Main Points :

- Ripple has partnered with Jeel, the innovation arm of Riyad Bank, to support Saudi Arabia’s Vision 2030 digital transformation agenda.

- The collaboration will explore cross-border payments, digital asset custody, and tokenization use cases.

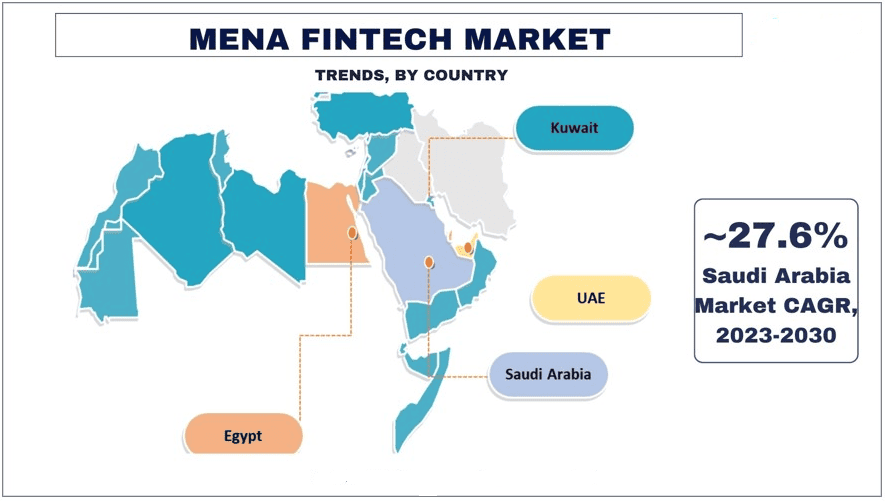

- Saudi Arabia is positioning itself as a global fintech hub in the Middle East.

- Ripple continues expanding in the MENA region amid rising institutional blockchain adoption.

- The partnership reflects a broader global trend of banks integrating enterprise-grade blockchain infrastructure.

- Tokenization and digital asset services are becoming core pillars of next-generation financial architecture.

1. Ripple and Riyad Bank: A Strategic Alignment with Vision 2030

Ripple has announced a strategic partnership with Jeel, the innovation division of Riyad Bank, one of Saudi Arabia’s leading financial institutions. The announcement was shared on January 26 via social media, where Ripple’s Managing Director for the Middle East and Africa, Reece Merrick, described the collaboration as “big news from the Middle East.”

This partnership is designed to align with Saudi Arabia’s Vision 2030 initiative — an ambitious national transformation plan aimed at diversifying the economy beyond oil and positioning the Kingdom as a global leader in technology, finance, and digital innovation.

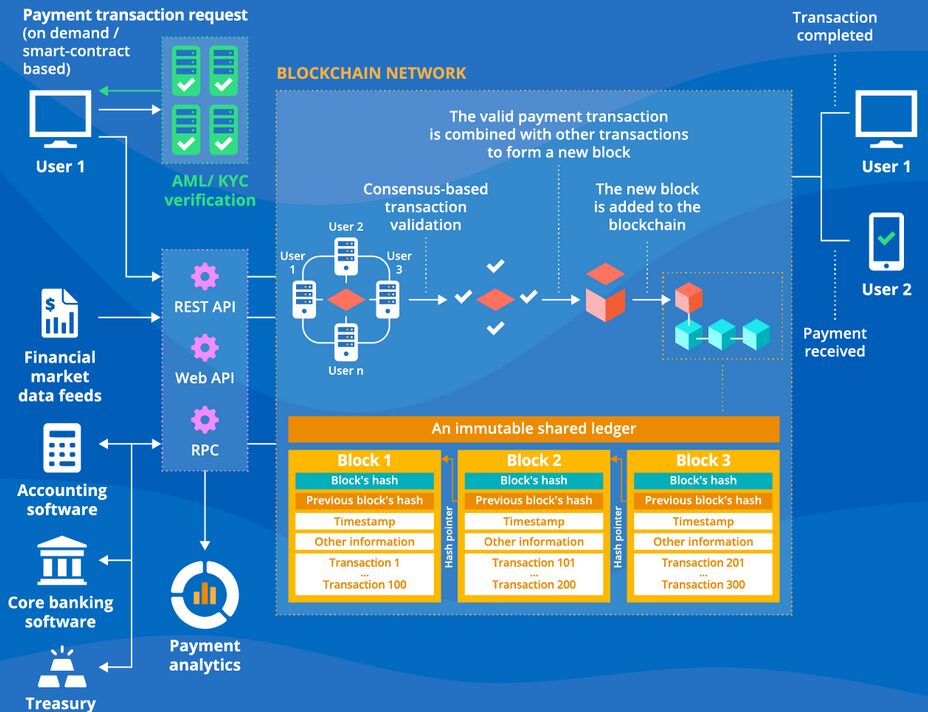

Through a Memorandum of Understanding (MoU), Ripple and Jeel will explore integrating secure and scalable blockchain solutions into Saudi Arabia’s national financial infrastructure. The focus is not speculative crypto trading but enterprise-grade financial architecture capable of supporting real-world institutional use cases.

Saudi Arabia’s leadership has made digital transformation a core pillar of its economic future. Financial modernization, regulatory sandbox programs, and strong sovereign support for fintech initiatives have accelerated innovation across the Kingdom. Ripple’s involvement signals international validation of Saudi Arabia’s fintech ambitions.

2. Exploring High-Impact Blockchain Use Cases

The partnership will focus on three primary use cases:

Cross-Border Payments

International remittances remain a critical economic channel in the Gulf region. Saudi Arabia is one of the world’s largest remittance-sending countries, with billions of dollars flowing annually to Asia, Africa, and other parts of the Middle East.

Traditional correspondent banking networks are often slow, costly, and opaque. Ripple’s blockchain-based payment infrastructure aims to reduce settlement times from days to seconds while improving transparency and lowering transaction costs.

For readers exploring revenue opportunities, this is significant. Payment infrastructure is one of the most commercially viable blockchain applications. Unlike purely speculative tokens, payment rails generate transactional demand and institutional usage.

Digital Asset Custody

As financial institutions begin offering exposure to digital assets, secure custody becomes a foundational requirement. Institutional-grade custody solutions must comply with regulatory standards, capital controls, and cybersecurity frameworks.

Ripple’s collaboration with Jeel includes exploring custody services for digital assets within Saudi Arabia’s evolving regulatory landscape. This could lay groundwork for bank-backed digital asset services in the region.

Custody is a high-margin infrastructure business. Globally, major financial institutions are building custody divisions because asset safekeeping becomes increasingly valuable as tokenized assets scale.

Tokenization

Tokenization refers to representing real-world assets — such as real estate, bonds, commodities, or equities — as digital tokens on blockchain networks.

This market is rapidly expanding. Analysts from major consulting firms estimate that tokenized assets could represent trillions of dollars in value over the next decade.

For Saudi Arabia, tokenization could unlock:

- Infrastructure financing

- Real estate fractionalization

- Sovereign bond innovation

- Trade finance efficiency

Ripple’s enterprise blockchain infrastructure is designed to integrate with existing financial systems rather than replace them, making it suitable for regulated environments.

3. Saudi Arabia’s Position as a Fintech Powerhouse

Saudi Arabia has been rapidly investing in financial technology infrastructure. Under Vision 2030, the Kingdom aims to:

- Increase non-oil GDP contribution

- Expand digital payment adoption

- Encourage fintech startups

- Modernize financial regulations

The Saudi Central Bank has launched regulatory sandbox programs allowing fintech companies to test blockchain-based financial services under supervision.

Compared to Western markets, the Middle East offers a unique advantage: strong sovereign coordination and rapid top-down implementation of policy initiatives.

Ripple’s regional expansion into Saudi Arabia builds upon its growing presence in the UAE and other MENA markets. The Middle East is becoming a serious competitor to Europe and Asia in blockchain adoption.

4. Ripple’s Broader Global Strategy

Ripple has faced regulatory battles in the United States, but internationally, it has continued expanding partnerships with banks and financial institutions.

Its strategy centers on:

- Enterprise blockchain solutions

- Institutional payment corridors

- CBDC infrastructure collaborations

- Tokenization frameworks

Rather than competing as a retail-focused cryptocurrency brand, Ripple increasingly positions itself as financial infrastructure for regulated markets.

The Saudi partnership reinforces this institutional narrative.

5. Market Implications for XRP and Digital Assets

While the announcement did not specify immediate use of XRP tokens, Ripple’s ecosystem historically integrates XRP as a bridge asset for liquidity in cross-border transfers.

If implemented at scale, cross-border payment corridors in the Gulf region could increase demand for blockchain-based liquidity solutions.

However, investors should distinguish between:

- Infrastructure adoption (long-term value driver)

- Token price speculation (short-term volatility)

Institutional partnerships typically signal long-term structural growth rather than immediate price surges.

6. Global Context: Why This Matters Now

Across the globe, banks are increasingly exploring:

- Stablecoin settlement systems

- Tokenized deposits

- Digital bond issuance

- Regulated crypto custody

Major financial institutions in Asia, Europe, and the Middle East are racing to build blockchain-integrated financial systems.

Saudi Arabia’s scale, sovereign wealth capacity, and regulatory coordination make it an ideal environment for enterprise blockchain deployment.

For blockchain entrepreneurs and fintech builders, the lesson is clear:

Real opportunity lies not in speculative hype cycles but in infrastructure integration.

7. Practical Takeaways for Blockchain Builders and Investors

For readers seeking practical blockchain applications and revenue models:

- Cross-border payment rails remain one of the strongest use cases.

- Custody services represent institutional recurring revenue streams.

- Tokenization is likely the next trillion-dollar market.

- Regulatory alignment is critical for sustainable growth.

- Emerging markets may adopt faster than legacy Western systems.

Saudi Arabia’s Vision 2030 acts as a macro catalyst for blockchain adoption in the region.

Conclusion: A Long-Term Institutional Play

Ripple’s partnership with Riyad Bank’s Jeel division reflects a strategic shift in global blockchain development.

This is not about retail speculation. It is about integrating blockchain into national financial systems.

As governments seek digital transformation, enterprise blockchain providers like Ripple position themselves as infrastructure layers beneath future financial architecture.

For investors and builders looking for the next wave of opportunity, the message is clear:

The future of crypto is not only decentralized finance — it is regulated, institutional, tokenized finance integrated with sovereign economic strategies.

Saudi Arabia’s Vision 2030 may become one of the defining case studies of that transformation.