companies could fall below an mNAV of 1 by September 2025. That scenario now appears to be unfolding earlier than anticipated.

4. A $12.4 Billion Quarterly Loss

Earlier this month, Strategy reported a staggering $12.4 billion loss in the fourth quarter, largely driven by mark-to-market accounting adjustments tied to Bitcoin’s price decline.

The company’s stock fell approximately 17% following the announcement, although it partially recovered in subsequent sessions, closing recently at $133.88 per share.

The loss underscores the structural volatility inherent in using Bitcoin as a treasury reserve asset. Under accounting rules, unrealized losses must be recognized during downturns, even if the company does not sell its holdings.

This accounting dynamic amplifies earnings volatility and can pressure equity valuations during bear phases.

5. Crypto Treasury Firms Under Pressure

Strategy is not alone. The broader crypto treasury sector has shown signs of structural stress. Several publicly traded companies that adopted Bitcoin or other cryptocurrencies as balance sheet assets have seen their stock prices collapse alongside declining digital asset prices.

As mNAV premiums evaporate, the financial engineering model that once allowed these firms to continuously acquire crypto using equity issuance becomes more fragile.

This creates a divergence between:

- Firms with strong balance sheets and access to credit markets

- Firms reliant on equity premiums to fund acquisitions

Strategy, due to its scale and brand recognition, may retain relative resilience compared to smaller players.

6. Strategic Conviction vs. Leverage Risk

Saylor’s thesis has long been clear: Bitcoin is digital property, a superior long-term store of value, and a hedge against fiat debasement. His strategy is predicated on the belief that over multi-year cycles, Bitcoin will appreciate significantly beyond current volatility.

Critics, however, point to leverage risk. Strategy has historically utilized convertible notes and debt instruments to finance acquisitions. During sharp drawdowns, this leverage magnifies financial stress.

The key strategic question becomes:

Is Strategy exploiting cyclical volatility for asymmetric upside — or compounding systemic balance sheet risk?

For now, Saylor’s actions suggest unwavering conviction.

7. Implications for Investors and Builders

For readers seeking new crypto assets, income streams, or practical blockchain applications, this episode offers several insights:

- Institutional conviction remains intact even during extreme volatility.

- Treasury adoption models are structurally sensitive to equity premiums.

- Market downturns expose leverage weaknesses.

- Long-term capital allocators view corrections as opportunity windows.

- Bitcoin’s role as corporate reserve asset is still being stress-tested.

Entrepreneurs building blockchain products should note that corporate balance sheet integration of crypto remains viable but demands disciplined capital management.

Conclusion: A Defining Stress Test for Bitcoin Treasury Models

Michael Saylor’s signal of continued Bitcoin accumulation amid a 50% market drawdown represents one of the most consequential stress tests of the corporate crypto treasury model to date.

With 714,644 BTC worth roughly $49.3 billion, Strategy stands as the most significant publicly traded Bitcoin proxy in global markets. Its mNAV compression below 1 introduces new financial constraints, yet the company continues to accumulate.

Whether this proves visionary or reckless will depend on Bitcoin’s trajectory over the next cycle.

For sophisticated investors and blockchain builders, the takeaway is clear:

Volatility is not the absence of conviction. It is the proving ground for it.

If Bitcoin reclaims levels above $100,000 in the next macro cycle, Strategy’s current accumulation may be remembered as strategic brilliance. If prolonged weakness persists, it may instead serve as a cautionary tale about leverage in emerging asset classes.

Either way, the experiment is unfolding in real time — and the outcome will shape the future of institutional crypto adoption.